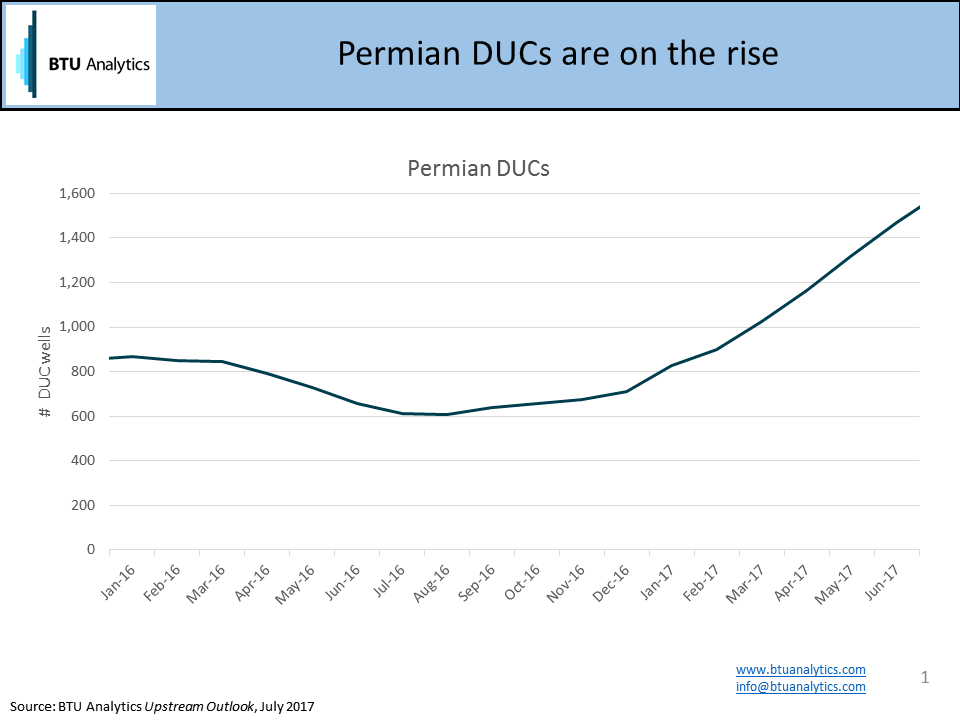

The number of drilled uncompleted wells (DUCs) in the Permian (or “PUCs”) is rapidly increasing as drilling activity in the region is outpacing completion activity. Total Permian DUCs reached nearly 1500 in June, over double what they were a year ago, as seen in the figure below. This increase in Permian DUCs comes as the market has finally worked through most of the excess backlog of DUCs in other regions. Those DUCs created a “hangover” in the market following the oil price crash, as they provided a source of production that could be turned on quickly and economically since costs associated with drilling could be considered sunk.

Given this new run-up of DUCs in the Permian, are we setting up for a second hangover? What are the implications for oil production and price given this growing backlog of DUCs in the Permian?

First, it is important to recognize that the cause of today’s increase in Permian DUCs is different than the buildup that occurred beginning in 2015. Back then, the backlog was largely driven by market considerations after the oil price crash, as producers slowed completion activity in anticipation of a recovery. In contrast, Permian DUCs are appearing today due to constraints in completion crews and infrastructure. However, even though the cause of new DUCs is different this go-round, the ramifications to the market may end up being similar, particularly if there is an oil price correction.

