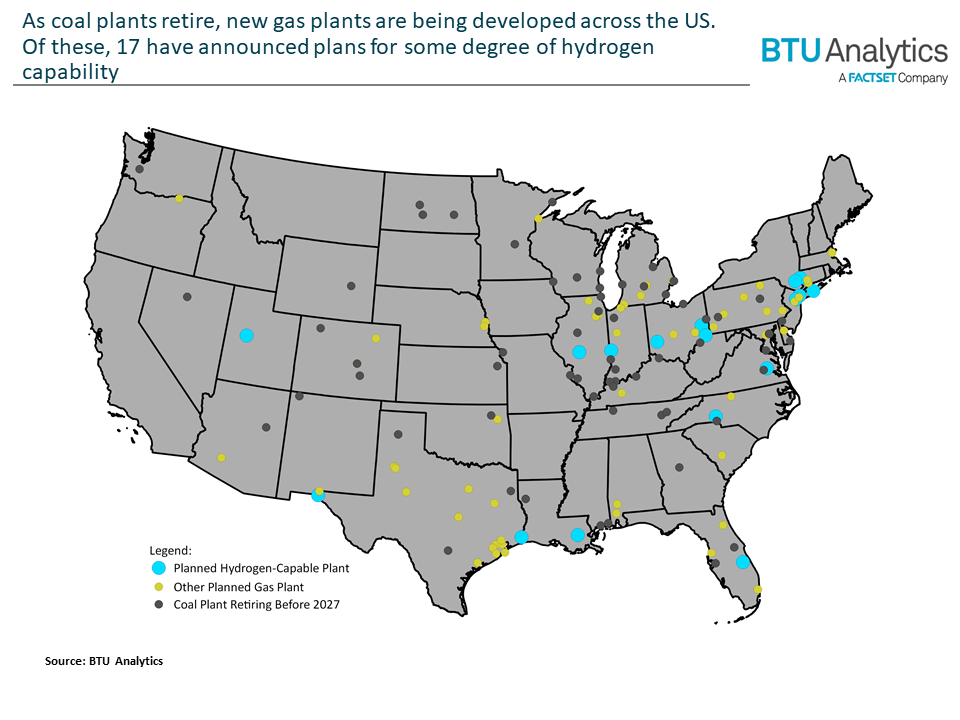

Hydrogen infrastructure has recently attracted political support and several billion dollars in private investment, with one goal being to enable net-zero power generation while retaining the flexibility of thermal generation. Though still an experimental technology, advancements have brought that goal closer to a reality for utility-scale power. The newest gas turbines can burn an increasingly high percentage of hydrogen blended with natural gas, and manufacturers expect a conversion to 100% hydrogen fuel will soon be commercially feasible. BTU Analytics currently tracks 10 US facilities with announced plans to blend hydrogen into their fuel-stream. Additionally, 7 other power plants have publicly expressed interest in the option of blending in the future. Today’s Energy Market Insight looks at the current outlook for hydrogen-blending and its implications for natural gas demand.

The interest in hydrogen-gas power has dovetailed with several market trends discouraging new fossil fuel plants. Firstly, utility demand is shifting, and developers are having to incorporate greener technologies to win contracts. This was the case with the Intermountain Power Project which struggled to sign contracts with Southern California utilities before hydrogen provided a path to net-zero emissions. Secondly, ESG-motivated goals have pushed power giants such as NextEra and Entergy into outlining their own net-zero plans, which frequently mention hydrogen as a critical component. NextEra is actively developing at least one hydrogen-capable plant, while Entergy has committed to hydrogen-blending at one new plant and may convert three others to blend hydrogen. Lastly, public sentiment has produced regulatory and political roadblocks for new gas plants in certain regions. Having faced public backlash, the Astoria Gas Peaker Plant in Queens, NY is now being pitched on its potential to eventually incorporate hydrogen.

As these pressures have mounted, turbine manufacturers have been working to provide the technology necessary to equip hydrogen projects. Mitsubishi Power has guaranteed all new turbines to operate with 30% hydrogen blends by volume. GE and Siemens have followed suit with claims that their largest turbines can operate at blends above 30%. Some smaller turbines, particularly aeroderivative models, are being marketed with hydrogen capability above 50%. Of course, these ratings are dependent on configurations with combustors, fuel injectors, and fuel lines specially designed for hydrogen-blends. However, the turbine represents one of a plant’s largest capital assets and its fuel-flexibility significantly lowers the bar for conversion.

As hydrogen-capable turbines enter the mainstream, it raises the odds that more new plants will adopt hydrogen. Of gas power capacity additions which BTU rates as likely to be completed in 2022, only 10% is publicly planned to be hydrogen-capable. Yet, another 78% of capacity is known to be furnished with turbines that are hydrogen-capable according to manufacturers. Despite other obstacles, including difficulties of production, distribution, and storage, the generator technology for hydrogen power is becoming more commonplace, and the exogenous factors described above may push developers of future projects to consider hydrogen optionality as a hedge.

