The Midwest is one of the windiest regions in the US and electric utilities have been putting all that wind to work, generating an increasing amount of energy from wind turbines. With more electricity being generated from wind alongside stagnant electric demand growth in the region, wind energy has been finding a way to elbow into the market, at the expense of natural gas and coal.

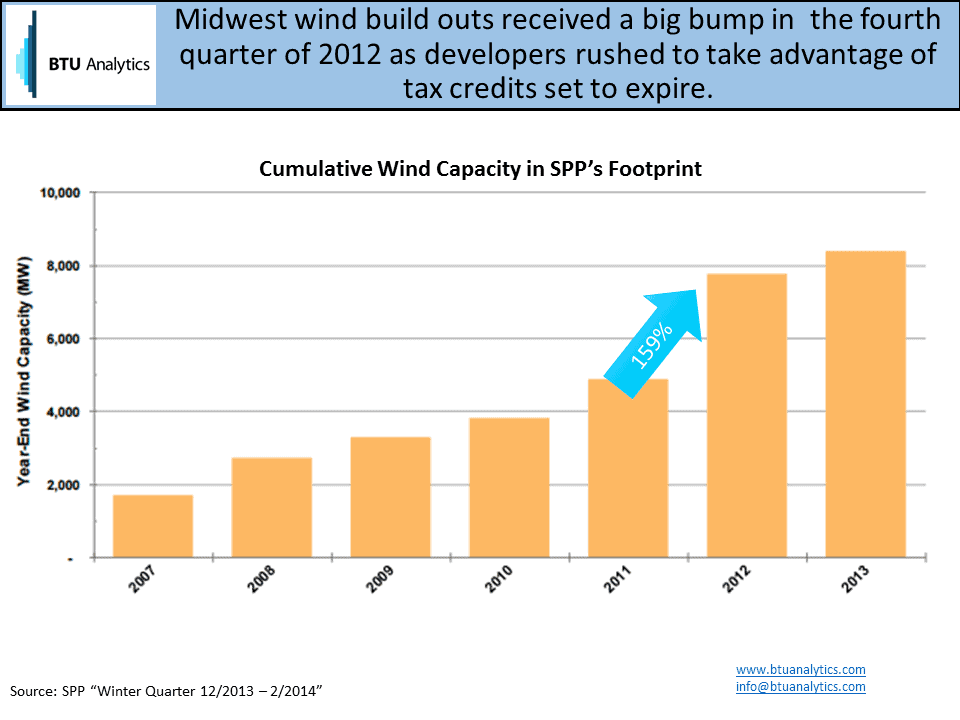

In 2012, much as in the rest of the country, Midwest developers raced to take advantage of tax credits that were set to expire. The Southwest Power Pool (SPP), a regional transmission organization serving mainly Oklahoma, Nebraska, and Kansas, reported a 60% increase in wind capacity between 2011 and 2012. Nationwide, a similar push happened in the fourth quarter of 2012, as EIA reported that of the 13 GW of new capacity in 2012 more than 7 GW of that came in the fourth quarter.

