Over the last several months, the market has been increasingly focused on instilling capital discipline to publicly traded natural gas and oil producers. A group known for outspending cash flow in the pursuit of growth. Private producers are generally thought of as the more capital disciplined investors in the E&P space. Private producers tend to be quicker to react to falling prices and slower to engage new projects as prices begin to rise. Additionally, private producers are not beholden to quarterly earnings statements and thus should be focused on maximizing returns on capital invested rather than short-term stock market sentiment. But does that hold true, do private producers employ capital that much differently than their public counterparts?

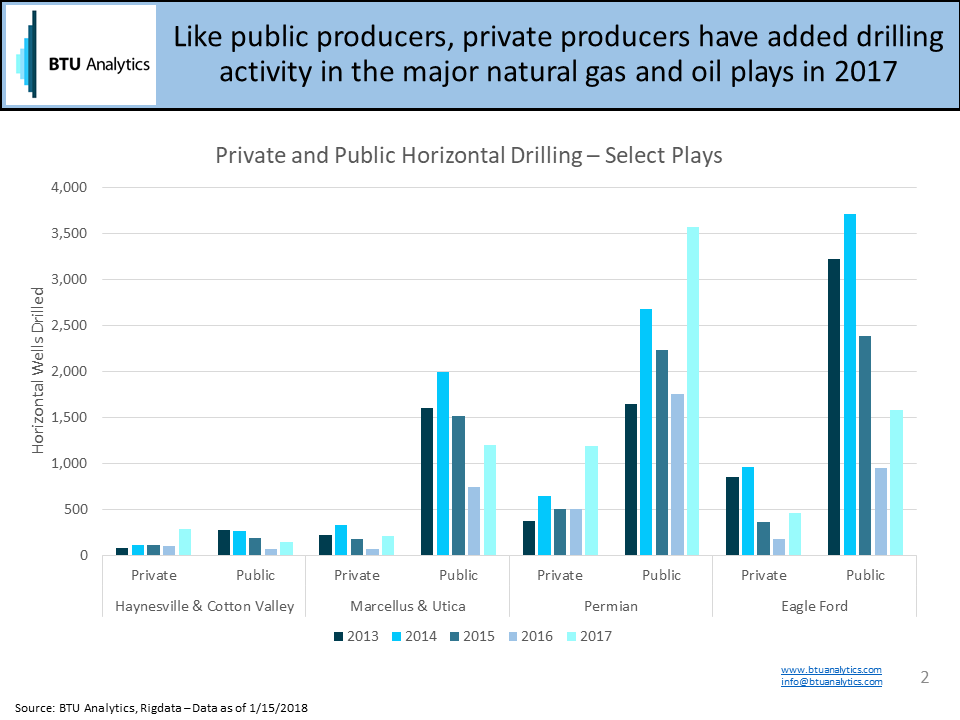

The chart below highlights the total number of wells drilled by year for both public and private producers in the Haynesville & Cotton Valley, Marcellus & Utica, Permian, and Eagle Ford since 2013.

