Last week, the Bureau of Offshore Energy Management (BOEM) announced it is seeking public comment on two Wind Energy Areas in the Gulf of Mexico. This signals further acceleration towards the Biden administration’s goal of 30 GW of offshore wind capacity by 2030. While BTU Analytics has recently discussed how offshore New England wind production will affect ISO-NE, today’s Energy Market Insight will see how Gulf of Mexico wind will affect the ERCOT and MISO power markets.

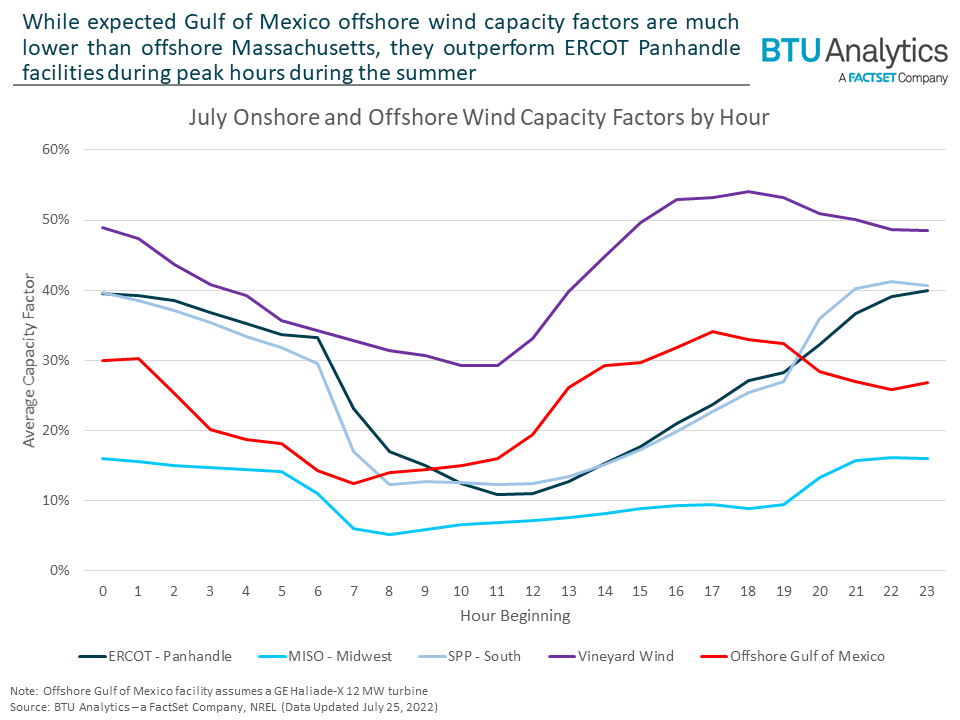

Wind development in the Gulf of Mexico is still in its earliest stages. While the areas identified are off the coast of Galveston (546,645 acres of potential development) and Lake Charles (188,023 acres), how much of that acreage will interconnect to ERCOT or MISO is unknown. Wherever the interconnection happens, it will not change the fact that offshore wind dynamics will be materially different to onshore facilities. For example, July capacity factors, shown below, are expected to be lower than ERCOT Panhandle facilities in the early hours but higher when peak load sets in in the evening.

