On October 13, 2017 FERC Commissioner Cheryl LaFleur dissented in her vote for the granting of certificates for Atlantic Coast Pipeline (ACP) and Mountain Valley Pipeline (MVP). While the Commissioner was outvoted in favor of proceeding with development, the dissent was mostly focused on whether a single alternative pipeline could meet the need and minimize environmental impacts to the region. These actions raised the question of how the Atlantic Seaboard market would fair if these pipelines were somehow not put into service. BTU Analytics has looked at flows along the Transco corridor before in previous commentary which showed the progress Appalachian gas has made in capturing demand. In this commentary, we will look at how Atlantic Seaboard gas power burn pushes higher and what power plant development is ahead in the coming years.

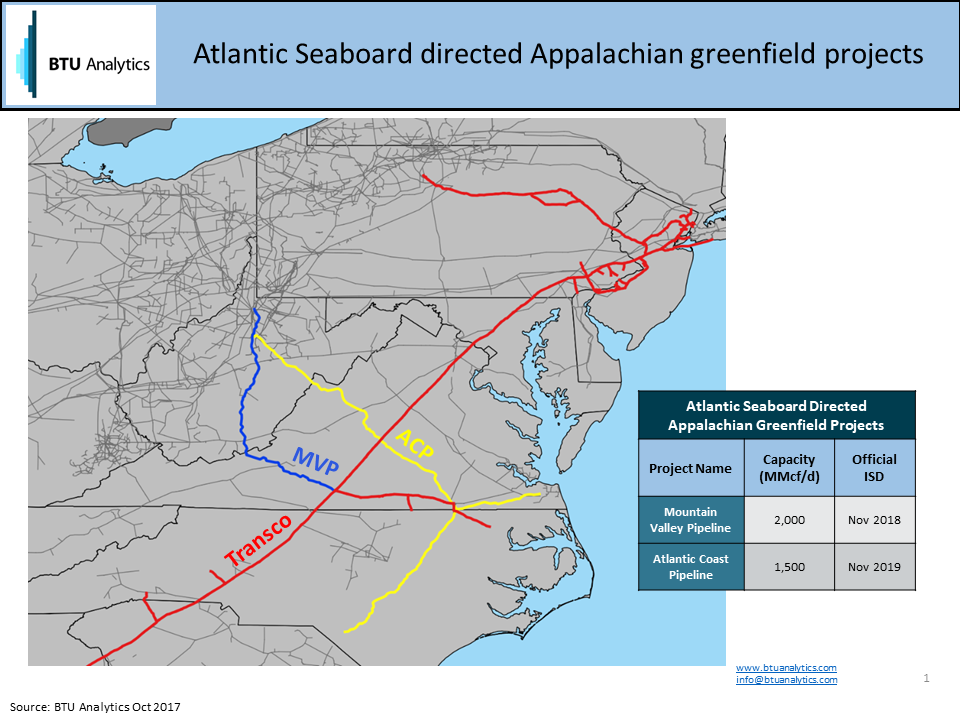

MVP and ACP plan to deliver gas produced in southwest Appalachia directly to the Atlantic Seaboard to the tune of 2.0 Bcf/d by Q3 2018 and 1.5 Bcf/d by 2019 respectively – see map below.