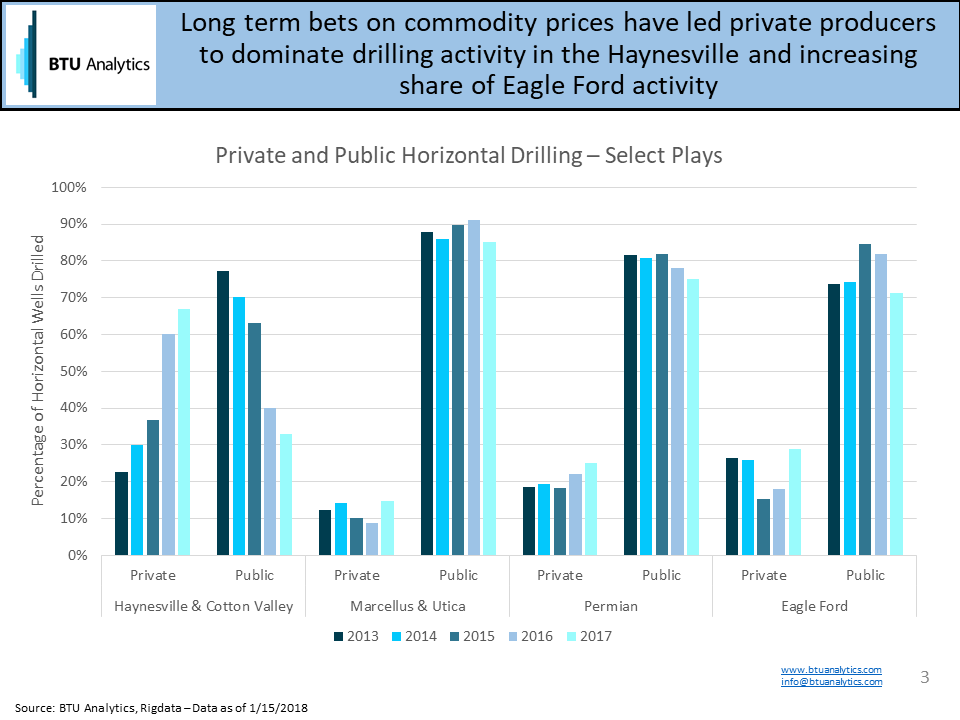

Private producers have followed crude prices higher and have been deploying capital in the Permian and Eagle Ford, but similarly private investment has grown in the Haynesville & Cotton Valley of East Texas and Northern Louisiana. As a share of total drilling, private producers now account for nearly 70% of all the activity in the region (See chart below) compared to just 15% in the Marcellus and Utica.

The Haynesville fell out of favor for public equity investors in 2012. The play suffered as natural gas prices plummeted and crude prices rocketed. The decline in public producer activity led the major E&Ps in the region like Encana, QEP, EP Energy, Chesapeake, Shell, and others to sell assets to fund drilling programs in other basins. Private producers now hold these assets. Drilling surged in 2017 led by Indigo Minerals, GEP Haynesville, Vine Oil & Gas and Covey Park. These 4 private producers accounted for nearly 55% of the drilling activity in the Haynesville & Cotton Valley during 2017 and they drilled 2.5X more wells in 2017 compared to 2016, while natural gas prices rose just 19% in 2017 over 2016.

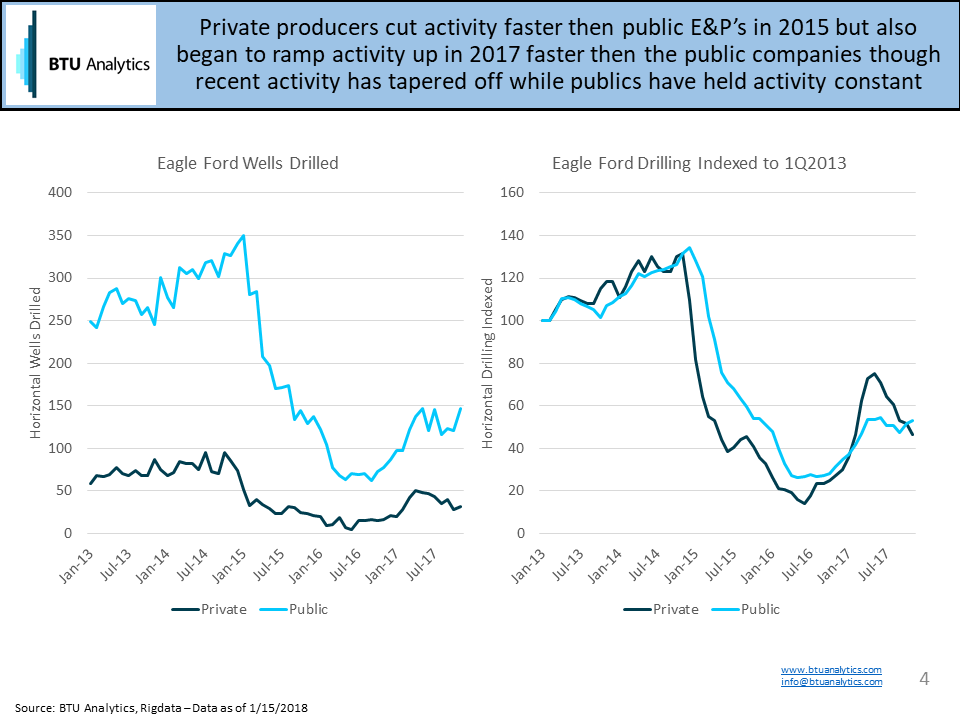

Like the Haynesville, the Eagle Ford fell out of favor in 2015 to the Permian as oil price plummeted. Public producers with acreage in both plays starved their Eagle Ford drilling programs of capital to fund new developments and acreage acquisitions in the Permian. The result was drilling plummeted despite play economics remaining competitive for many operators. The chart below and on the left shows the number of horizontal wells drilled in the Eagle Ford by public and private operators and the chart on the right shows drilling indexed to the 1Q2013.

