Despite a cold start to winter, natural gas prices have plummeted to $2.66/MMbtu in February. The rapid decline followed record breaking natural gas production and a warm December and January. As a result, coal to gas switching should be a hot topic again this summer. BTU Analytics reviewed coal to gas switching potential in 2016 and 2017. Even with significant gains in market share, coal to gas switching is still relevant in the current market. Reporters highlight how large coal plants are retiring each year. Name plate capacity retirements sound great. However, when capacity is compared to actual generation from those facilities the result is underwhelming. Today’s Energy Market Commentary will provide an update on coal plant utilization and natural gas pricing relationships to the real potential for economic coal to gas switching.

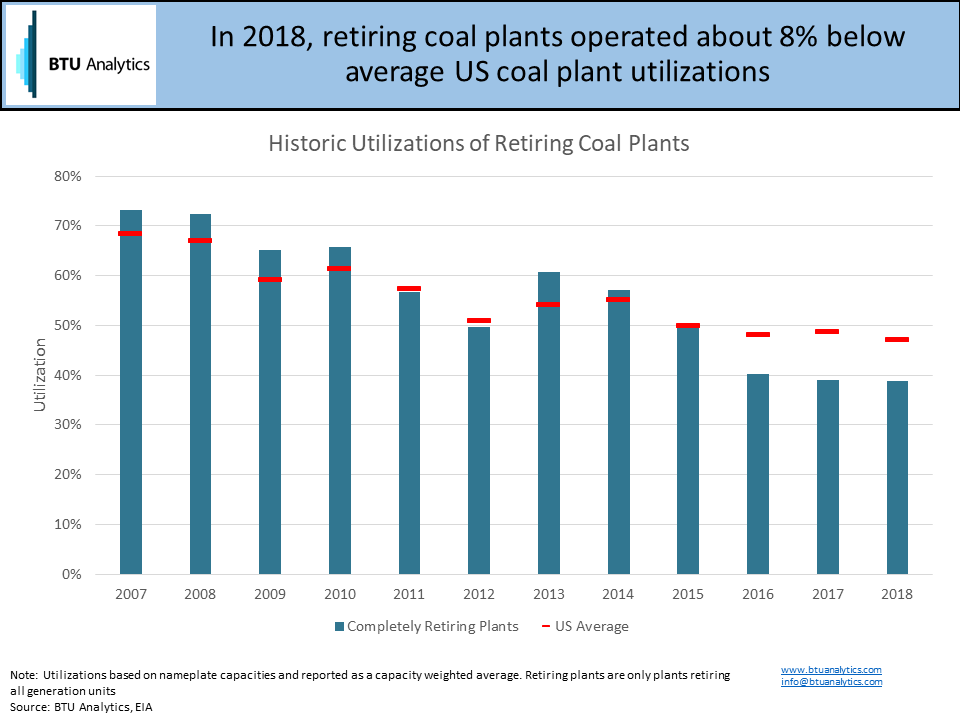

In 2019, seven coal plants are set to completely retire. The plants combine for 3 GW of capacity. Additionally, 14 coal plants announced retirements over the next decade. The additional plants represent 8.6 GW of name plate generation capacity. However, the natural gas power generation gained by these retirements will be lower than nameplate capacity. The plants are being retired due to decreasing utilization. The decline in utilization results generally from low US natural gas prices. From 2007-2011, the retiring plants operated at or above the US average utilization for a coal plant. Now the group of retiring plants operate at less than 40% of nameplate capacity. The average US coal plant operated at just under 50% utilization in 2018.

