California ISO (CAISO) has stood at the forefront of deploying solar resources, with the largest share of operational solar assets in the U.S. totaling about 16.5 GW of capacity. Despite the benefits that come with solar, increasing its presence yields a substantial amount of intermittent generation. Battery energy storage systems (BESS) have been the growing solution to addressing renewable intermittency issues, but up to this point they have mostly acted on the periphery through the ancillary services market. In this Energy Market Insight, we will discuss how BESS contribution has evolved into a more prominent role in CAISO and how it will likely grow with its continued build out.

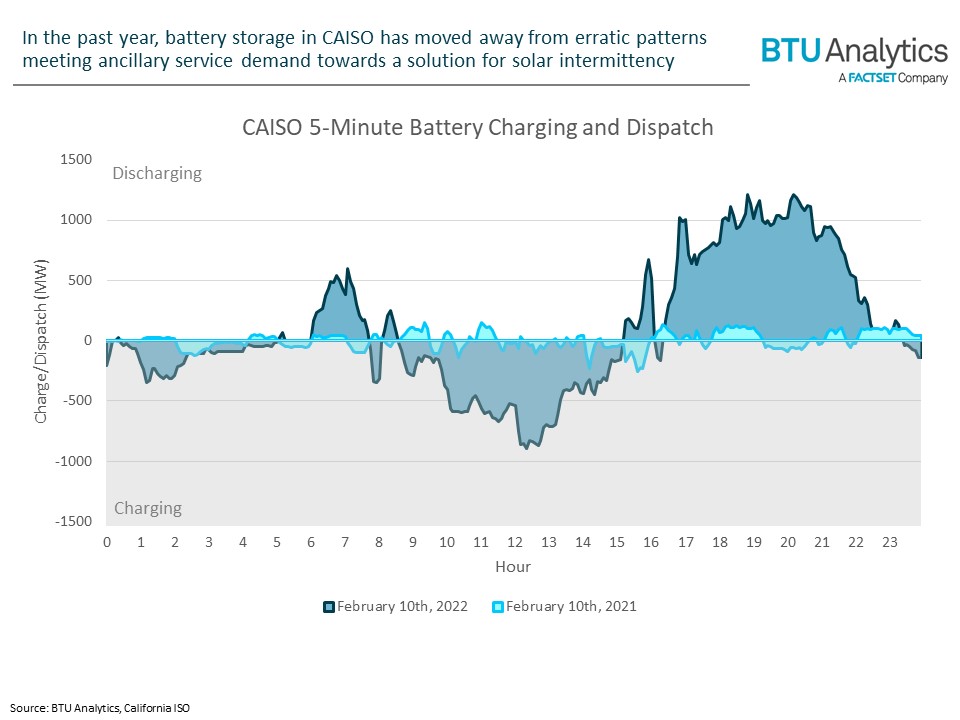

In its preliminary stages, due to limits in duration and capacity, BESS facilities commonly served as part of the ancillary services market by regulating small market imbalances in the transmission system. However, recent data from CAISO suggests that storage has come to scale enough to contribute to meeting daily peak load, by charging in the afternoon during peak solar generation and dispatching in the evening when solar generation declines.

