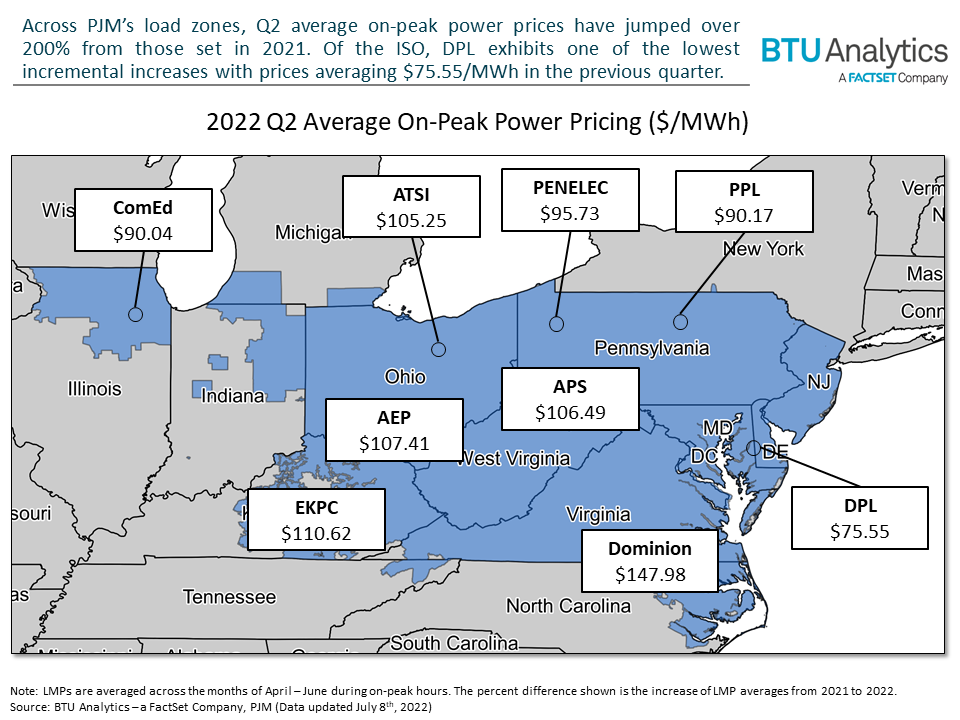

U.S. power prices are on the rise. With the rising costs of natural gas, narrowing reserve margins, and soaring temperatures, it’s no surprise that power prices are increasing. We have already seen mounting pressures in ERCOT and MISO, but PJM is yet another ISO that has seen a surge in power pricing. While system-wide prices have risen to unseasonable highs, not all regions are showing similar signs of drastic price increases. In today’s Energy Market Insight, we will explore PJM pricing and why one region of weaker pricing stands out among the rest.

PJM relies heavily on natural gas generation; the rising costs for gas are a major contributor to the escalated pricing in PJM and across the country. Yet, in the wake of rising temperatures, demand, and fuel pricing, some regions have maintained weaker pricing than the rest of ISO.

We see substantially lower pricing within the Delmarva Peninsula, served by Delmarva Power and Light (DPL). While average on-peak pricing surpasses $147/MWh in PJM’s extreme, DPL maintains an average far below those of its neighboring load zones. The drastic spread begs the question of what dynamics within DPL could foster a lower power price than the rest of the system.

