With the holiday season in full swing and Christmas around the corner, naturally, the mind turns toward coal. However, recent history for coal in power generation has been far from cheery. But instead of dwelling on the past, let’s look towards the future and what we can expect from coal-fired power generation over the next few years.

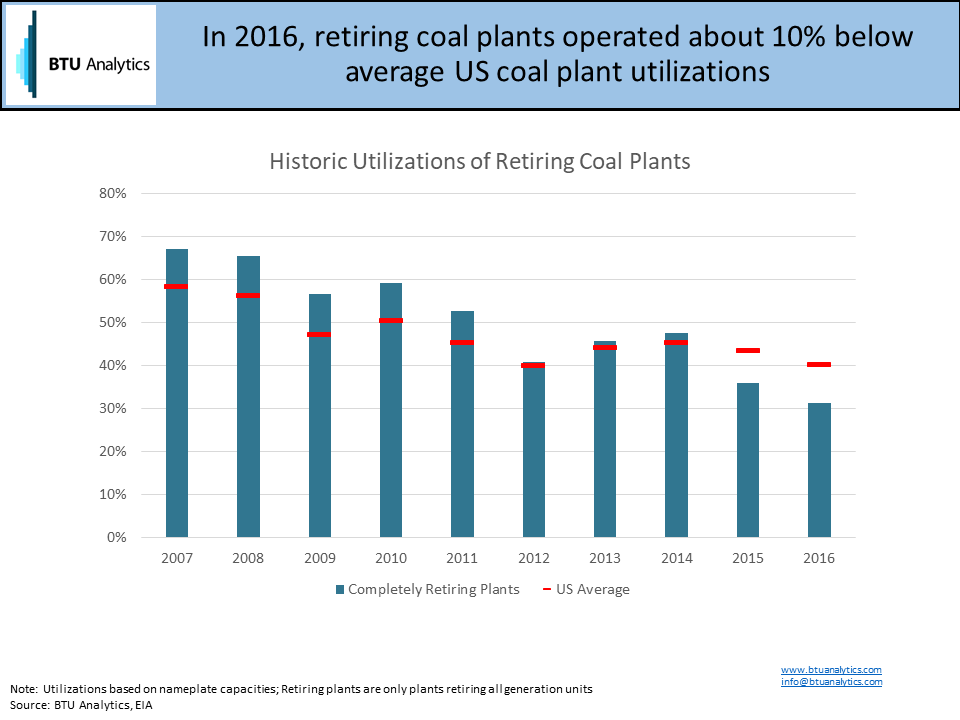

It’s easy to get caught up in headlines of big nameplate capacity coal retirements, but the first thing to realize is that retiring US coal plants operate at much lower utilizations than the average coal plant. So, when seeing those headlines, a distinction must be made between retiring capacity and retiring generation. As shown in the graphic below, in 2016, coal plants with announced retirement dates were operating a full 10% below the average US utilization of 41%.

