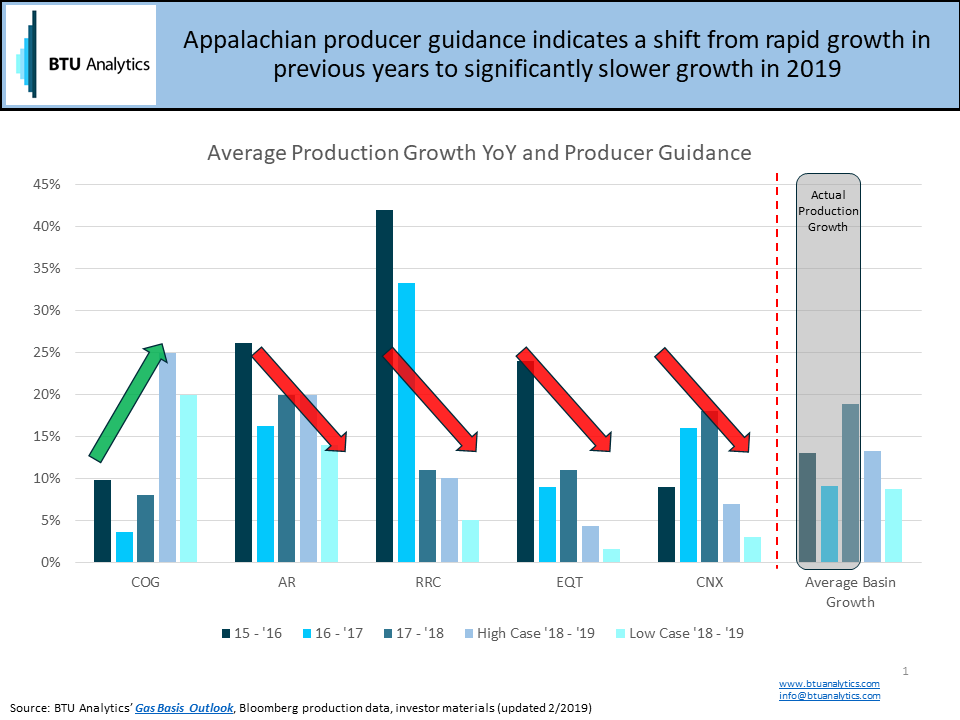

For over a decade, Marcellus and Utica production has hit new records each year. Now, the majority of Appalachian producers are tapping the breaks on production gains in 2019. In 2018, the Appalachian market saw multiple greenfield and brownfield pipeline projects come into service. The new pipelines allowed for year-over-year production to jump higher by 3.9 Bcf/d in December 2018 resulting in production setting a new record high of 30.1 Bcf/d. However, in 2019, no major pipeline expansions are expected to bring new capacity to the basin. Additionally, pressure by shareholders for E&Ps to move towards a goal of capital stewardship and free cash flow generation is impacting producer growth plans. Have we reached peak Appalachian gas production or not?

As the slide below shows, across a sampling of Appalachian producers, only Cabot Oil & Gas (NYSE: COG) is providing guidance in 2019 indicating higher growth rates than in 2018. Other E&Ps such as Antero (NYSE: AR), Range (NYSE: RRC), EQT (NYSE: EQT), and CNX (NYSE: CNX) are all expecting growth to be flat or grow less than the previous year.

