Starting this year power plants in Pennsylvania will have to start accounting for their emissions and buying offsets through the Regional Greenhouse Gas Initiative (RGGI). The first cap-and-trade (or rather cap-and-invest as it’s typically branded) system in the US for carbon dioxide emissions, RGGI is an initiative 11 states (currently, excluding PA) in the northeastern part of the country, which requires fossil fuel powered generators greater than 25 MW to acquire CO2 credits for their emissions. The effects of RGGI are debated, and while we will see CO2 emissions in the participating states have certainly been on the decline, the amount to which the RGGI program itself can be credited with the decline is up for debate. Today’s insights will give an overview of RGGI and how the program has, or hasn’t, effected emissions.

To start, RGGI is comprised of 11 states, excluding PA. These are Connecticut, Delaware, Maine, Maryland, Massachusetts, New Hampshire, New Jersey, New York, Rhode Island, Vermont, and Virginia. An important note here is that while the RGGI auctions began in 2009, our analysis will start in 2012. At that time, Virginia and New Jersey were not participating in the program. New Jersey joined (again) in 2020, and Virginia joined in 2021. Each quarter, an auction is held for allowances, and a plant is required to have all allowances needed to offset emissions over the course of the three-year control period. Allowances can be traded over the counter, but we will focus on auction results for the time being.

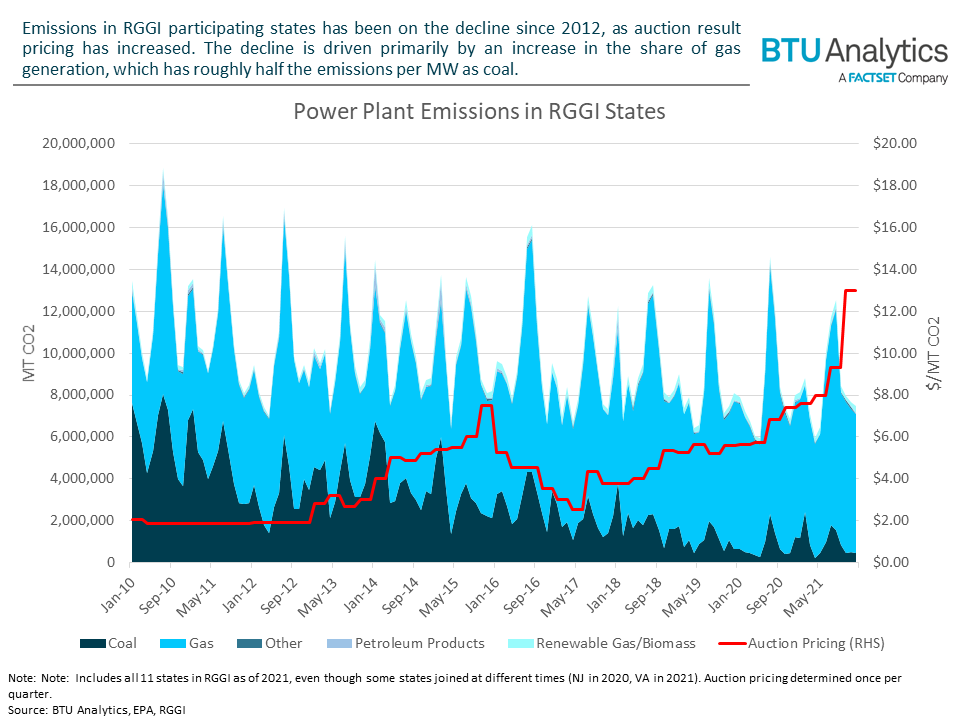

Below is an overview of the auction pricing results, as well as emissions by fuel type for the 11 participating states. To make an accurate comparison, New Jersey and Virginia are included for the history shown.

Overall emissions have been declining since the share of gas generation, which emits roughly 0.5 MT of CO2 per MW, has been increasing, pushing out coal generation which has a much higher emissions intensity of around 1 MT of CO2 per MW. However, skeptics of RGGI would be right in pointing out that while emissions in the RGGI states are down 31% when comparing 2010 emissions to 2021 emissions, the Lower 48 US is down 29% over the same time period, indicating the initiative likely hasn’t had a disproportionate effect on reducing emissions.