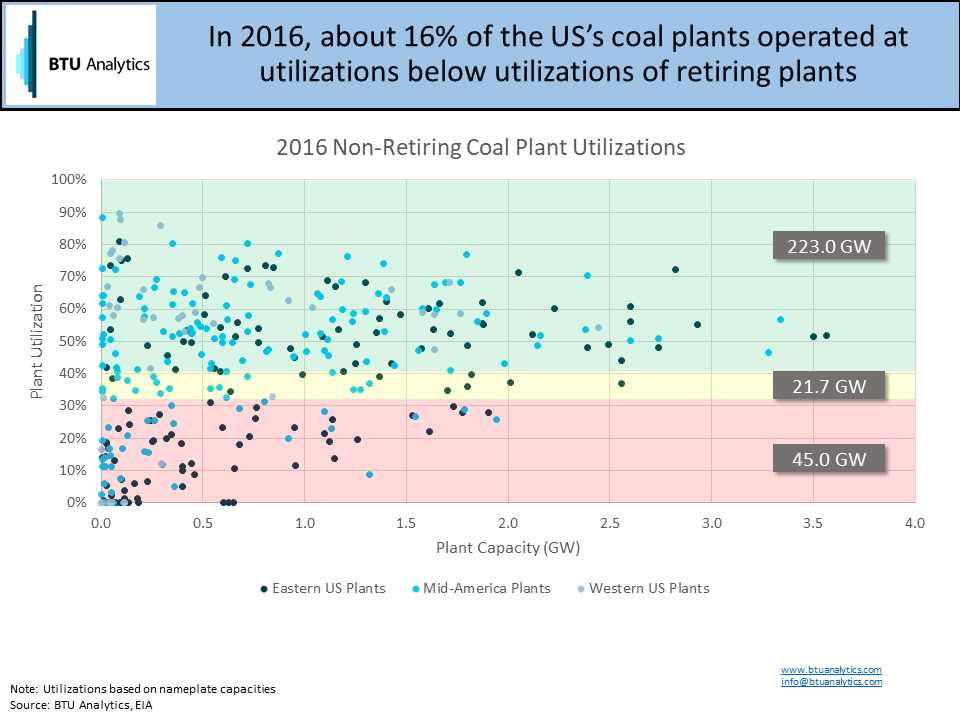

But the bars above are only the plants that have announced that they are officially retiring. It turns out EIA generation data shows that there are more than a 100 non-retiring coal plants that are operating at dangerously low utilizations, below the 31% utilization that officially retiring plants were operating at.

Does this put them at danger of retiring? It is hard to say without considering the specific circumstances surrounding each plant, but it’s hard to argue that low utilizations are sustainable in the long-term. The graphic below plots existing non-retiring coal plant utilizations into three areas: below retiring plant utilizations (red), above retiring plant utilizations but below US average utilizations (yellow), and above US average utilizations (green).

It turns out that in 2016, about 45 GW of (nameplate) capacity that has not announced retirement was operating below levels of retiring plants. That’s about 16% of the US’s coal fleet. What does that look like on a more granular level?

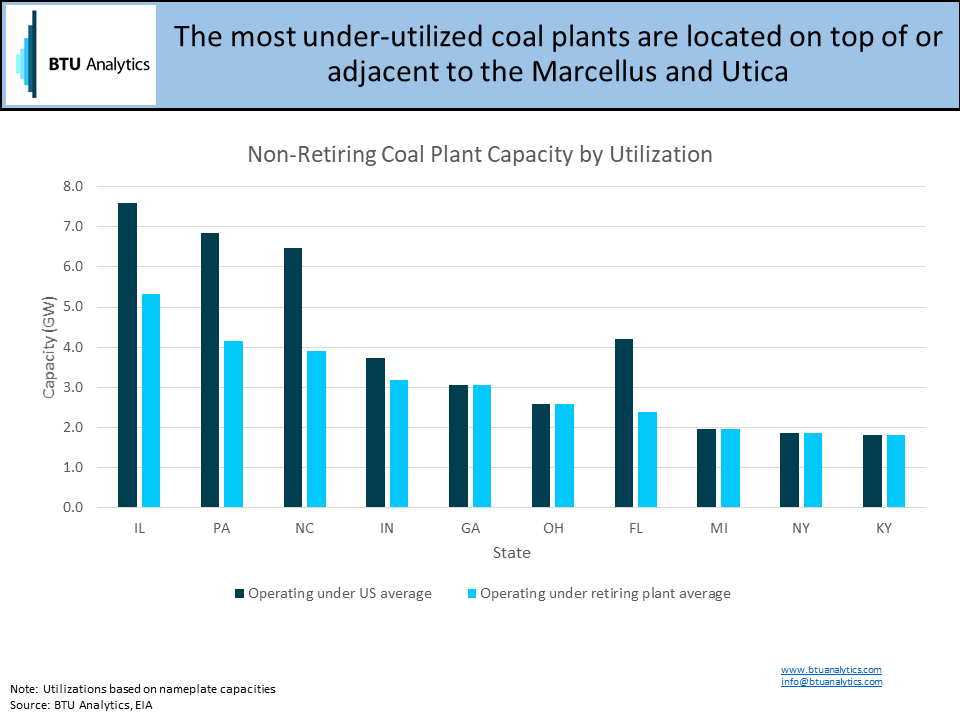

Breaking those plants down by state shows what we probably should have expected: the coal plants most at risk come from areas that are on top of or adjacent to the Marcellus and Utica, where we have seen prolific natural gas production growth over the past few years.

With numbers like that, it’s easier to understand why some in the industry are ramping up pressure for new pricing structures for generators that would reward resiliency, such as Secretary Perry’s recent Notice of Proposed Rulemaking to FERC. Nevertheless, even if pricing structure were to change, the wheels of government move slowly, so be on the lookout for more headlines in 2018 of further coal retirements.

For more on changing dynamics in the power market and how they will affect natural gas power burn, check out our new power and renewables section each month in our Henry Hub Outlook. Also, want to know what’s in store for the future of natural gas, including the second wave of LNG facilities and the impacts to demand from electric vehicles? Register now for our upcoming conference to find out What Lies Ahead.