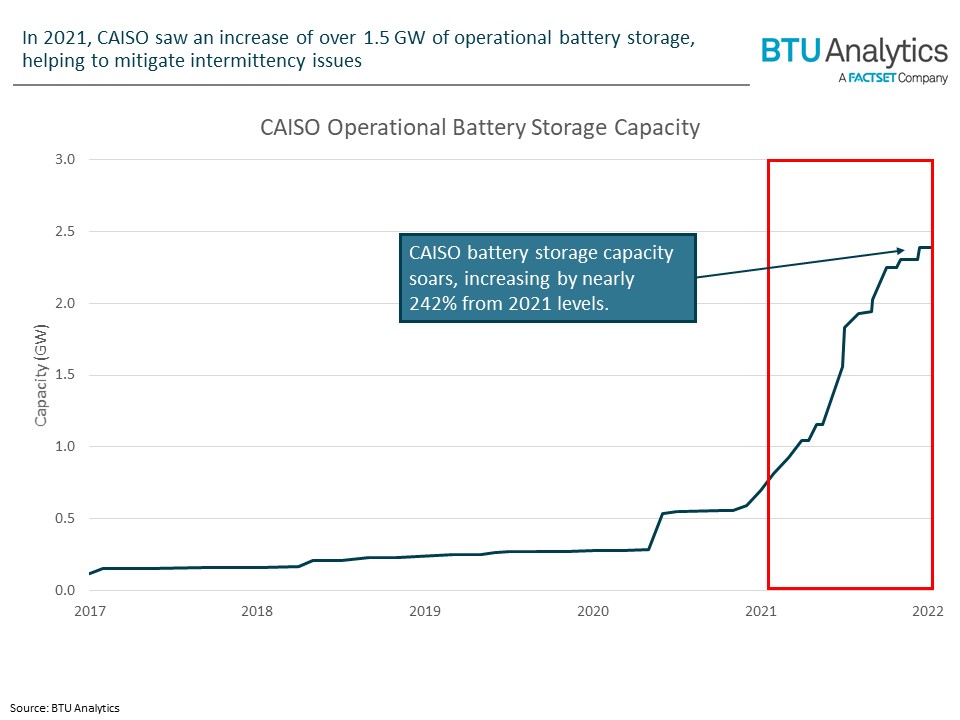

These changing trends in charging and dispatch follow the continued buildout in BESS capacity. With a drastic increase in operational capacity, BESS can provide more significant contributions to the grid than in prior years.

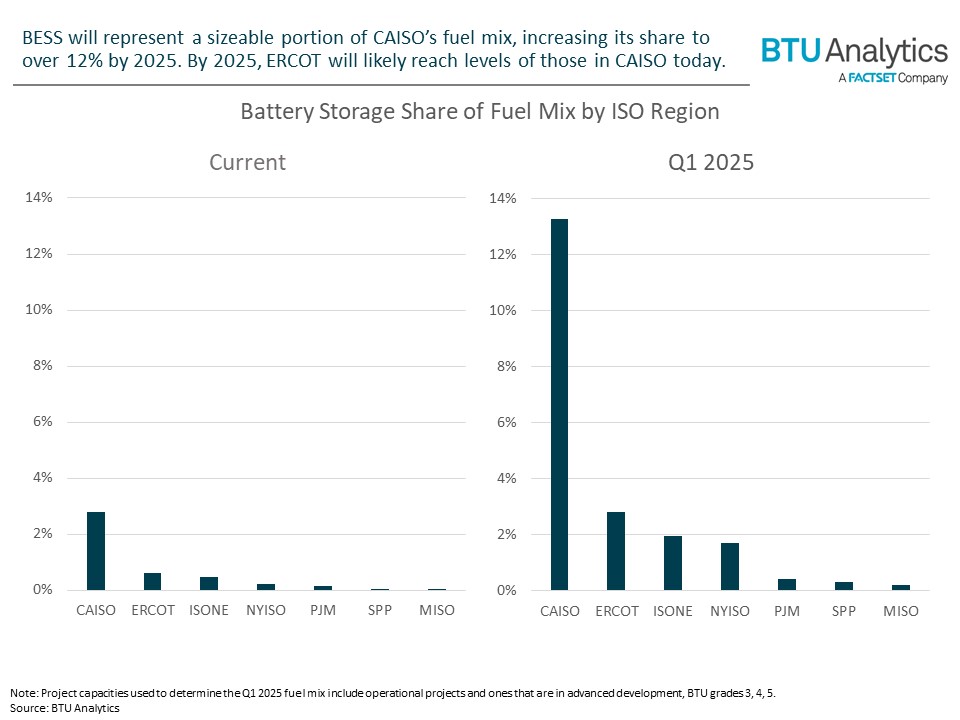

In California, imports and natural gas fired peaking plants predominantly serve daily peak demand. As BESS operations continue to rise, peak power prices will likely be offset by the deliverability of BESS capacity. Furthermore, imports and fossil fuel-fired generation may decrease.