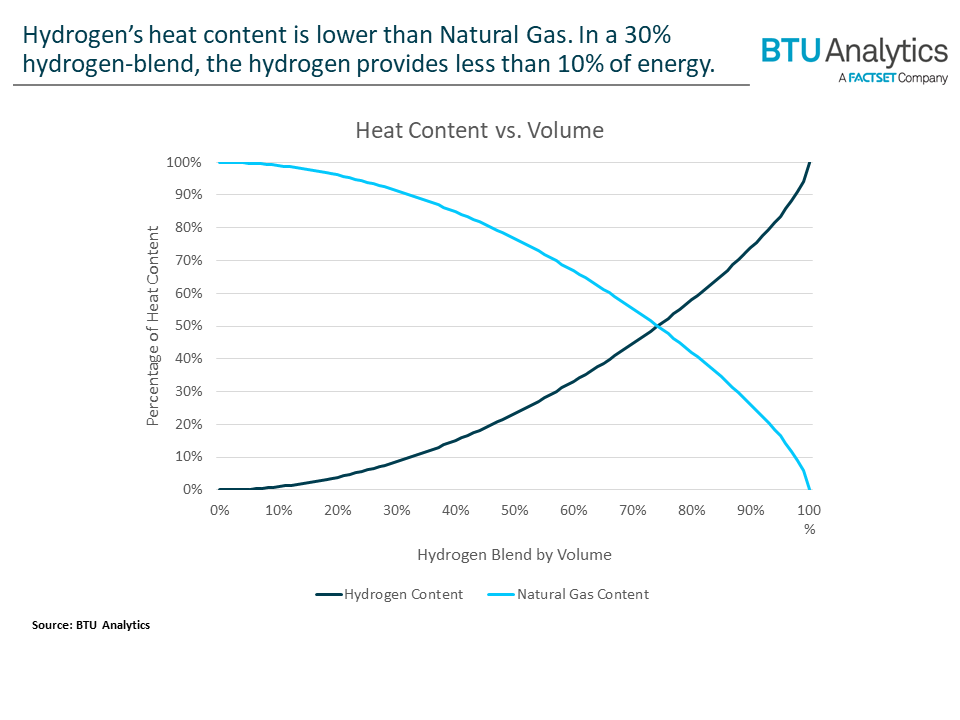

However, analysis of the 17 hydrogen-capable plants which have been proposed suggests that hydrogen is unlikely to significantly impact demand for natural gas. Critical to understanding why is the difference in heat content between the two gases. By volume, natural gas contains about 3.3 times the energy of hydrogen. Therefore, in a fuel-blend containing 30% hydrogen by volume, the hydrogen is providing less than 10% of the energy. It would take a 75% blend before hydrogen would make up the majority of the fuel’s heat content. For this reason, the extent to which hydrogen would displace natural gas is non-linear, with little impact when the blend is low. Also working in favor of natural gas, plant operators plan to gradually phase in hydrogen, such that the plants would burn primarily natural gas during the first decades of their operation.

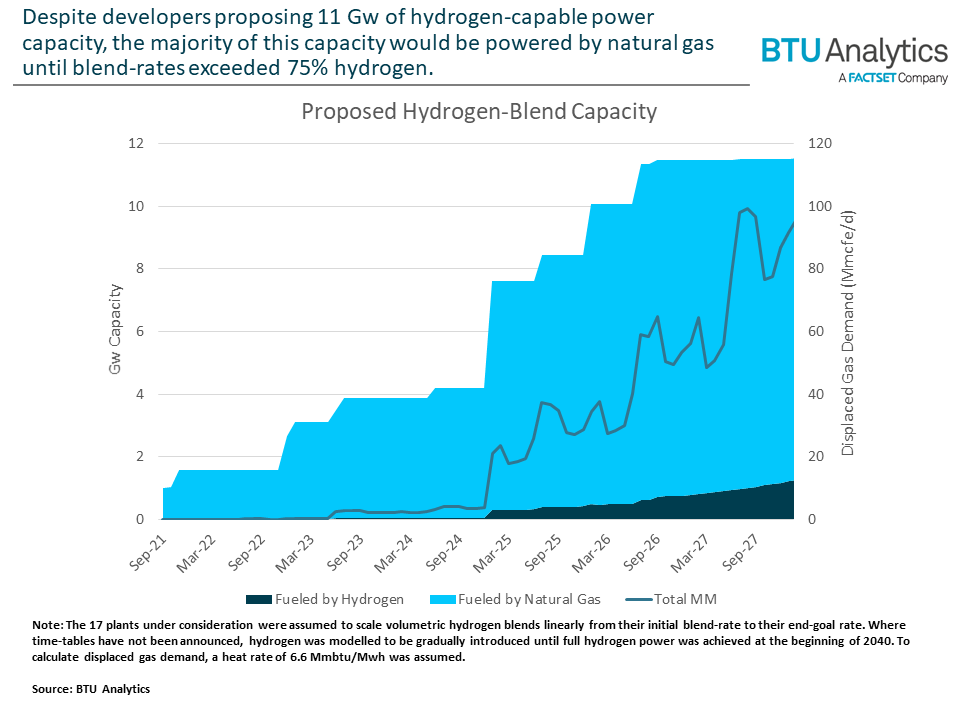

Modelling the generation of the 17 proposed plants, including each facilities’ timetable for increasing its blend-rates, BTU found that by 2027 only 770 Mw of the proposed 11 Gw capacity would be effectively fueled by hydrogen. Even assuming that these newer plants would run at capacity factors well above average, such that more than 60% percent of capacity was dispatched during summer months, the 17 plants would burn only 74MMcf/d less natural gas in 2027 than were they to run without hydrogen. This would decrease BTU’s power burn forecast by only 0.2% in 2027.

Of the 17 hydrogen-capable projects cited here, most are early in development and may never be built. Those that are recently completed or currently under construction are primarily considered as gas plants. For hydrogen-blending to displace a meaningful portion of gas demand, investment in power plants far beyond what has so far been announced is required, in addition to the other infrastructure necessary to supply hydrogen fuel. Given this analysis, BTU’s base forecast does not incorporate hydrogen-blending as a driver for gas demand.

BTU’s Long Term Gas Outlook next published in November, provides a detailed forecast of North American natural gas production and demand over the next 30 years. Additionally, BTU offers the Power View platform for insights into planned and operational power capacity in the US.