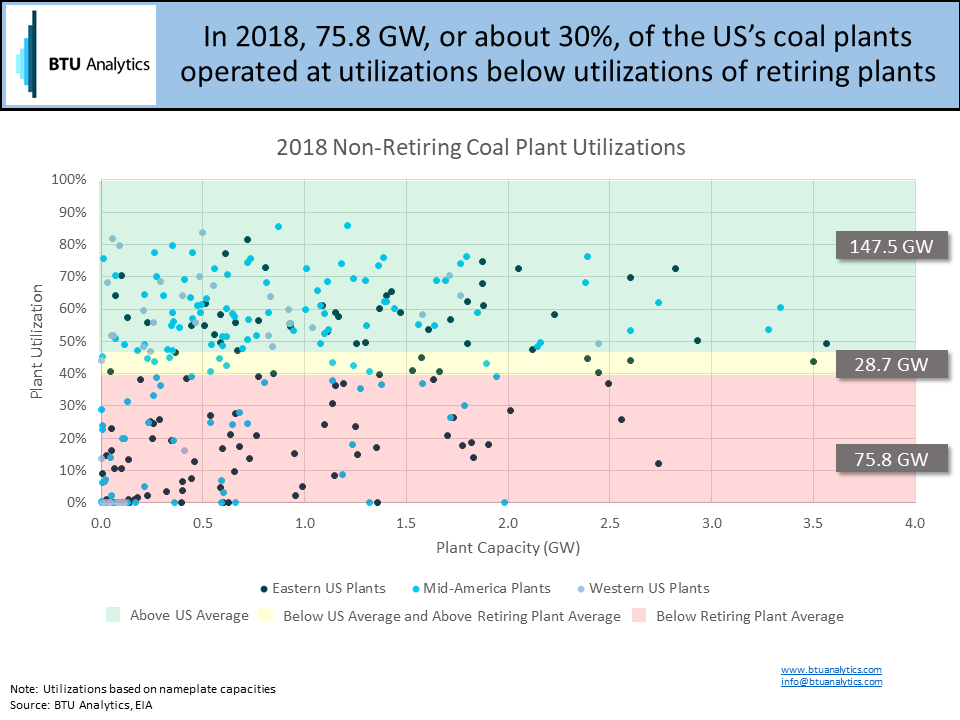

The chart below compares 2018 active coal plant utilization to retiring plant utilization. In 2018, 147.5 GW of active coal plant capacity operated above the average US utilization of 47%. Plants operating at high utilization are unlikely to exit the market in the short term. However, 75.8 GW of active coal plant capacity operated with utilization below 39%. These plants are operating below the average utilization for retiring plants in 2018. The low utilization plants account for 30% of active capacity and could be at risk for retirement. Another 28.7 GW of capacity operated below the US average utilization in 2018 at 47%.

The plants operating below the US average are potentially on the path to retirement as well. This sounds like a lot of capacity that could be back-filled with natural gas fired generation. However, all the potential name plate capacity at risk is running below 50% utilization diminishing the future gains to natural gas.

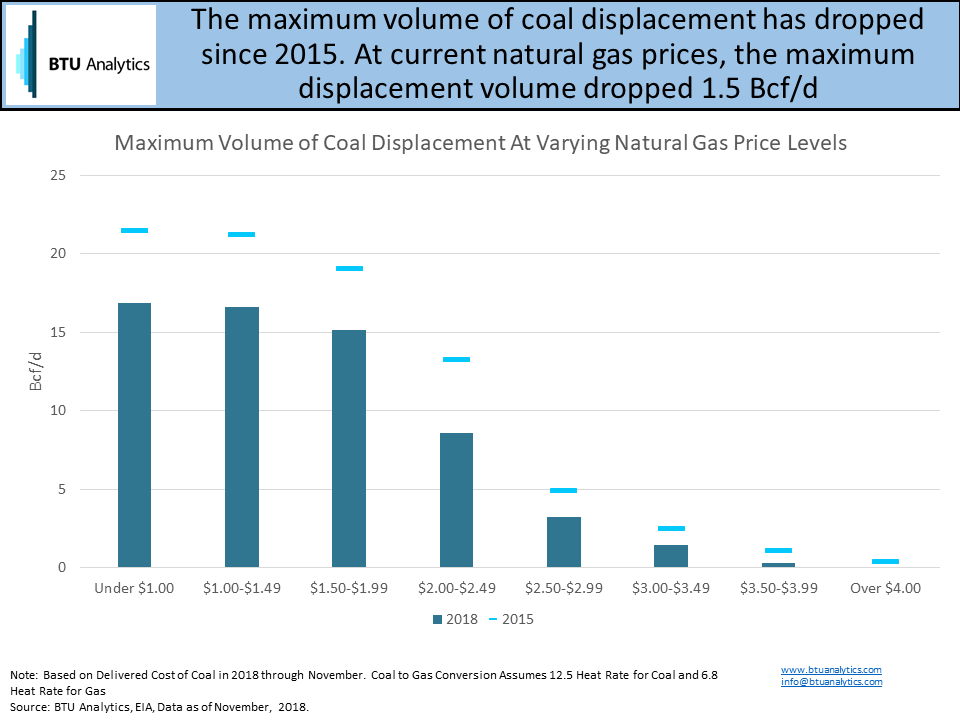

Generally, economics drive coal to gas switching in the short term. Regions where the delivered cost of natural gas falls below the delivered cost of coal generally see an uptick in natural gas fired generation. The graph below illustrates the economic switching potential for natural gas at various pricing levels for natural gas based on the actual delivered cost of coal. Over the last ten years, the maximum potential volume of coal displacement declined due to falling coal consumption in the US. At current price levels ($2.50-$2.99), the maximum switching potential has dropped 1.5 Bcf/d since 2015. At lower price levels ($2.00-2.49), the maximum switching potential dropped to 8.6 Bcf/d in 2018, down by over 4.7 Bcf/d since 2015.

Throughout February, Henry Hub has stayed within the $2.50 to $2.99 price level, falling from over $3.00/MMBtu in January 2019. BTU Analytics expects natural gas prices to remain weak this summer in part due to record-high production levels. At current price levels, the maximum potential for switching is 3.2 Bcf/d. If prices fall into the $2.00-$2.49 bucket, that maximum potential increases to 8.6 Bcf/d. Complete switching though is highly unlikely due to power system reliability requirements and system constraints.

Heading into summer 2019, retiring coal plants and falling natural gas prices increase potential for coal to gas switching. Looking forward, retiring coal plant capacity does not create equal natural gas plant capacity to replace it in part due to the trend of lower coal plant utilization over time but also the impact of increasing renewable generation in the US. To stay up to date with BTU Analytics’ views on the US power generation mix, request a sample of our Henry Hub Outlook.