With the Democratic presidential primary continuing to pick up, energy policy has come into focus, bringing rarely discussed topics like nuclear power to the forefront. More left leaning candidates, like Bernie Sanders and Elizabeth Warren, have come out against nuclear power, with Warren stating she would wean the US off of nuclear power as part of her “100% renewable and zero-emission” plan. So where does nuclear power stand today and how will planned retirements, and a more extreme full-fleet retirement affect the market?

Today, nuclear power makes up about 20% of the US’ generation mix, with the bulk of plants having been built in the 1970s or prior. As shown in the graphic below, these plants were mostly built in PJM and MISO around market centers in the Northeast and Midwest, respectively.

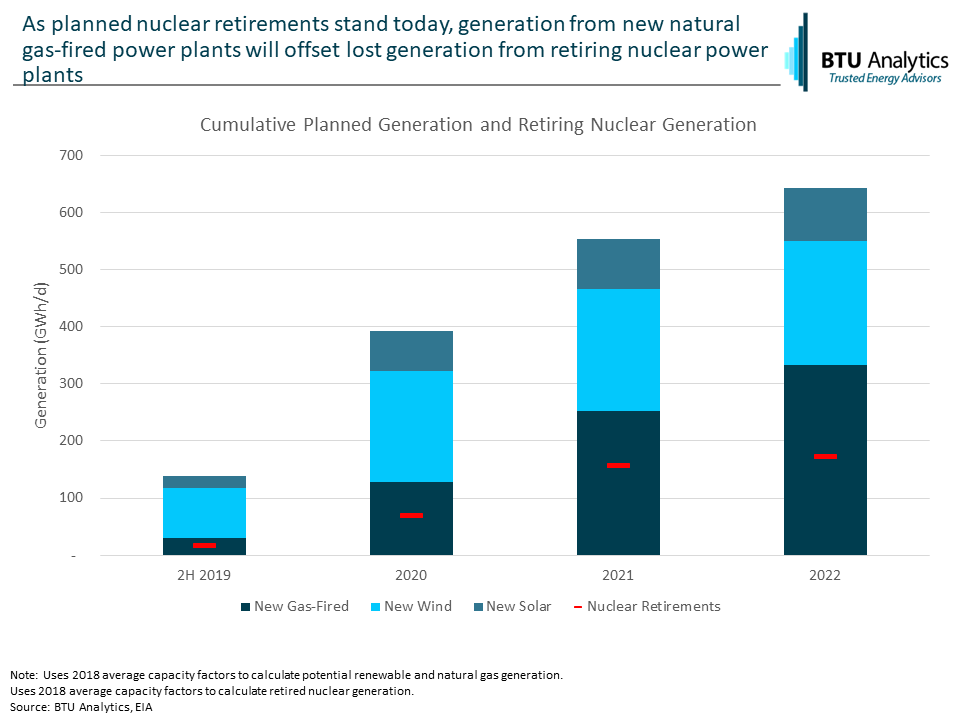

An aging fleet and weak power prices have put financial pressure on nuclear power plants and have caused about 10% of the US’ nuclear fleet to announce retirements. As it stands today, there is about 200 GWh/d (10.4 GW) of generation from nuclear plants slated to be retired by 2022. New potential generation from gas-fired power plants alone would be able to offset that loss in generation, however, layering in potential generation from wind and solar projects shows potential new generation would outstrip lost generation from announced nuclear retirements.

