With Gulf Coast Express (GCX) gas pipeline full and the next Permian pipe not expected until early 2021, Permian producers are right back where they started. Considering Permian pipeline constraints, flaring above base levels is likely to remain for the foreseeable future. As a result, some producers may choose to shut-in volumes as the cost of producing gas becomes too expensive in a weak Waha environment. However, whether to flare or shut-in depends on a combination of asset type, state regulations, firm transportation capacity, and overall company strategy. For producers like Apache, shutting in gas is material to their bottom line, but for others, shutting in is a small cost relative to the revenue to be captured from growing oil production. Looking to the shoulder season in 2020, after winter demand ebbs, will another bout of weak Waha pricing result in the same operators shutting-in and flaring or will the mix change based on firm transportation agreements on new gas pipelines?

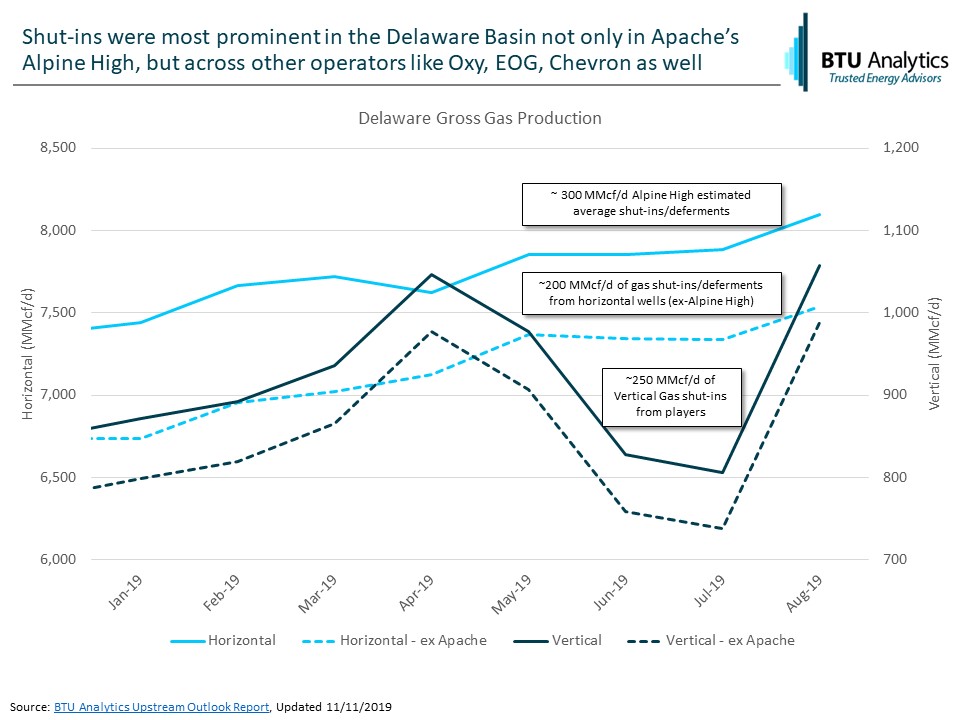

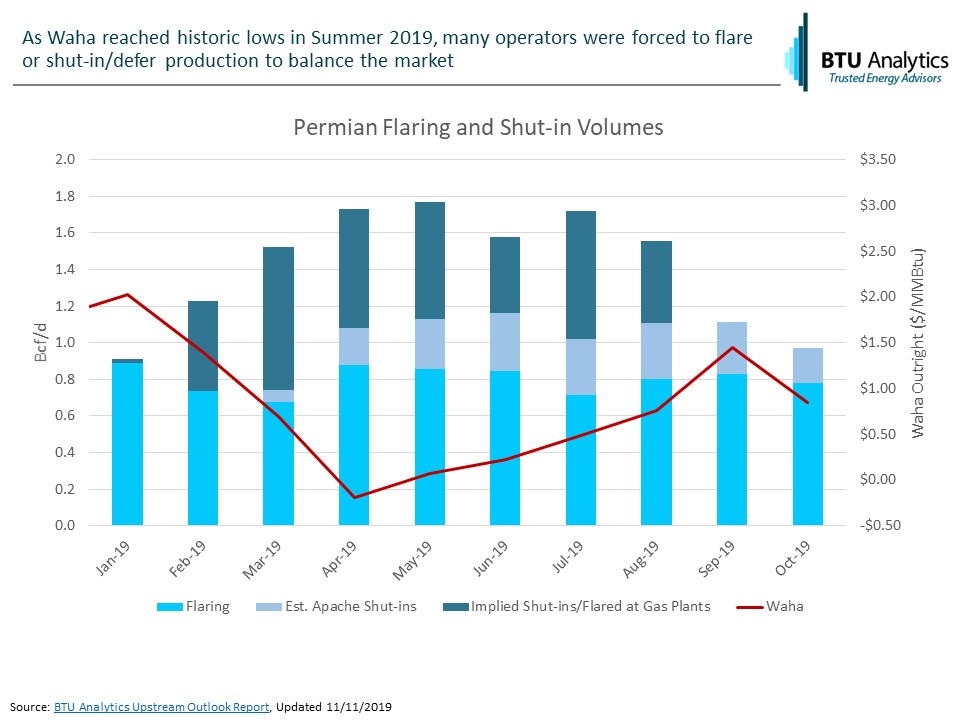

While Apache’s Alpine High shut-ins/deferments were the poster child for producers responding to weak gas prices in the Permian, the graph below highlights that wellhead flaring and gas shut-ins at Alpine High were only part of the balancing equation until Kinder Morgan’s Gulf Coast Express Pipeline (GCX) began service in September. In addition to Apache’s shut-in volumes, BTU Analytics estimates there was at least an additional 450 MMcf/d of gas that was shut-in/deferred by other operators or flared at the tail-gate of a gas plant.

While visibility on gas plant flaring is limited, visibility on operator production in New Mexico and Texas shows that it was primarily Delaware Basin operators who shut-in production in response to low gas prices. Higher GORs in the Delaware make operator economics more dependent on gas prices than their counterparts on the Midland side. The chart below highlights that shut-ins of legacy and likely gassier vertical production accounted for almost 250 MMcf/d in the summer of 2019. Horizontal shut-ins/production deferments outside of Alpine High accounted for an additional 200 MMcf/d of lost production. Operators like Oxy, EOG, Exxon, Mewbourne, and Chevron all appear to have shut-in production this summer. These shut-ins/deferments paired with Apache’s Alpine High shut-ins/deferment suggest that there was at least an average of 750 MMcf/d of production that could be turned back online that could rapidly provide supply to help fill GCX when it came online. This production can likely be turned to sale faster than flared gas volumes and directly impacted the fill rate of GCX.

The next pipeline from the Permian, Permian Highway, is not scheduled to be completed until early 2021. Over the next 12 months, Permian gross gas production could grow by as much a 2 Bcf/d. However, with GCX already full, Permian pipeline constraints in 2020 could create a similar dynamic in advance of Permian Highway with a few nuances. The key difference being that Apache and other large operators like Oxy and Exxon who shut-in material production this summer also hold firm capacity on Permian Highway. BTU Analytics continues to expect a significant gas takeaway shortage in 2020, and winners and losers will once again emerge in the Permian based on who owns firm transportation on new gas pipelines. As majors and large independents continue to focus on the Permian and take capacity out on new gas pipelines, smaller independents may be at a disadvantage. For more information on detailed producer shut-in estimates, request a sample of our Upstream Outlook Report.