For the last five years, the Permian has changed oil and natural gas markets by unleashing a torrent of cheap oil and natural gas on the market. Prices plummeted into the negatives and infrastructure struggled to keep pace. Like the hydrocarbon markets, power markets, specifically ERCOT, have felt the force of booming Permian activity. Today’s Energy Market Insight will look at that impact and how power markets can help electrify and decarbonize hydrocarbon infrastructure.

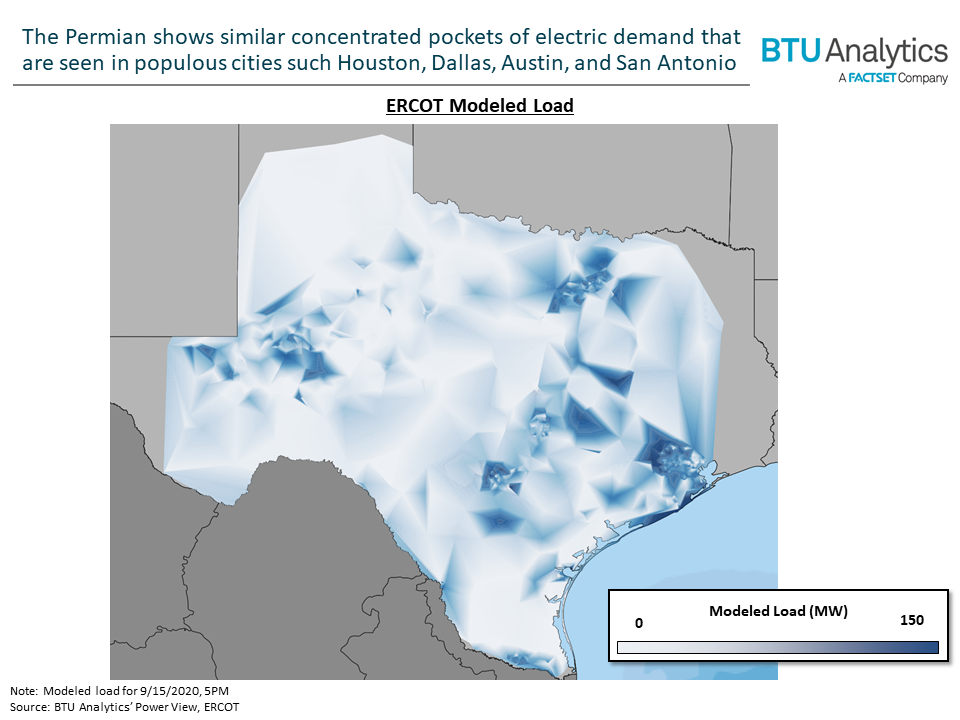

First, let’s start with the electricity landscape in Texas. Below is a snapshot of hourly load (electricity demand) across ERCOT. Darker colors represent areas of high load, while lighter colors are areas with less load. Major cities in Texas are easy to pick out: Houston, San Antonio, Austin, and Dallas in the eastern half. However, in the west, the Permian shows similar concentrated pockets of electricity demand that are seen in the populous cities to the east.