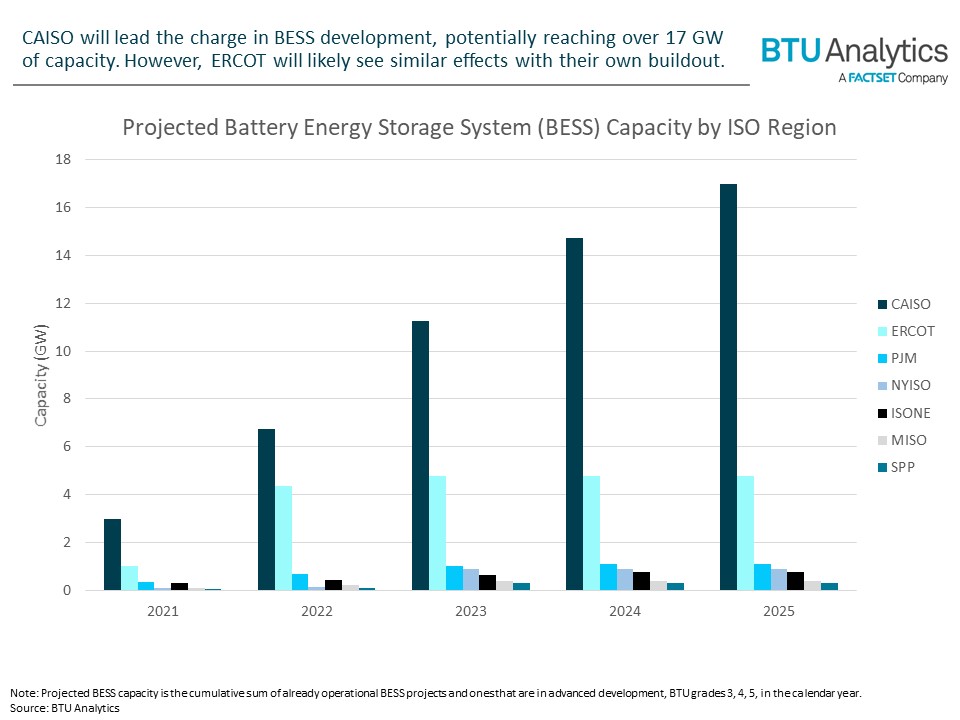

Beyond CAISO’s borders, other ISOs share a different outlook on future BESS operations, as shown below.

Although CAISO has the highest amount of BESS capacity across the seven ISOs, ERCOT has a substantial amount in development with operations capable of reaching over 4 GW by the end of this year. ERCOT holds the highest development of renewables in the U.S. with over 40 GW of solar and wind in operation and 36 GW in the development pipeline. Given the availability of resources and persistent transmission congestion, ERCOT could see an impact greater than that of CAISO. Including speculative BESS projects in early and mid-development phases, ERCOT could reach capacities of up to 44 GW in 2025, compared to the respective capacity for CAISO of 41 GW. If the currently queued projects all come to market, the energy market in ERCOT will be drastically different than today.

By 2025, ERCOT will find itself in a similar position as CAISO. We may not see the same magnitude of effects in the other ISO’s unless significant capacity additions are announced. In the meantime, CAISO and ERCOT will be in the spotlight to showcase what role energy storage will have in developing the next phase of the energy grid. How will growing storage resources affect ERCOT and its reserve margins? We’ll take a deep dive into the implications to ERCOT’s energy-only market in a future Energy Market Insight.