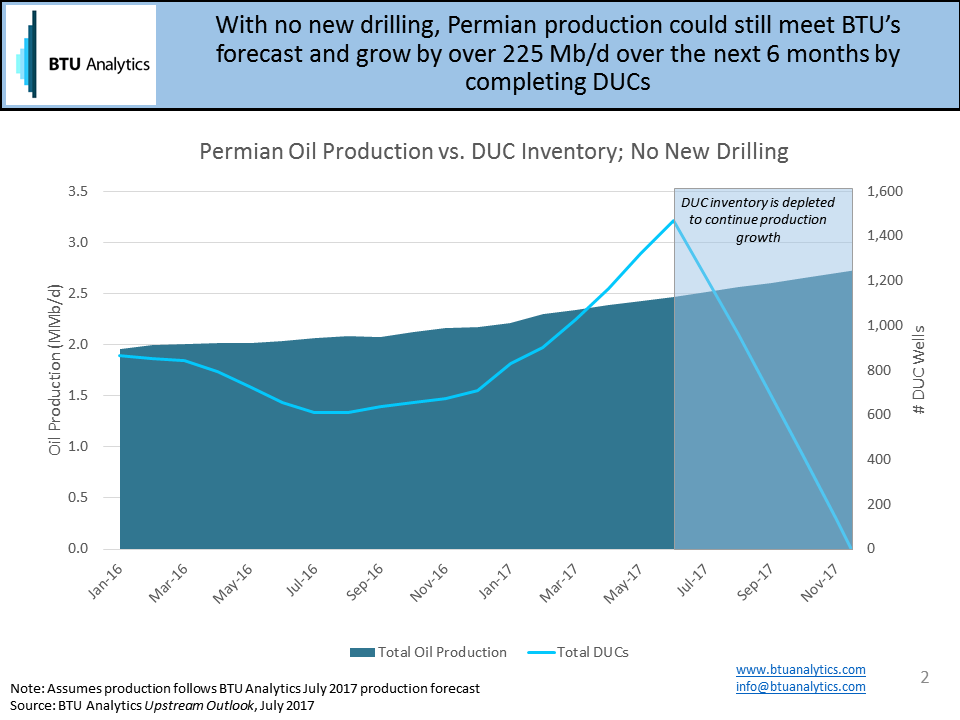

To address the impact Permian DUCs may have, we quantified the time it would take to work through our current backlog of DUC inventory. If we consider a world where there was no new drilling activity, turning just our backlog of DUCs to sales would sustain our production forecast over the next six months, as seen in the figure below. Put another way, drilling in the Permian could completely stop, and production would still be able to grow by 225 MB/d over the next six months by completing the current DUC inventory.

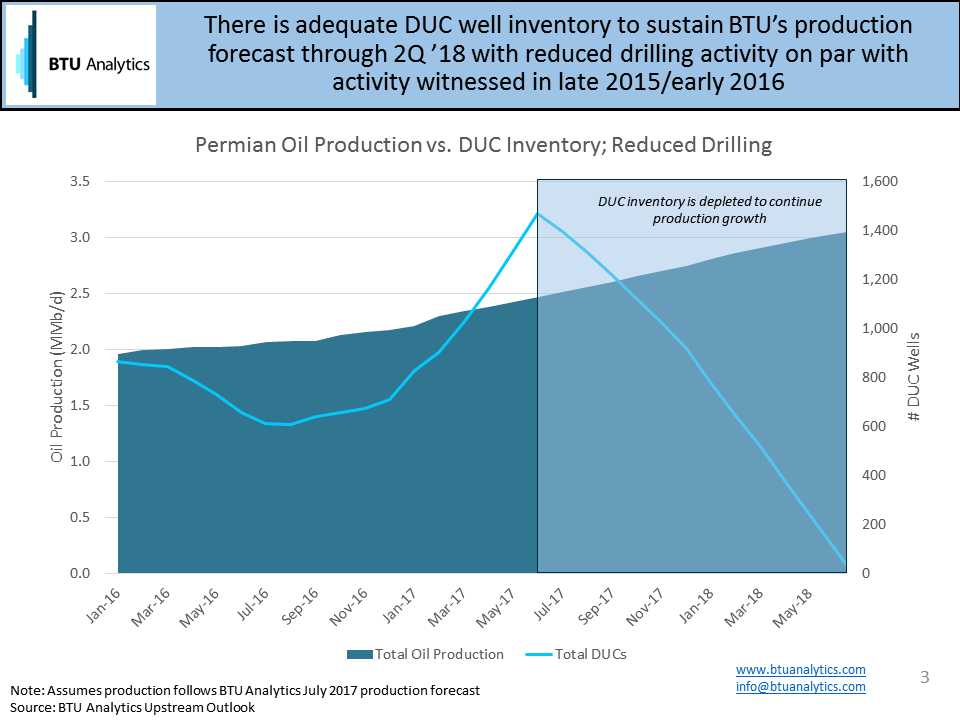

This is a bookend, but not realistic given that drilling decreased but did not completely fall to zero during the 2014 crash. To adjust for this, we took drilling activity down to the levels seen in late 2015/early 2016, when producers began to scale back heavily on drilling. This equates to drilling about 175 wells/month, down from nearly 400 wells/month currently. In a world with this reduced drilling activity, there is adequate DUC inventory to sustain our production forecast through 2Q2018, as seen in the figure below.

Note, these scenarios assume production growth based on our current forecast. Instead if production goes flat at current levels, there is enough DUC inventory at a reduced drilling scenario to maintain production throughout 2018.

In a positive oil price environment, these DUCs are less impactful and can be worked off in due course as infrastructure constraints are lifted. While there has been recent optimism in the market given the outcome at the July 24 OPEC meetings, BTU Analytics sees the oil market as fundamentally long supply, making a price recovery tenuous at best. Ultimately, the growing backlog of Permian DUCs means low oil prices are unlikely to stop production growth in the Permian over the next 12 months. Since Permian production now makes up over a quarter of total US oil production, continued growth from this region will have a dramatic impact on US production and in an oversupplied market, will weigh heavily on oil prices.

To keep up with our outlook on the oil market, check out the Oil Market Outlook, and to continue tracking Permian production and DUCs, check out the Upstream Outlook.