Natural gas prices are low, gas storage levels are at an all-time high, and winter has started off much warmer than normal across the US. Factor in the Clean Power Plan (CPP) finalized in August, aimed at cutting carbon pollution from power plants, and it’s clear to see that natural gas is poised to take even more power generation market share away from coal in 2016 as coal to gas switching continues.

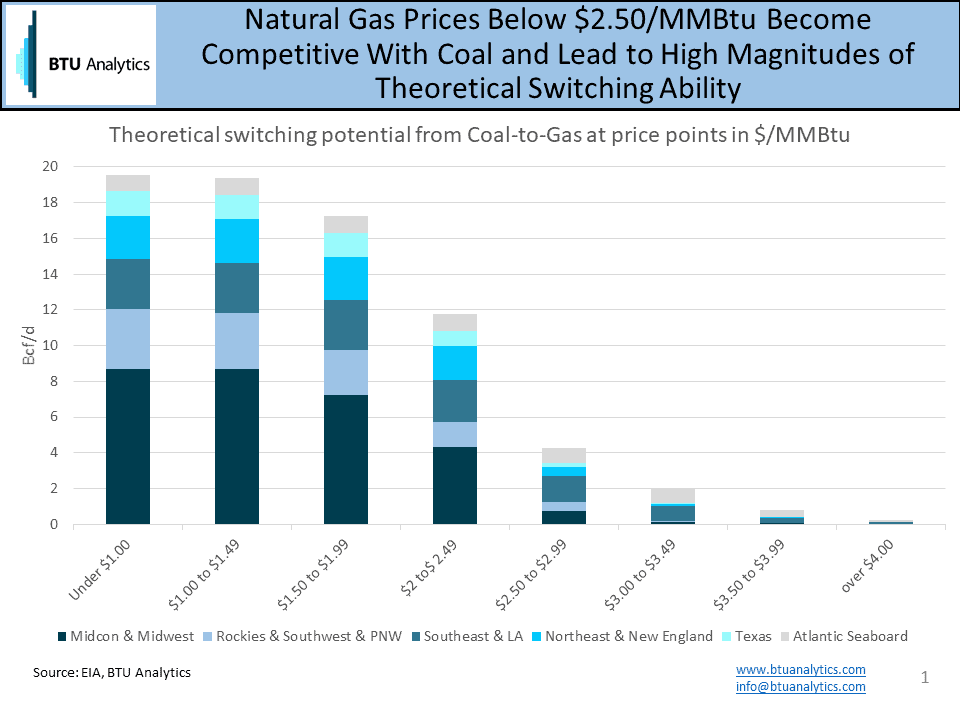

Coal has long been our preferred source of cheap energy, though natural gas prices falling and stabilizing below $2.50/MMBtu make gas a very competitive fuel source for power plants even without the new CPP regulations. But at what price levels do we really start to see this coal-to-gas switching take place? The chart below shows the theoretical switching potential for coal-to-gas as a Bcf/d energy equivalent vs natural gas cost in $/MMBtu and broken up by BTU Analytics’ regions. This chart is generated by using the average year to date delivered cost of coal in 2015 and converting on an energy equivalence basis using the reported heat content. At gas prices above $3.00/MMBtu very little switching from coal-to-gas feedstock will take place. However, as gas prices drop below the $2.50/MMBtu mark, natural gas is able to begin replacing coal as the low cost energy source.

The magnitude of these replacements is dependent on the region, with the Midwest and the Southeast showing the highest theoretical potential for coal-to-gas switching. Some Southeast states source expensive Appalachian coal and have the advantage of few pipeline constraints making them an ideal location to switch to gas volumes. In the Midwest, which largely sits in the MISO footprint, economic dispatch and ample spare capacity allows for easy switching to the cheaper energy alternative. This is bad news for the already hurting coal producers as they see more lost revenue and increased competition.

