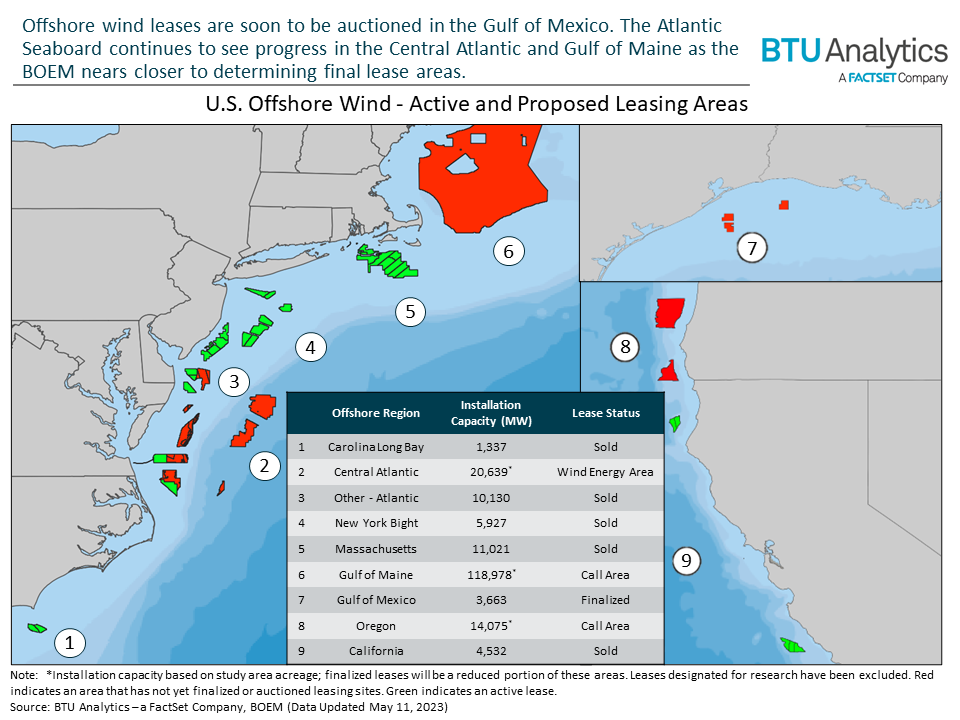

The Bureau of Ocean Energy Management (BOEM) continues to advance their goal of holding seven new offshore wind leasing sales by 2025. Following the most recent auction in California, the BOEM announced a Proposed Sale Notice for three leasing sites in the Gulf of Mexico totaling 301,746 acres. Moreover, progress continues to be made along the Atlantic Seaboard, where the agency has determined eight Wind Energy Areas (WEAs) for the Central Atlantic and solicited commercial interest for development in the Gulf of Maine. A geographic layout of these latest announcements can be seen in the map below, with red areas indicating leasing efforts that are underway and green areas marking an active lease.

The proposed leases in the Gulf of Mexico are expected to be auctioned in 3Q23, bringing total estimated U.S. developable capacity to nearly 37 GW (determined using leasing acreage and an assumed power density of 3 MW/km2). Other areas off the coasts aren’t far behind, with the BOEM timeline planning for the auction of leases in the Central Atlantic and Oregon regions in 2023 and the Gulf of Maine to follow in 2024. With offshore wind development heavily concentrated along the Northern Atlantic, the Gulf of Maine could add sizeable capacity to the already growing buildout of offshore wind in the Northeast.

As offshore wind continues to develop, many questions loom around the impact it will have on regional power dynamics. The Northeast could have the most to gain from offshore wind, as electrification and rising winter load are poised to further stress the reliability of a system with growing natural gas supply constraints. Offshore wind could mitigate some of this winter stress by displacing existing thermal generation and reducing the natural gas volumes needed for the power sector.

