It has been a long time in coming, but yesterday afternoon FERC issued Energy Transfer’s Rover much needed Notice to Proceed (NTP), which allows Rover to begin clearing trees. With the end of Rover’s tree clearing window looming on March 31, 2017, the question remains: does 45 days provide Rover enough time to clear the project’s nearly 300 miles of new right-of-way? And what other risks persist that can throw a wrench in Energy Transfer’s timeline? Beyond that, what will be the effects of Rover on Appalachian gas production and the wider natural gas market?

This notice comes on the heels of a spate of approvals on February 3, 2017, when Chairman Norman Bay stepped down from FERC’s Commission leaving only two out of five seats filled. With only two Commissioners, FERC lost its requisite three Commission seats needed to approve projects. This means that before another natural gas pipeline project can be approved, President Trump will need to nominate a commissioner, who must then be subsequently approved by the Senate. A sampling of the last ten commissioners shows this is no trivial matter, with average duration from nomination to swearing in lasting in excess of five months.

Keeping the above graphic in mind, it was very fortuitous that Rover would receive their FERC approval on the last day of FERC’s quorum and their NTP in short order after that (having stated they needed the NTP by February 20, 2017, to make its 2017 in-service date). While Energy Transfer was diligent in submitting required follow-up documents following the Certificate decision, doubts still hung over the project regarding the destruction of the 1843 Stoneman House. Even now with its NTP issued, some uncertainty remains around the securing of required easements and the timing surrounding wetland tree clearing.

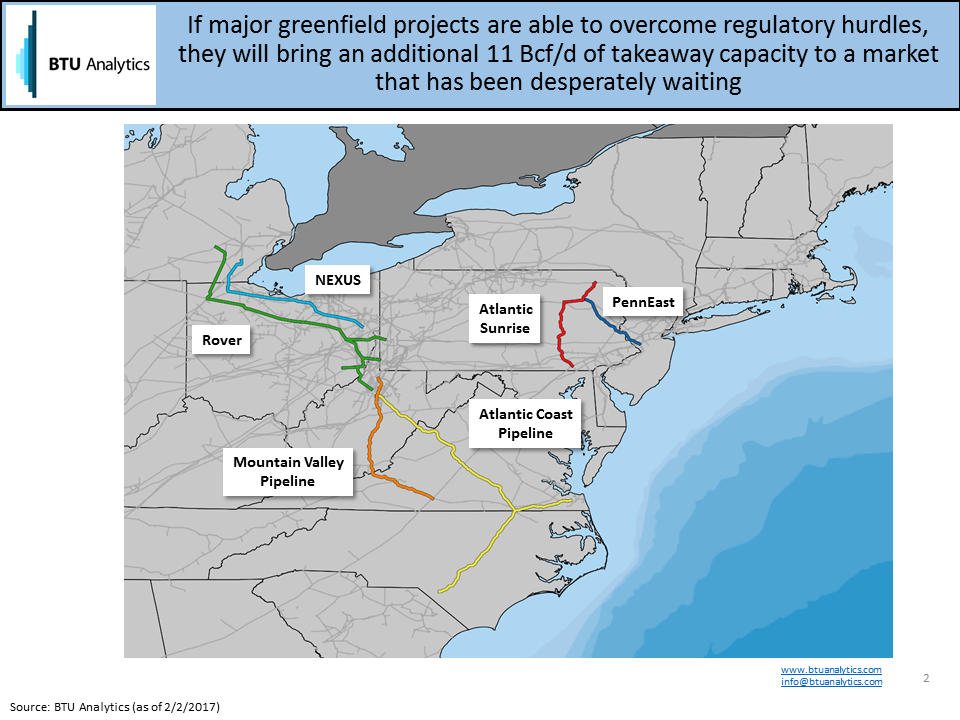

Taking a step back, the map below shows Rover’s path, as well as the other five major greenfield projects coming out of the Northeast.

Of the six, Rover will bring the most volume out of the Northeast, with a capacity of 3.25 Bcf/d. A portion of this gas will eventually push northward into the Michigan and Canadian markets, while the rest of the gas will push southbound towards the Gulf via Panhandle and Trunkline reversals. While TransCanada’s open season on its Canadian mainline did not end in success, Rover’s northbound gas will be making its way into an increasingly crowded marketplace, where it has the potential to displace midcontinent gas, which has traditionally served the Chicago and Michigan markets. Gas making its way down south will find increasing demand as Mexican and LNG exports have come into their own and should continue to grow in the foreseeable future.

What are the still persisting risks surrounding Rover’s anticipated in-service date? Will shippers on Rover begin to ramp up their drilling activity to meet their impending commitments? And most importantly what will happen to Appalachian natural gas production growth if Rover comes on in 2018 versus 2017? For answers to these questions and more, see our upcoming spotlight report on Energy Transfer’s Rover project in our Northeast Gas Outlook this month.