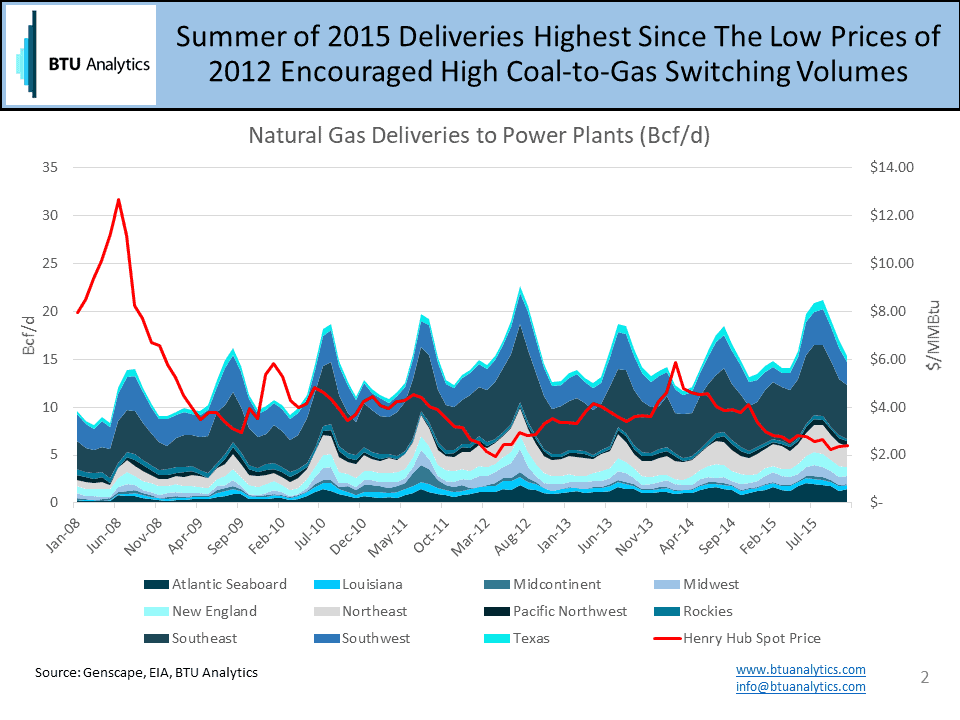

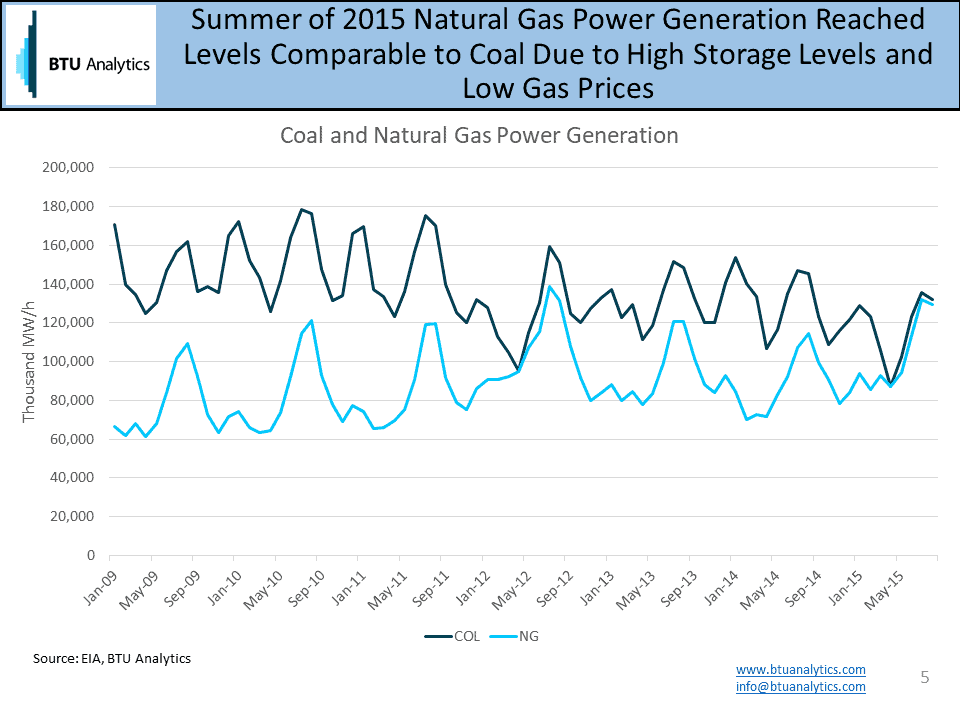

An increase in natural gas power burn was already seen this summer with deliveries to power plants almost 3 Bcf/d higher than the summer of 2014 as shown below. These high levels were last seen in 2012 when a warm 2011/2012 winter led to high storage numbers causing gas prices to crash in the spring. However, in 2012 prices rebounded by September and a normal 2012/2013 winter helped correct the previous year’s storage problem. Fast forward to today. Storage levels just reached a record high of 4.009 Tcf last week, and a month of the winter season is already behind us in which we saw no withdrawal. A warm winter will leave us with above