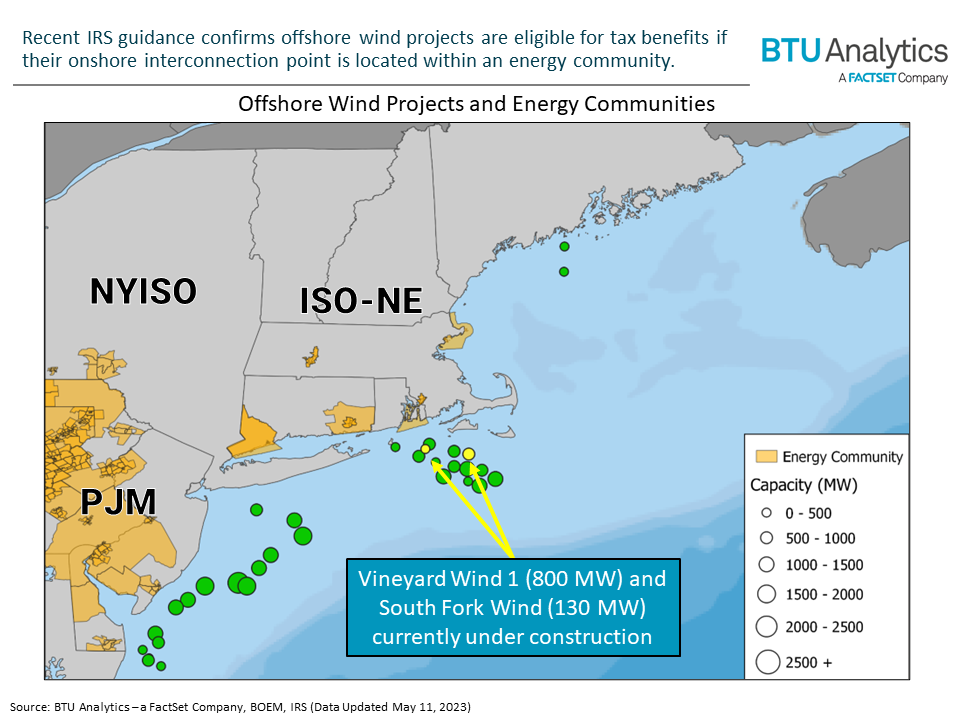

Using BTU Analytics’ Power View, we can see just under 30 GW of projects currently under development off the Northeast coast. However, it is unknown where all this power will ultimately come ashore. The IRS recently announced that offshore wind projects will qualify for a 10% increase in production and investment credits if their onshore interconnection point falls within an energy community. As shown below, the Northeast has numerous energy communities with some bordering major load centers, like Boston.

Driven by enhanced federal tax credits, developers are likely to secure project interconnection points that fall within these energy communities. In the Central Atlantic, this could concentrate power inflows into southern New Jersey and Delaware. For ISO New England (ISO-NE), many offshore wind projects will interconnect in its southern load zones, potentially introducing pricing disparity in a region that typically exhibits little to no transmission congestion.

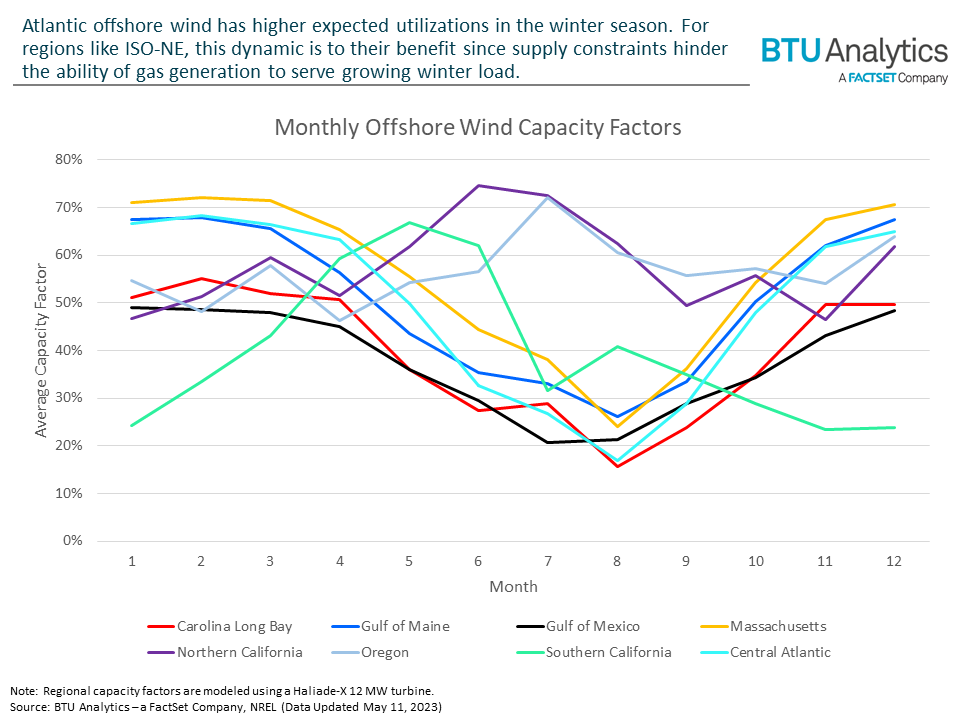

To the benefit of the Northeast, monthly offshore wind capacity factors show that generation will be at its strongest during the winter, providing a potential backstop for regional power generation when natural gas-fired capacity is constrained.

Interestingly, the Pacific Coast differs from the Atlantic and Gulf of Mexico in that offshore wind generation is expected to be at its strongest in the summer months. More summer capability could mitigate resource adequacy concerns for areas like California, where the ISO issued flex alerts in September 2022 to avoid undersupply scenarios. However, the magnitude of impacts along the Pacific Coast is yet to be determined.

The unique performance characteristics of offshore wind resources will help develop its future role in power markets. BTU Analytics has previously examined these dynamics in ISO-NE and ERCOT. However, with development further afield, questions in new regions of the country are being raised. Will development maintain its current pace? How will offshore wind impact the Pacific Coast? Could offshore wind stabilize summer markets in the West? We will look to answer these questions and more in future Energy Market Insights.