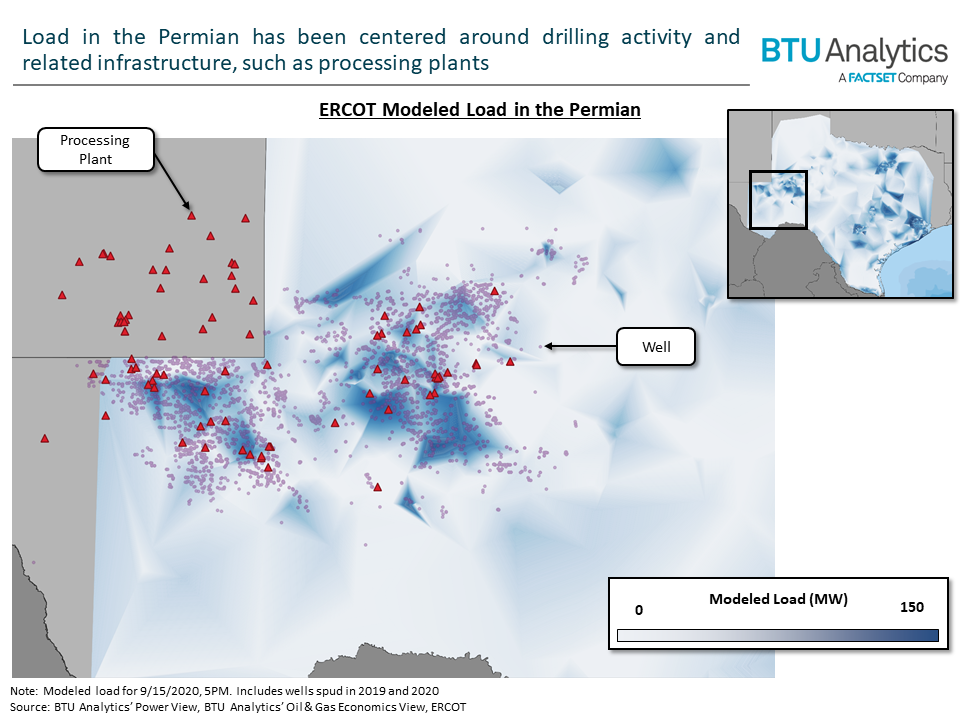

Zooming into the Permian and overlaying recent drilling activity and natural gas processing plants, show that pockets of electricity demand are co-located. Over the next 5 years, the Permian is expected to increase oil production by 2 MMb/d and gas production by 8 Bcf/d. These increases in production will continue to cause concentrated pockets of electricity demand in West Texas.

This concentrated electricity demand has coincided with aggressive growth of electricity generation from wind and solar developers. In fact, this area of West Texas accounts for 80% of ERCOT’s solar capacity and about a quarter of ERCOT’s wind capacity. This has presented an opportunity to electrify and decarbonize some hydrocarbon infrastructure, as illustrated by Energy Transfer’s agreement to purchase renewable energy for its Tippet processing plant in Pecos county from Recurrent Energy’s Maplewood 2 Solar Project or their recent PPA with SB energy in Lamar county.

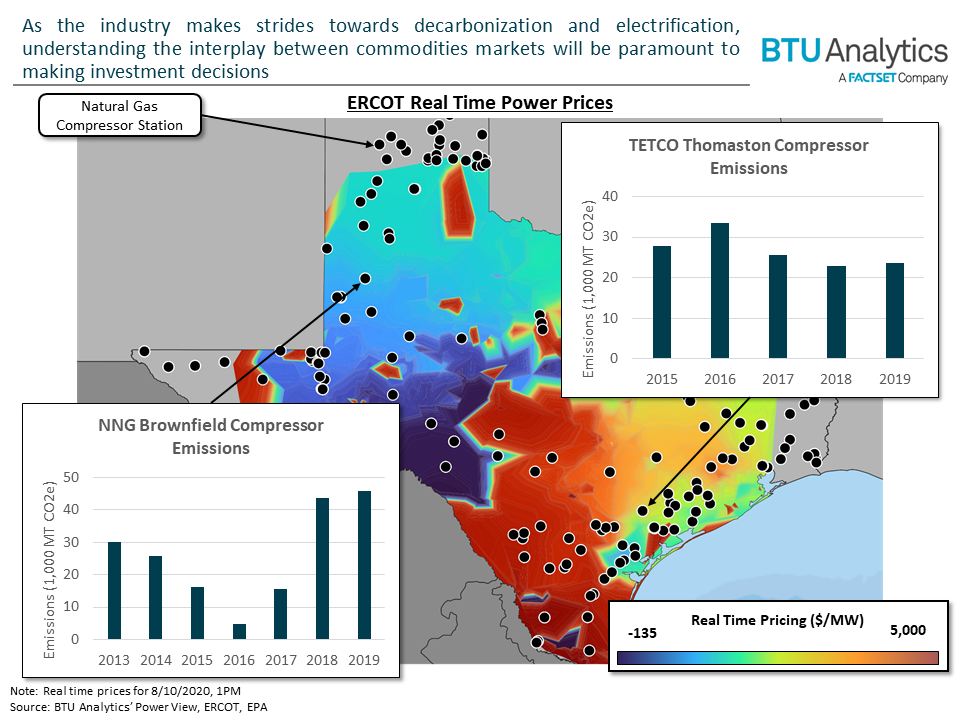

Natural gas compressor stations provide another route for potential electrification, where the power pricing dynamics around each compressor station will help to determine the best route to electrification. The map below shows a snapshot of pricing in ERCOT as well as natural gas compressor stations with associated emission profiles.

Electrification can be achieved in a few ways: build a dedicated generator, tie-in to the grid, or sign a power purchase agreement (as in Energy Transfer’s cases above). In areas with low and/or less volatile pricing, tying into the grid would be the easiest way to electrify a compressor station. However, volatility due to intermittent generation or high pricing due to being on the wrong side of a transmission constraint would suggest having a dedicated generation source, either through a PPA or operated generators, is the best route.

As all industries push towards decarbonization, including the hydrocarbon industry, understanding and evaluating the options presented in the power market will be key. BTU Analytics’ Power View can help you understand these market dynamics at play. For a free trial of our power platform click here.