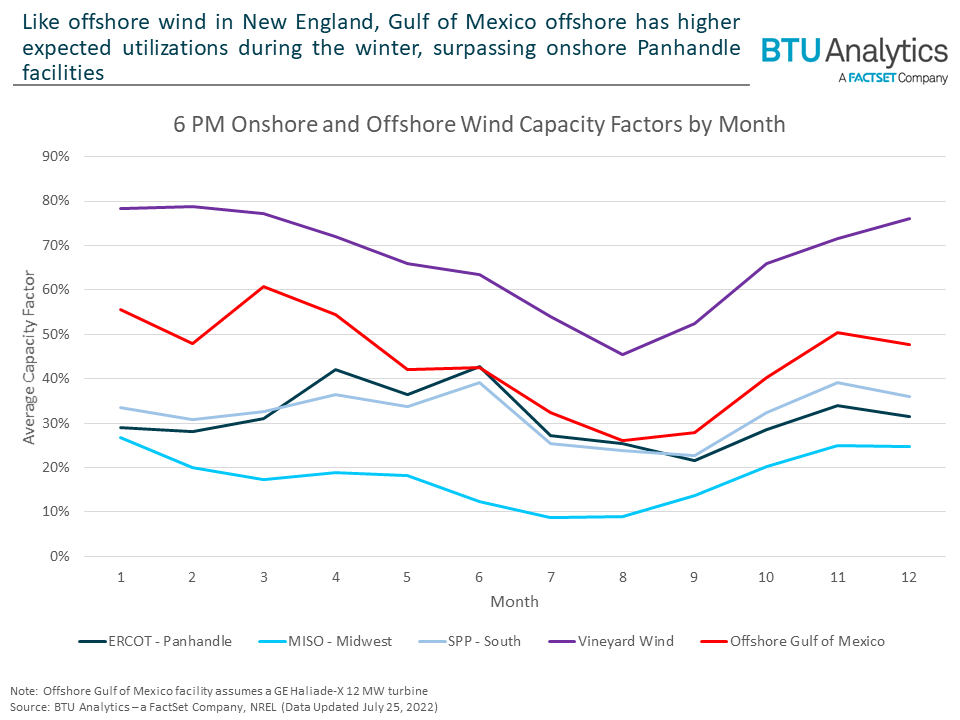

Performance during daily peak load times will be crucial. While much lower than an offshore New England facility like Vineyard Wind, peak hour winter capacity factors will be significantly higher than onshore facilities. This means as solar generation rolls off, gas generators will not need to ramp as hard to meet evening demand.

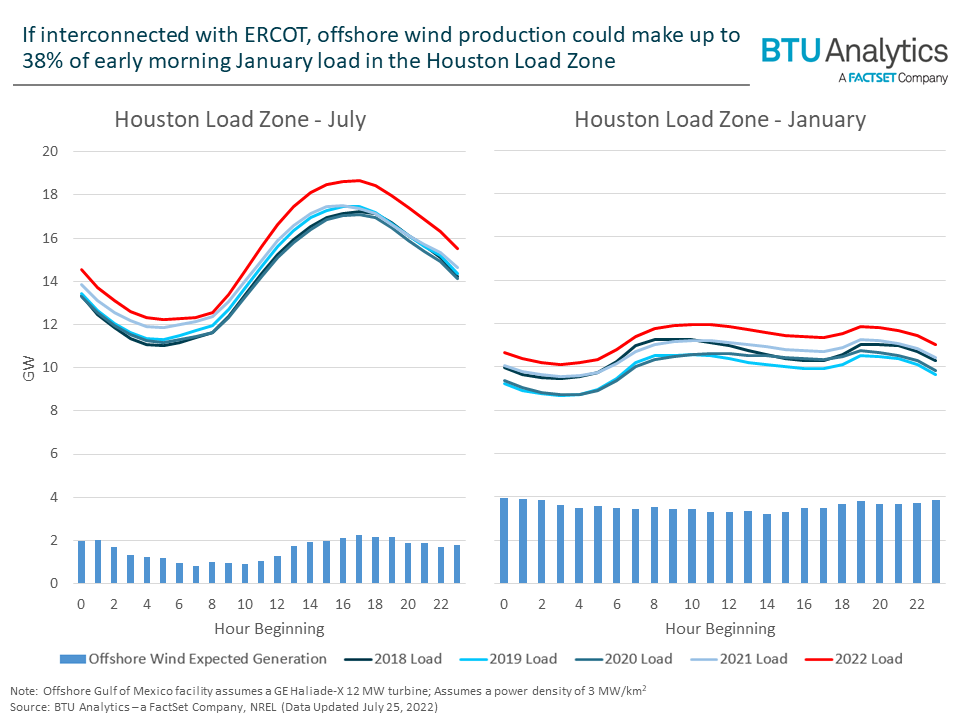

What does this mean for generation? Take the larger of the two Wind Energy Areas 40 miles off the coast of Galveston. Assuming this area will interconnect into ERCOT’s Houston Load Zone, we can compare potential generation to regional load to understand what percentage of load could be met from new offshore facilities. Due to inflated load and dipping seasonal capacity factors, expected generation in July only reaches about 15% of Houston’s 2022 load.

The opposite is true for winters. During that time, load is depressed and capacity factors are expected to be higher than in the summer, leading to offshore generation making up almost 40% of Houston’s 2022 load in the early morning hours.

Typically, ERCOT isn’t known for being an exciting market to watch in the winter. However, offshore generation will bring two things that are likely to be felt acutely during winter months: increased hour-to-hour and day-to-day volatility based on wind conditions and muted requirements for baseload thermal generation. Both mean increased pressure on traditional thermal assets, especially if they are not able to ramp during times of offshore production volatility.

Obviously, details will develop as the BOEM moves closer to holding auctions for identified lease areas. How many leases will be up for auction and what are their potential capacities? Where will potential facilities interconnect? What are the implications to congestion? Who will potential offtakers be? Whatever the answers to these questions (and many more), it is guaranteed that offshore wind in the Gulf of Mexico will represent another development for ERCOT and MISO power markets.