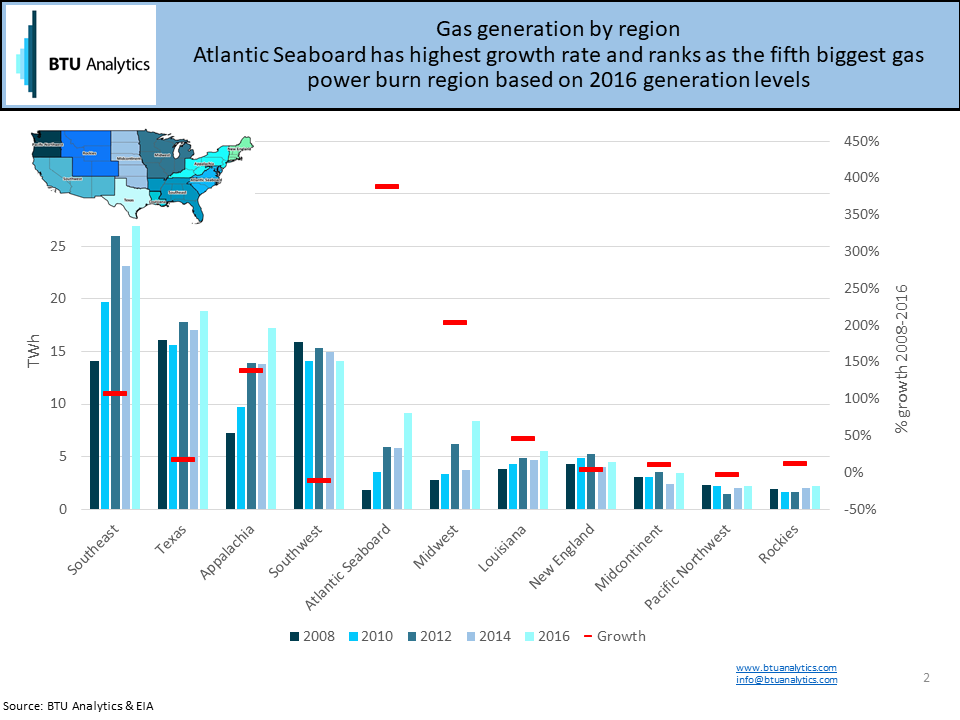

There are solid fundamental trends in place that support these two projects. The Atlantic Seaboard, which BTU defines as Maryland, Delaware, Virginia, North Carolina and South Carolina, has been the fastest growing gas generation region in the U.S. and now ranks fifth of all regions measured by BTU as shown below. Also note the other two fastest growing regions are Appalachia itself and the Midwest region, which can take advantage of low cost Appalachian gas supply.