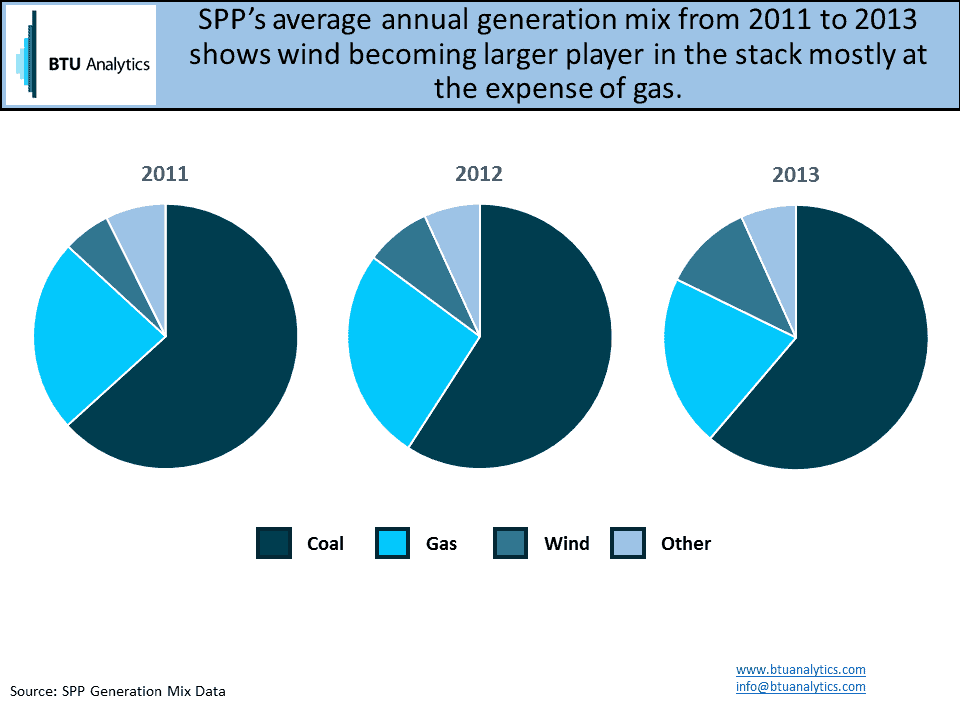

With this much wind coming online, it needs to find a place to go. Granted, since wind is an intermittent resource, not all of that capacity is being utilized due to seasonal variations. Since wind power must be dispatched into the generation stack, other fuels will be pushed out of the stack. In the case of SPP, wind’s growth comes (mostly) at the expense of gas with wind’s share of energy production increasing from 6% to 11% from 2011 to 2013 and natural gas power burn decreasing from 24% to 21% over the same time period.

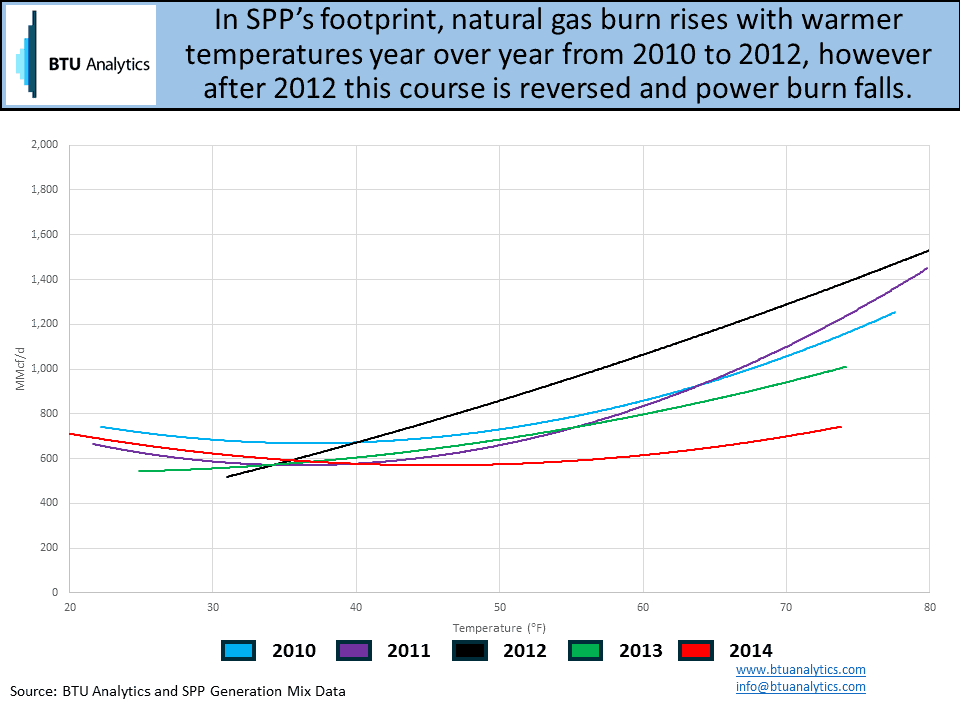

This reverses a previous trend of natural gas taking on a larger and larger role in the generation stack. Looking at power burn normalized for population weighted temperatures, we can see from 2010 to 2012 we had increases in natural gas power burn during the summer, helped specifically by especially weak natural gas prices and record coal to gas switching in 2012, reaching summer records of 27 Bcf/d nationwide and 1.1 Bcf/d in the region. After the implementation of the increased wind capacity, we can see that natural gas power burn has been falling, especially at higher temperatures, pushing back at the region’s ability to reach 2012 levels.

This poses a problem for the gas market. BTU Analytics expects storage based on normal weather to match 2012 record levels by the end of the 2015 injection season at 3.9 Tcf. For that to happen, the market will need to balance record high natural gas production levels against demand from power burn and storage. This sets the stage for natural gas prices needing to dip low enough to incent coal to gas switching at levels that offset the loss of market share to wind. BTU Analytics expects the US gas market will need an incremental 3.3 Bcf/d of natural gas demand over 2014 from coal to gas switching. As renewables continue to fill more of the generation stack, gas prices will have to weaken even further than they would in the past to keep the market balanced. For further analysis on the economics of coal to gas switching, stayed tuned to our Energy Market Commentary.