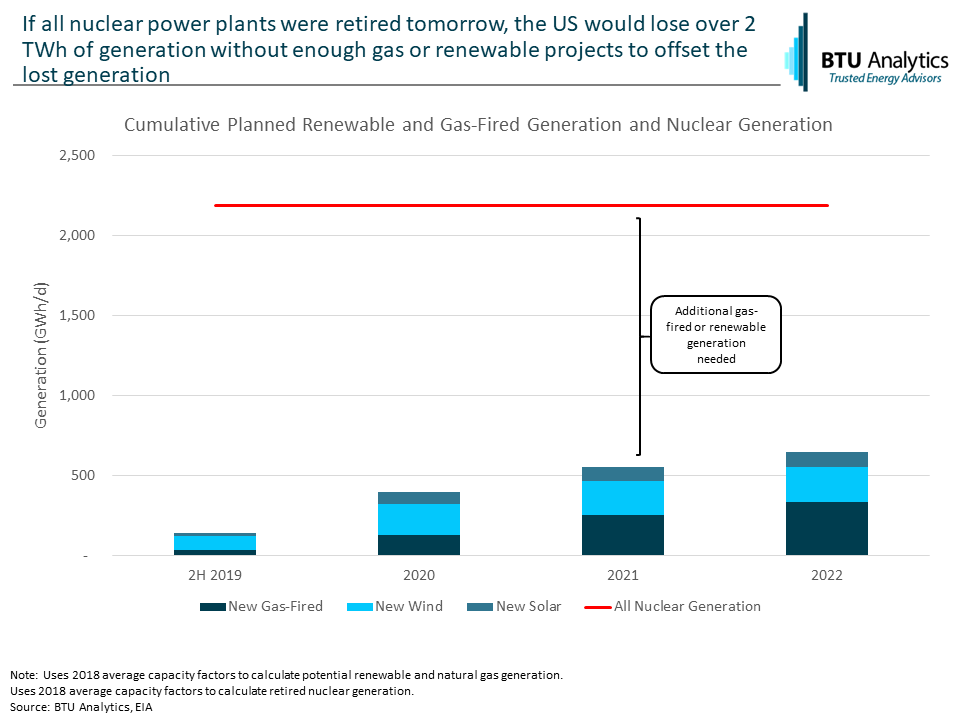

If the US were to retire all nuclear power plants, the story looks significantly different than present-day planned retirements. Retiring all nuclear plants would remove 2 TWh/d (104 GW) of generation from the market. Currently, planned solar and wind projects and natural gas-fired power plants would be unable to replace the total lost generation across the US. This extreme scenario would leave ample room for additional generation from natural gas-fired plants or new renewable projects.

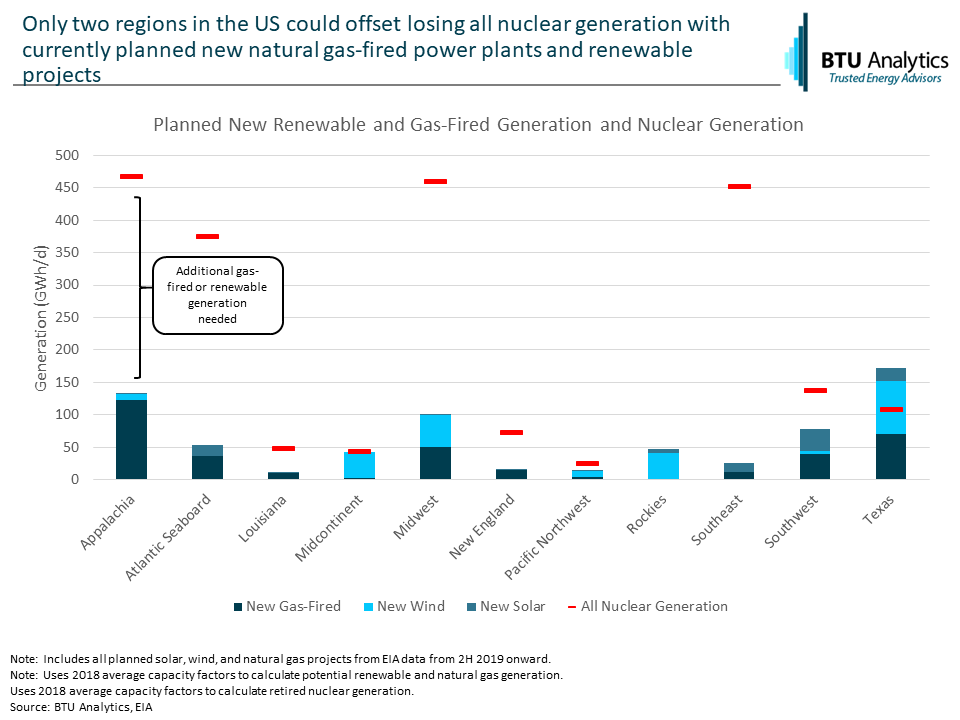

The situation becomes more dire at a regional level. Only two regions of the US would be adequately supplied by new gas-fired and renewable projects if all nuclear power plants were retired: the Midcontinent, where significant generation from new wind projects is planned, and Texas, where both natural gas-fired plants and new wind projects will provide new generation. In Appalachia, the Midwest, the Atlantic Seaboard, and the Southeast, retiring all nuclear power plants would provide significant space for new natural gas-fired power plants or renewable projects to enter the market. Especially in Appalachia, the need for new local power generation could provide upside to the demand constrained Marcellus and Utica production.

While it is unlikely the US will quickly retire all of its nuclear powered fleet, natural gas producers could see upside in a case of expedited nuclear retirements, as natural gas-fired power plants could also help offset generation lost from nuclear retirements. The continued development of new storage technologies would offset some of that upside for gas, but likely a mix of renewables and gas would be needed to meet an expedited loss in nuclear power generation. Though this scenario is far-fetched at the moment, a significant swing in the political climate could fundamentally shift the US generation stack. To follow our view on demand dynamics including power, exports to Mexico, and LNG exports, request a sample of our Henry Hub Outlook.