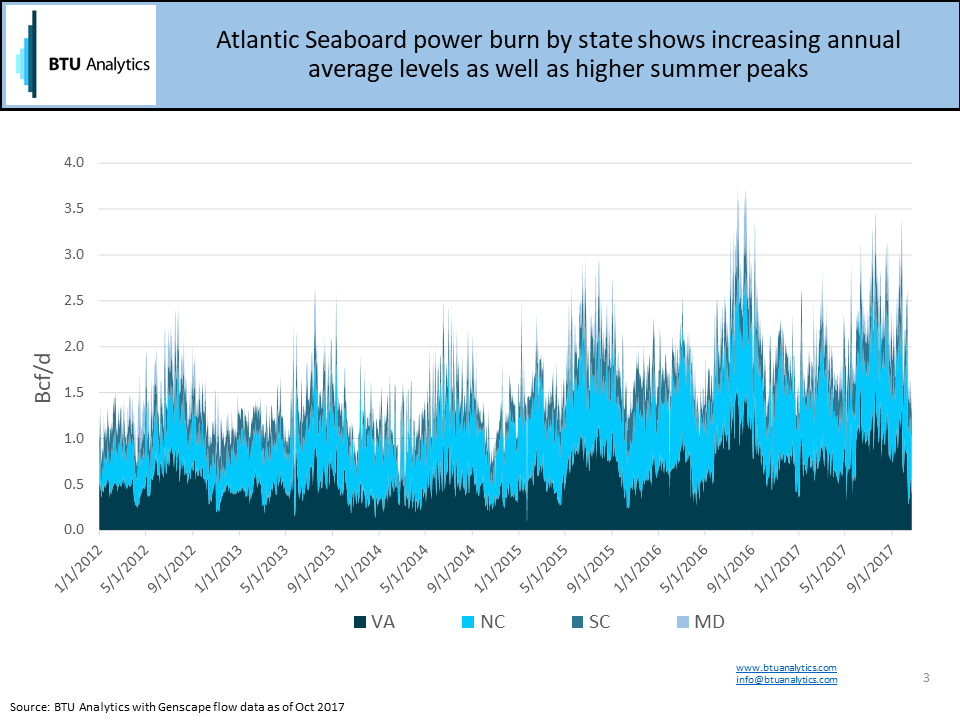

If we look at Atlantic Seaboard power burn, as shown below, it has steadily climbed from an average of 1.3 Bcf/d in 2012 to 2.1 Bcf/d 2017 YTD with peak days rising from 2.5 Bcf/d in 2012 to 3.5 Bcf/d in 2016 and 2017.

In addition to growing gas demand from power development in the Atlantic Seaboard, Dominion’s Cove Point export terminal is 95% complete and expected to go into service in Q4 2017 with 0.8 Bcf/d of export capacity.

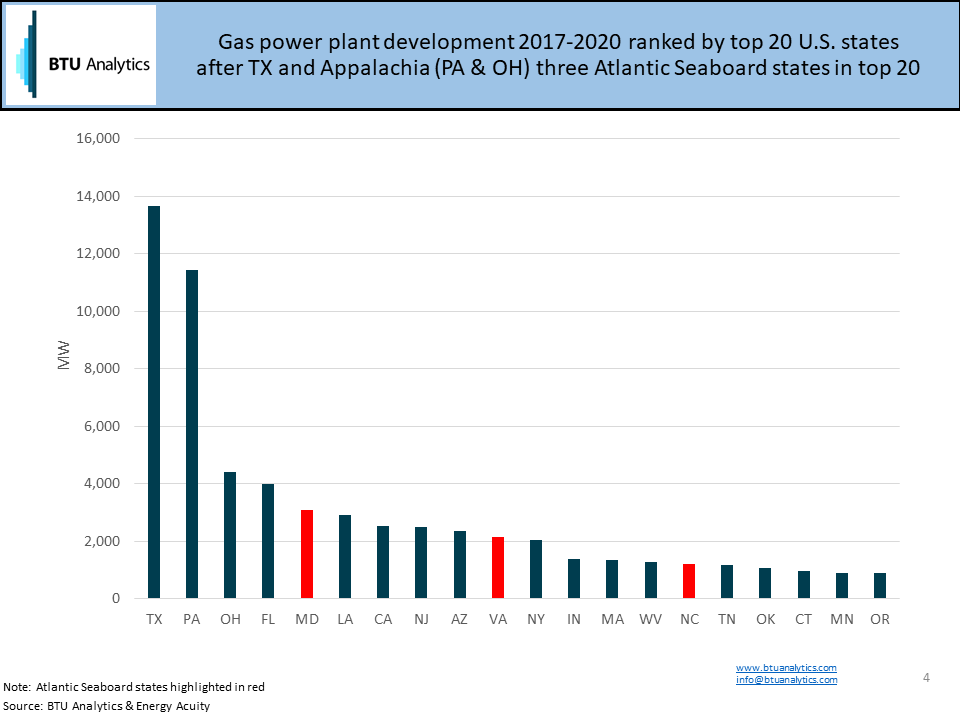

More gas demand is coming. Looking at future gas power plant development at a state level, three of the Atlantic Seaboard states rank in the top 20 states for development as shown in the slide below. While the top three spots, Texas, Pennsylvania and Ohio, are all driven by a combination of large state populations and low cost growing gas supplies within state boundaries, Atlantic Seaboard states, Maryland, Virginia and North Carolina, have aggressive gas plant development plans which will further drive gas demand through 2020.

How will the supply/demand balance play out in the Atlantic Seaboard? Despite the FERC Commissioner’s dissent, MVP and ACP are set to move forward bringing low cost supply to growing demand markets. Track exactly how this all unfolds through BTU Analytics’ Northeast Gas Outlook subscription.