Public producers dominated activity in the Eagle Ford when prices crashed in 2014 accounting for over 70% of activity and in 2015 their share of activity increased to over 85% as private E&Ps rapidly cut activity in response to prices. Over the last several years, public regional pure plays have consolidated acreage in the Eagle Ford. Consolidation and rising prices led both public and private producers to add activity back to the Eagle Ford. Again, private producers outpaced their public counterparts. However, recently, private producers have begun to scale back activity to lower levels. The decline could indicate service cost increases are eroding drilling economics or well results are under performing expectations.

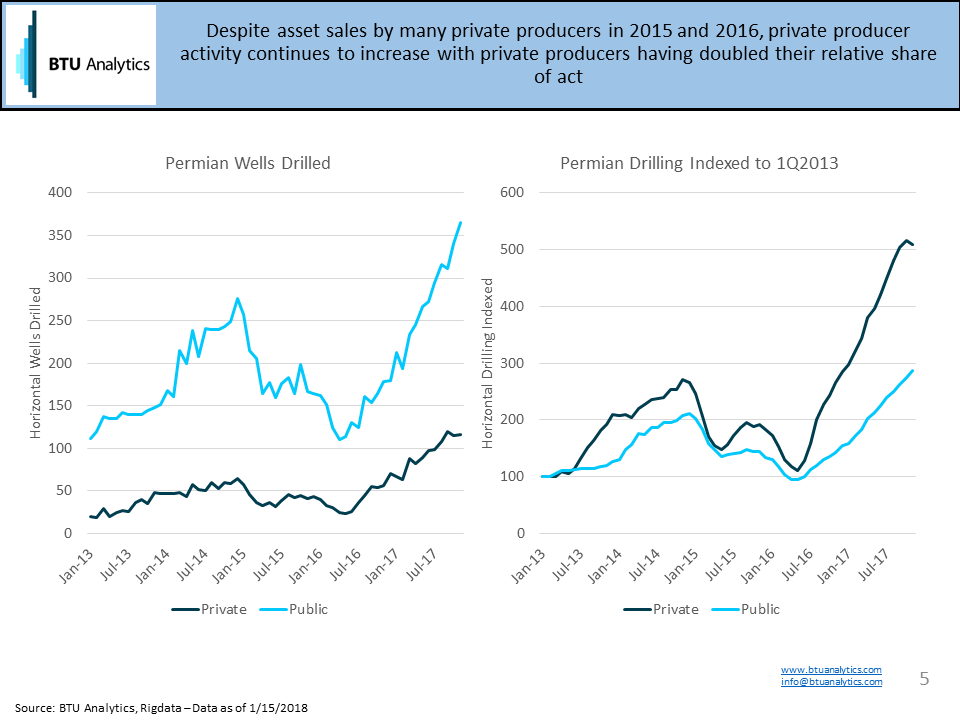

While, the Eagle Ford and Haynesville fell out of favor with public markets, the Permian shines brightly in investor’s eyes. Current drilling activity reflects the play’s economics and long-term potential. In December, operators drilled over 450 horizontal wells. The appetite for acreage by Public producers has prompted many private producers to exit the play over the last 24 months selling positions to Parsley Energy, SM Energy, PDC Energy, Exxon Mobil and others. The remaining private producers continue to drive activity to new highs. Additionally, they have increased their share of total drilling. The gains have occurred despite concerns on commodity prices in 2016, transportation constraints, and availability of service companies.

While public E&Ps are currently under the microscope to increase returns to shareholders, private companies continue to drive forth activity in response to commodity price signals faster than their public counterparts in both a rising and falling price environment. As Brent prices topped $70 this week, expect more E&P capital to flow in, chasing higher prices both from public and private producers.