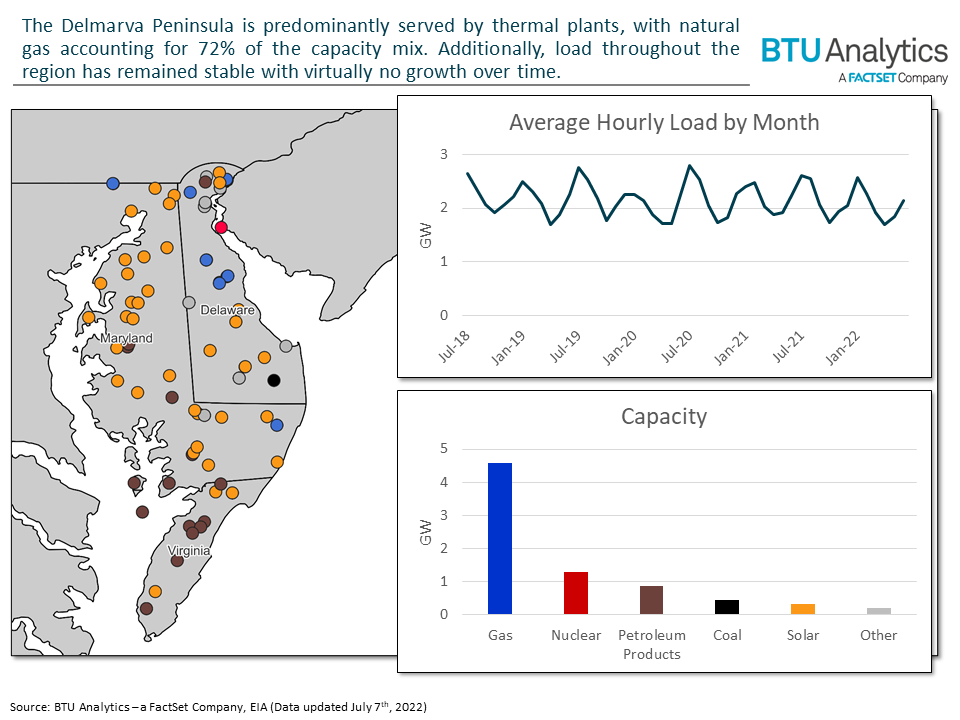

Much like the rest of PJM, DPL load is met primarily with natural gas. Oscillating around 2.2 GW, load in the region is stable and relatively low compared to an entire system load average of 95.2 GW for June 2022. With no load changes and little contributions from renewables, lower pricing is unexplained by the internal dynamics within DPL alone.

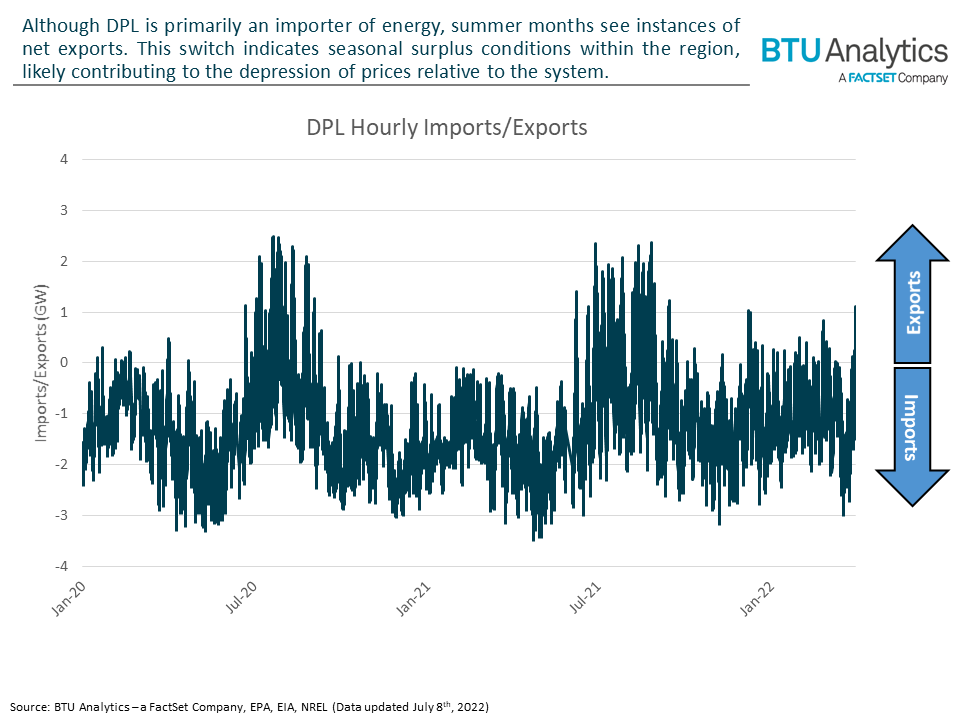

To further understand the pricing spread, we must consider the effects of the rest of the ISO on the region. DPL can interact with the rest of PJM through power transfers and, across the board, is primarily a net importer of energy. However, hourly imports and exports show that DPL becomes a net exporter during summer months.