average storage levels next spring and unless new demand sources materialize, the downward pressure on gas prices will continue.

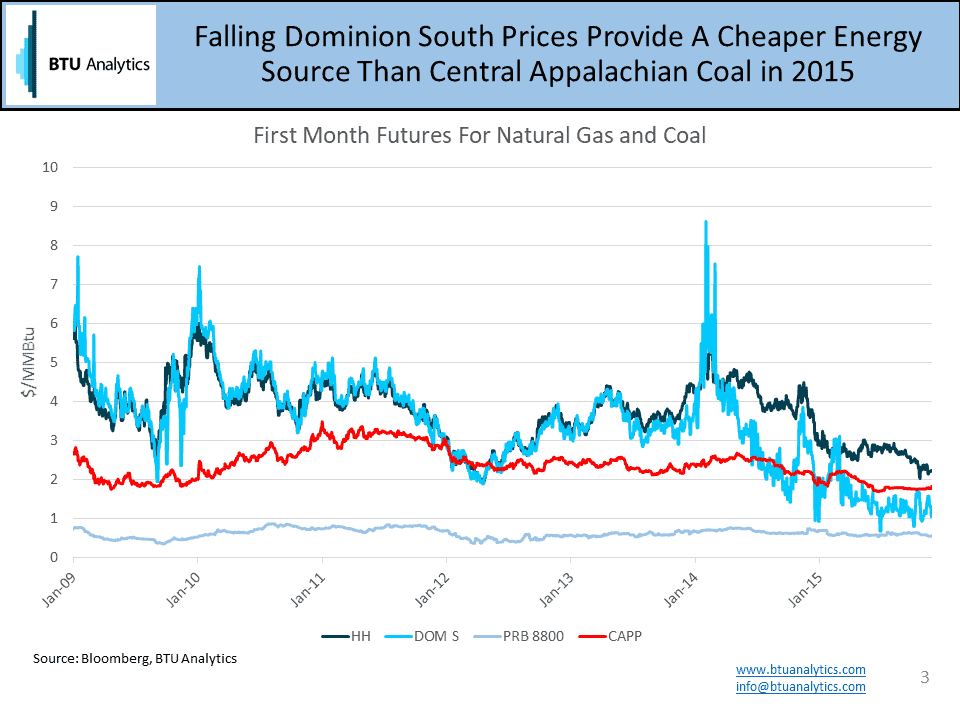

To draw a stronger correlation between 2012 and today’s situation, we can compare the historical first month futures for natural gas and coal in $/MMBtu. The high deliveries of 2012 are due to Henry Hub gas prices dipping below the Central Appalachia coal price, encouraging higher than average coal-to-gas switching. While the spread between HH and CAPP has narrowed in 2015, HH gas prices have yet to fall below CAPP coal again. However, Dominion South (the common price point for Appalachian supply) futures did drop below coal this summer as seen below.