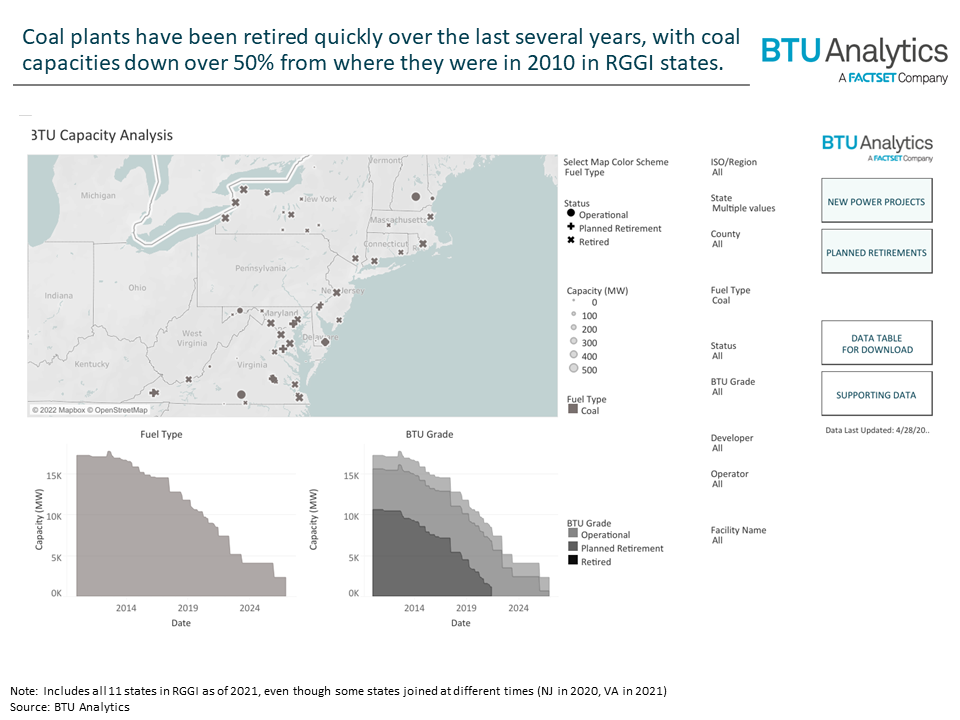

The more likely reason for the decline in emissions is the retirement of coal capacity, shown in the graphic below for the RGGI area, driven primarily by low regional natural gas prices over the last decade.

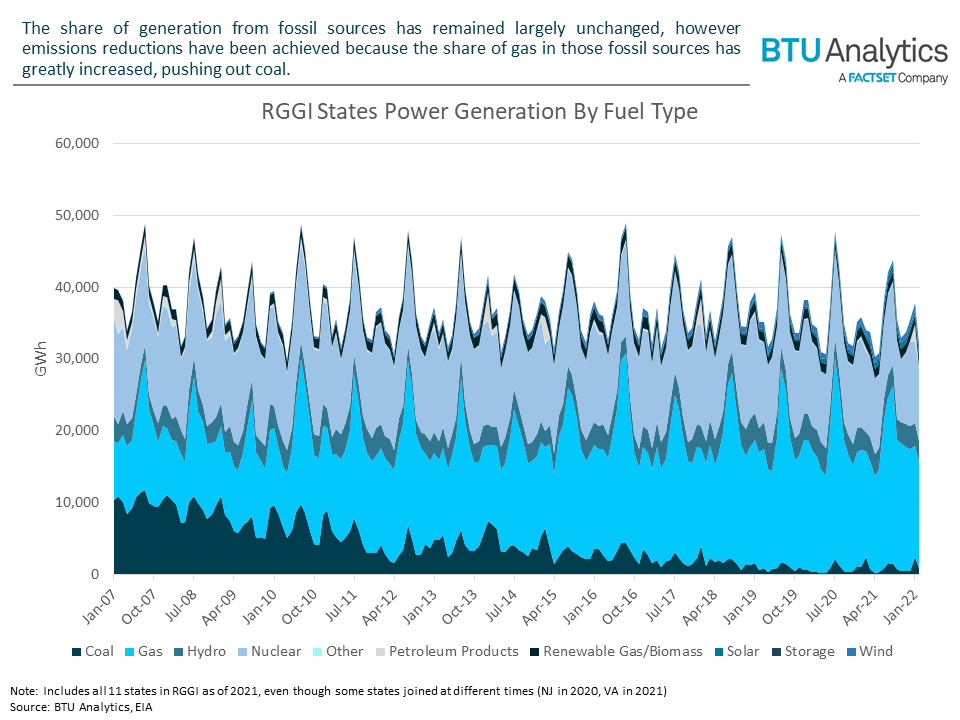

However, we do not expect this trend of declining emissions to continue. The below graphic shows the breakdown of generation by fuel type for RGGI states.

With coal playing only a marginal role in the region’s generation, emissions reductions in these states are likely at a stalling point until low or zero carbon generation sources are added to the stack, like major offshore wind developments.

Given the above information, future auctions in which the price of CO2 rises will have little to no impact on reducing emissions in the short term, since the region doesn’t have the ability to switch to lower cost fuel sources if CO2 allowances increase in price. Historically auction prices were low enough that impacts to power pricing were negligible, typically around a dollar or two per MW at most. However, if RGGI prices continue to increase until offshore wind facilities get built, the only effect would be an increase to power pricing. At the current auction rate of $13.5/MT, this would likely add around $6-7/MW to power pricing given gas as the marginal generation source, which would be significant to a region which sees average monthly prices range from around $20-50/MW.

RGGI has other benefits, and states have the option to use the revenue to reinvest in their communities and fund various programs, which can positively impact those states. However, RGGI’s usefulness as a system to reduce emissions has not made a meaningfully greater impact on emissions reductions in the region than the US in general has seen over a similar time frame, though it could start to have an impact on increasing power prices. As RGGI drives increases in pricing, regional dynamics and incentives will adjust, creating new market opportunities that we will explore in future Insights.