The switch to net exports is a key indication that the region has excess supply over demand. Moreover, the switch provides insight into how PJM’s dispatch curve plays into the regional generation within DPL. Typically, during times of moderate to low load, demand is met by power flows into the region from more economic generators elsewhere. However, as load increases across PJM, Delmarva’s less economic plants are called on to dispatch to meet local load and export out of the region.

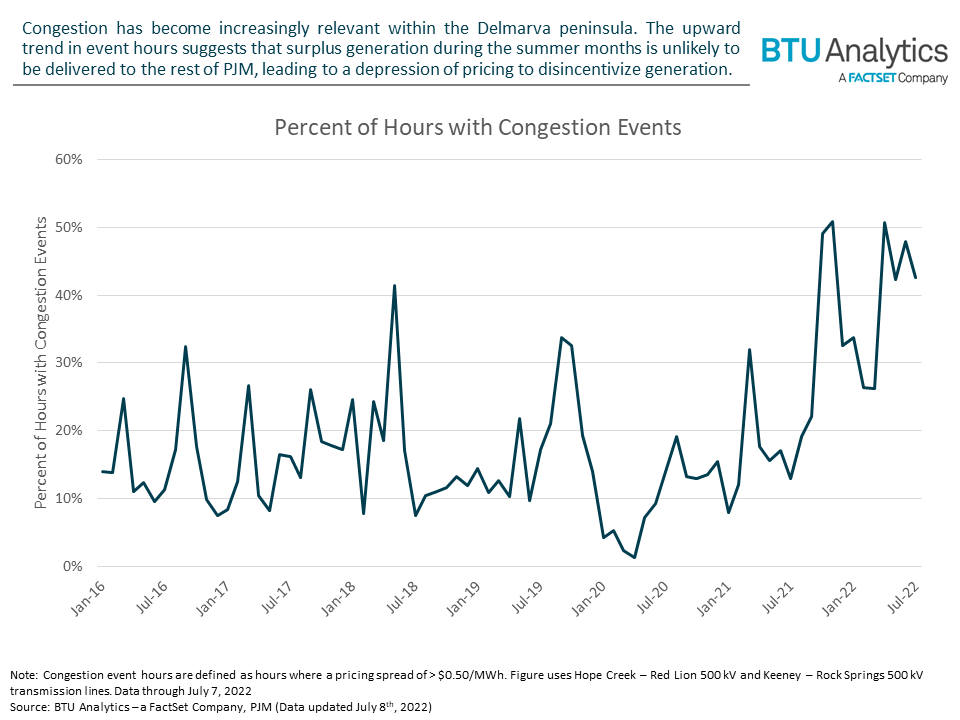

Like other regions across the U.S., this increase in local generation and exports is often met with transmission constraints and congestion. While DPL gas plants are called upon to generate, generation is capped at the limits of the transmission infrastructure. For DPL, both seasonal summer and winter congestion are evident.

More recently, congestion has been increasing within the region. With nearly 45% of hours seeing congestion in May and June, the recent weak pricing is best explained by the increased gas generation encountering increased congestion. Although summer generation requirements allowed for more gas plants to dispatch, insufficient transmission is causing a depression of pricing.

While Delmarva’s weak pricing can be mitigated with new infrastructure and/or exacerbated by a changing fuel mix (Indian River retiring in 2023), the region is just another recent example of how transmission infrastructure can drive a wedge within an ISO. Similar dynamics are happening all over the country (see North Dakota and South Dakota in MISO) and will continue to develop as transmission buildout lags generator investments.