While many have prognosticated that the drop in crude prices will ultimately hurt the prospects for natural gas exports, BTU Analytics would contend that in the long-run, the drop in global supply will ultimately benefit exporters of natural gas from the US. The boon to US natural gas exporters, and ultimately to US natural gas producers, will come in the form of a lack of supply investment in downstream markets around the world. As an example, let’s take a look at a growing US export partner here in North America: Mexico.

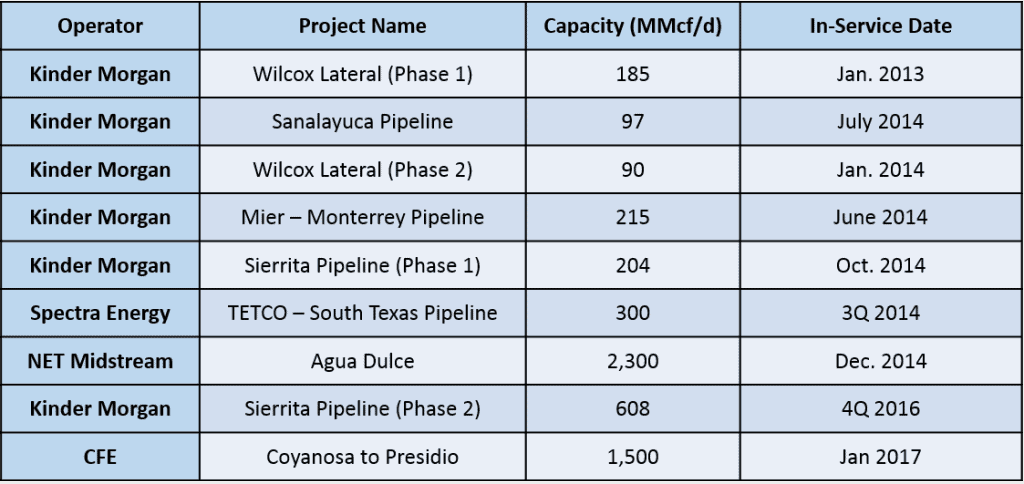

Not all US exports are destined for overseas markets in the form of LNG. Mexico has committed to more than 5 Bcf/d of pipeline expansion projects to capitalize on cheap US natural gas supplies sourced from the Permian basin in West Texas and the Eagle Ford in South Texas.

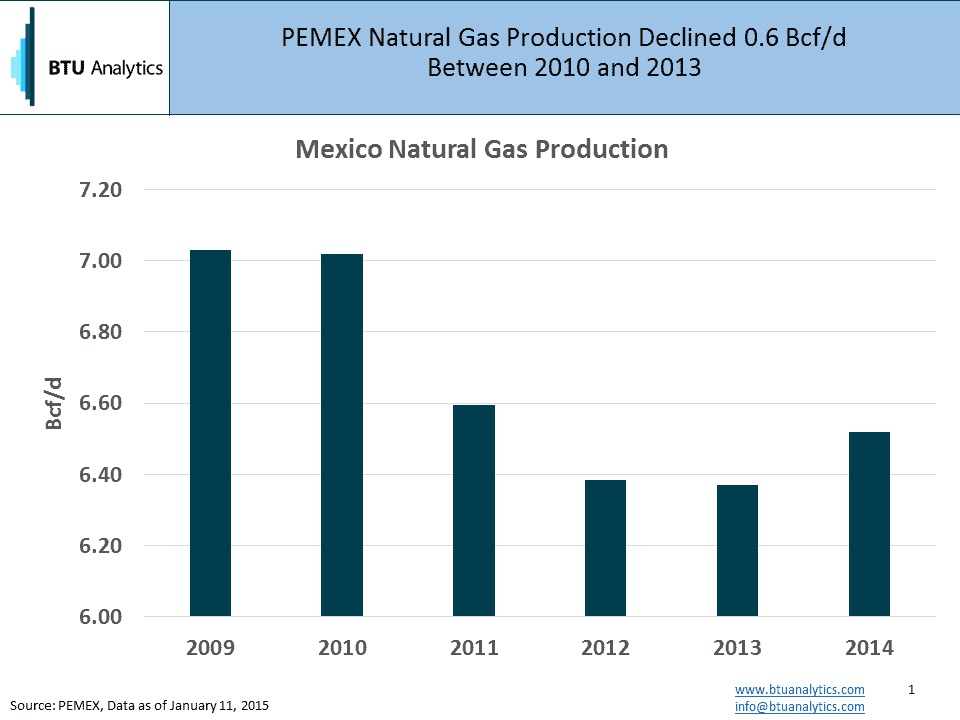

Mexican natural gas production declined 0.6 Bcf/d between 2010 and 2013 as cheap natural gas in the US chased out higher cost conventional development in Mexico and PEMEX shifted capital to focus on oil assets.

US pipeline exports of natural gas ratcheted up over this time period backing out planned imports of oil price linked LNG. In 2014, natural gas production in Mexico rebounded due to increases in associated natural gas production from investments in Mexican oil fields. One would expect the fall in crude to slow the pace of investment in Mexico’s oil field developments even with Mexico in the beginning stages of energy reform. Should Mexican natural gas production return to the rate of decline experienced from 2010 to 2013 (5% per year), Mexican production would decline by about 0.2 Bcf/d per year or 1 Bcf/d by 2020. This decline would thus boost the demand for US sourced natural gas production and increase the utilization of the expansion pipes to Mexico.

In addition to the potential for natural gas supply declines in Mexico, demand for natural gas should be on the rise over the next 5 years as new natural gas fired generation is added to the mix. We’ll cover the outlook for Mexican natural gas demand growth in a separate post.

So while the drop in crude will be painful for some projects, producers in dry natural gas plays in the US like the Haynesville and Marcellus could see long term benefit from a lack of investment in oil plays not just in the US but globally as well (See US Upstream Outlook for BTU Analytics’ drilling and production forecasts).

BTU Analytics does not dispute that many greenfield LNG projects in the US will likely be scrapped in the wake of weaker crude oil prices as investors, international consumers, and producers hit the brakes on taking additional long-term take or pay contracts to their respective balance sheets, but for the ~10 Bcf/d of LNG projects that will likely be developed in the next five years the outlook may not be so bleak.

BTU Analytics is hiring! We’ve had a great year and looking to add to our team. Check out BTU Analytics Careers for more information