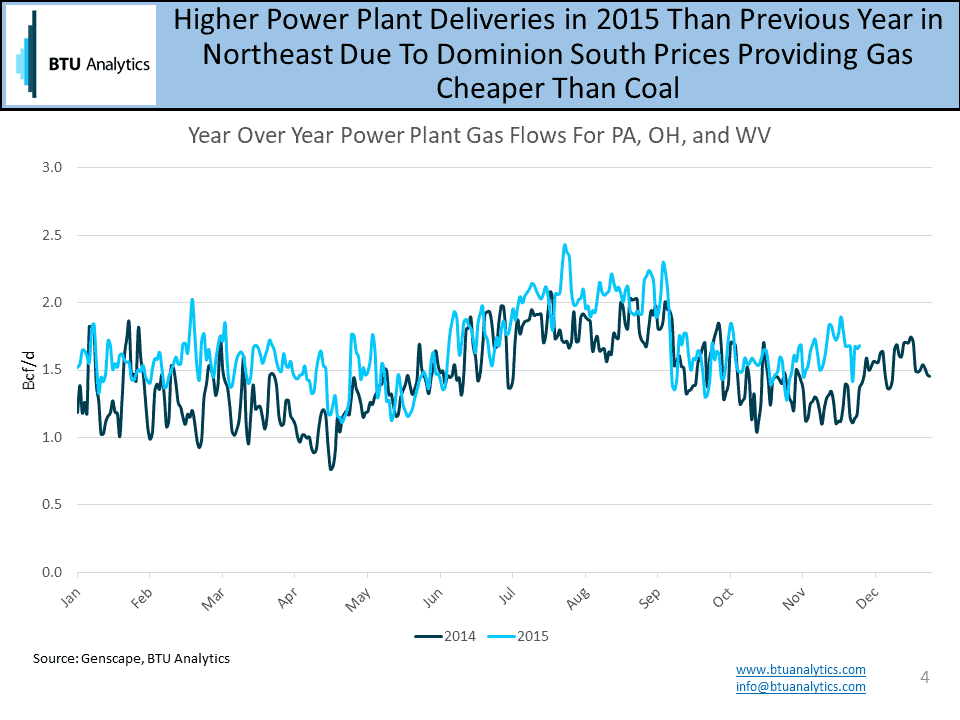

With a clear price advantage of gas over coal in the Northeast we would expect to see increased gas flows to power plants in that region. A year-over-year analysis for PA, OH, and WV shows that 2015 levels are significantly higher on average than the previous year. 2015 YTD averages for power plant deliveries were 0.2 Bcf/d higher than 2014 and 0.18 Bcf/d higher than 2012 levels. Even with coal prices dropping steadily over the last year, Dominion South gas at or below $1.50/MMBtu will remain competitive. The ability and scale of coal-to-gas switching in the US will depended heavily on regional characteristics and prices, pipeline constraints, coal quality, and seasonal demand.

A prolonged environment of low gas prices will expedite the coal-to-gas switching process as coal based power plants face fuel cost competition. Looking at the historical natural gas and coal power burns through time, 2015 has seen significant changes in the stack. For the first time, more power generation is coming from natural gas than from coal.

In 2016, 3.5 GW of coal power is planned for retirement and over 15 GW was already retired this year. Producers are struggling as coal prices continue to fall and new regulations increase costs. The CAPP price has dropped to $40/st from $60/st a year ago and is far from the $80/st value of 2011. Many of these power plants will be repurposed or replaced to burn gas in the next five years as coal is phased out as the majority energy source. Going forward, expect to see cheap natural gas holding the largest portion of power generation in the US.

This is just one of the many topics we’ll cover at our upcoming What Lies Ahead conference to take place on February 4th in Houston, TX. Click HERE for more information and to take advantage of discounted pricing.