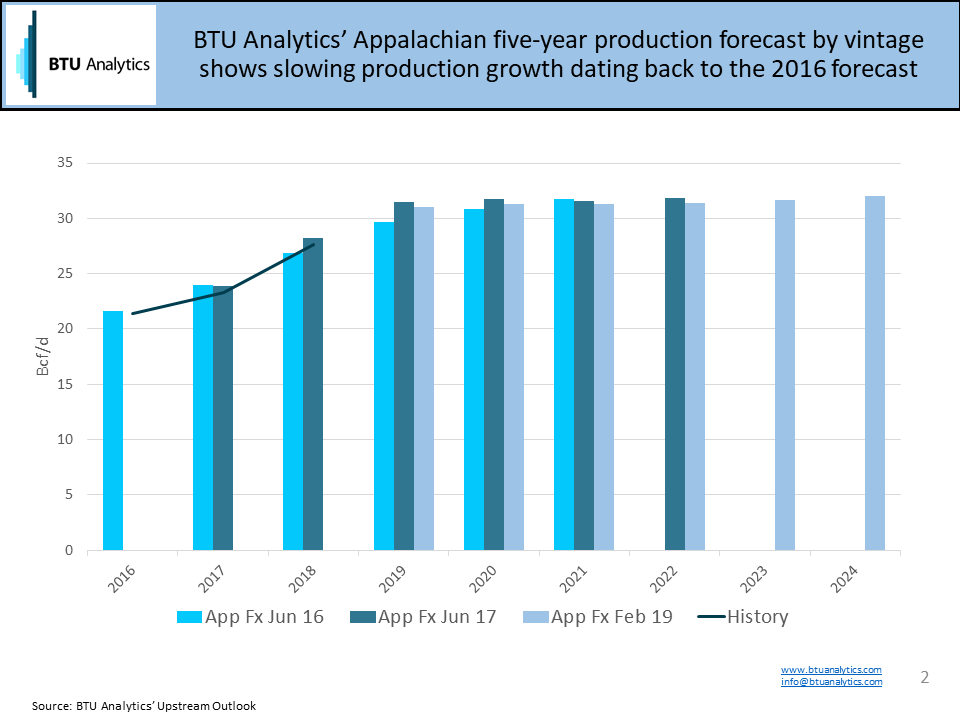

BTU Analytics has been calling for a slowing of Appalachian growth for years based on our gas market balance modeling estimates. We have brought this to the attention of our Energy Market Commentary readers in 2016 and in 2018. As shown below, BTU Analytics’ Upstream Outlook forecast for Appalachia in 2016 and 2017 had slower growth arriving by 2019.

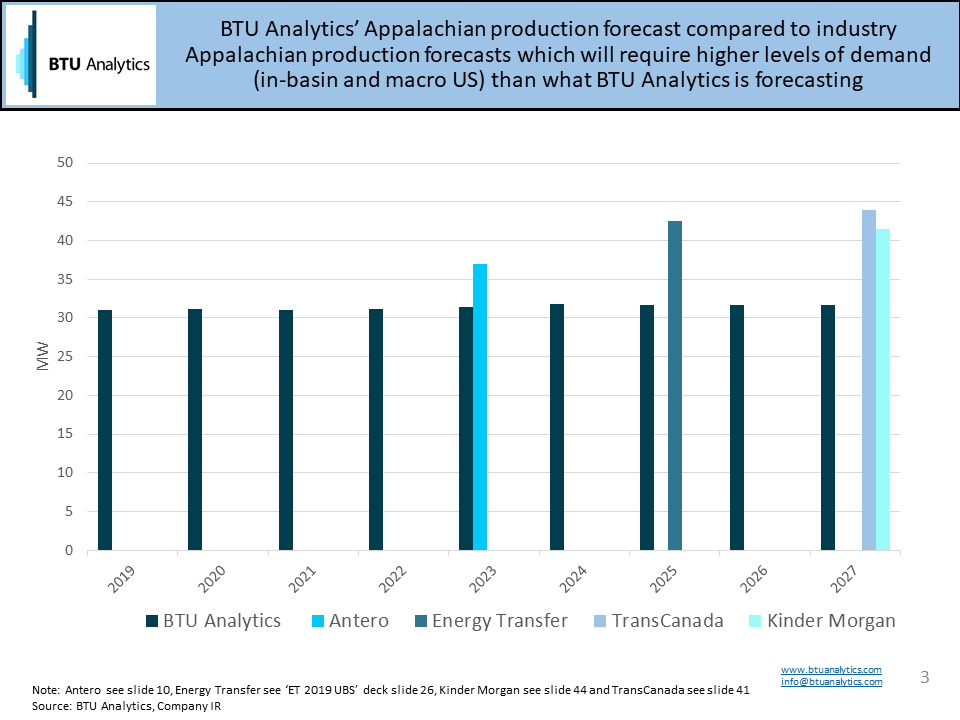

Appalachian production forecasts have been pipeline constrained for years but now the region is transitioning. Appalachian production will now be constrained by limited in-basin demand growth, downstream constraints on pipelines and demand, and capital availability. BTU Analytics forecasts Appalachian production to remain flat through 2027 at approximately 31 Bcf/d.

However, several industry forecasts are more bullish on Appalachian production than BTU Analytics. Bullish Appalachian production growth industry forecasts include Antero at 37 Bcf/d by 2023, Energy Transfer at 42.5 Bcf/d by 2025, Kinder Morgan, and TransCanada at 41.5 Bcf/d and 44 Bcf/d respectively by 2027 as shown in the slide below. In order to achieve these forecasts one must believe in a combination of the following: 1) higher natural gas prices to fund operations, 2) significant additional in-basin demand growth to absorb supply, and 3) the most bullish cases, the development of additional greenfield pipelines to downstream markets.

In the last decade, Appalachian producers have done a fantastic job at claiming market share. Now, Appalachian natural gas meets the majority of demand east of the Mississippi River. However, BTU Analytics fades the prospect of a new greenfield pipeline from Appalachia to the Gulf Coast due to escalating Appalachian long haul pipeline costs. Is the current pause in Appalachian production a short term issue or have we reached ‘Peak Appalachia’ gas? To follow BTU Analytics’ coverage on Appalachian and other regional natural gas markets, subscribe to the Gas Basis Outlook.