On January 14, 2019, Pacific Gas & Electric (PG&E) announced it would file for Chapter 11 bankruptcy protection. California’s largest utility faces nearly $30 billion in potential liabilities stemming from wildfires in 2017 and 2018. As the company prepares to restructure, some 16 million California customers are preparing to deal with the fallout. However, they’re not the only ones as Kinder Morgan (NYSE: KM) and Pembina’s (TSX: PPL) Ruby Pipeline serves as a major supply route to the west coast, and PG&E is the largest capacity holder on Ruby Pipeline. The pending bankruptcy combined with delays in west coast LNG exports could leave Ruby Pipeline facing a shortage of potential shippers as existing contracts expire.

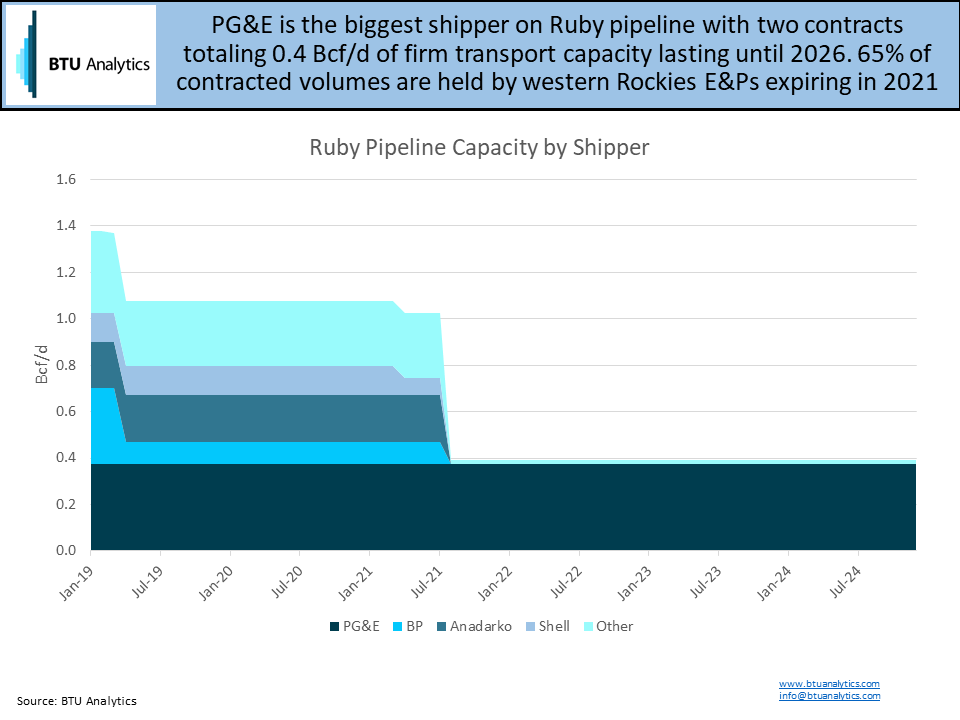

The Ruby Pipeline stretches 680 miles across Wyoming, Nevada, and Oregon. Additionally, the Ruby Pipeline provides 1.5 Bcf/d of capacity out of the Rockies to meet demand on the West Coast. The pipe terminates in Malin, OR, where it connects with PG&E’s California Gas Transmission line to serve demand in Northern California. It comes as no surprise, then, that PG&E is the largest shipper on Ruby pipeline with one contract serving its electric generation load and one for its gas distribution arm. In total, PG&E has about 0.4 Bcf/d of take-or-pay arrangements that expire in 2026. This represents approximately 35% of Ruby’s currently contracted volumes, and 25% of total capacity as illustrated in the chart below. The remaining 65% is predominantly held by western Rockies E&P companies with most commitments expiring in 2021.

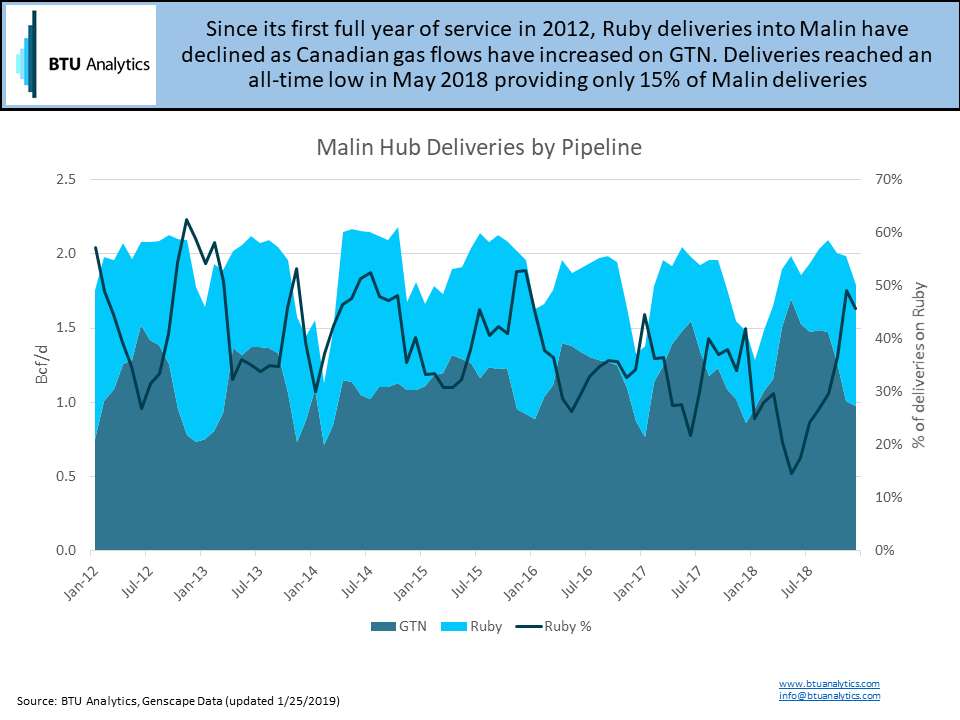

The uncertainty surrounding the outcome of PG&E’s impending bankruptcy isn’t the only concern for Ruby Pipeline. Despite filing for Chapter 11, PG&E’s natural gas load will still need to be served and PG&E could honor its gas pipeline commitments. Since its first full year of service in 2012, the percentage of Ruby deliveries into Malin Hub has steadily decreased. Competition with cheap Canadian gas on GTN pipeline has replaced declining Rockies natural gas production. For 2018, AECO (Canada) traded at an average of $1.20 while Opal (Rockies) traded at $2.76 outright. As a result , Ruby deliveries hit a low of just 15% of all deliveries into Malin Hub in 2018. The chart below highlights Ruby and GTN deliveries to Malin.

However, Ruby Pipeline volumes jumped higher in late 2018 following the rupture of the Enbridge Westcoast pipeline. The outage on Westcoast pipeline resulted in a decrease of 1.3 Bcf/d in Canadian-US cross-border capacity. The explosion has provided a boost to flows in the short-term. However, it is unlikely Ruby Pipeline will be able to depend on Canadian supply outages going forward and Canadian production shows no signs of declining. Additionally, TransCanada is preparing to expand the West Path of the Nova pipeline by 0.6 Bcf/d by 2020. The expansion would increase deliverability to GTN pipeline. Resulting in a boost to Canadian export capacity into the Pacific Northwest. The increase of supply from Canada will result in Rockies’ natural gas facing stiff price competition for west coast markets until new demand arrives.

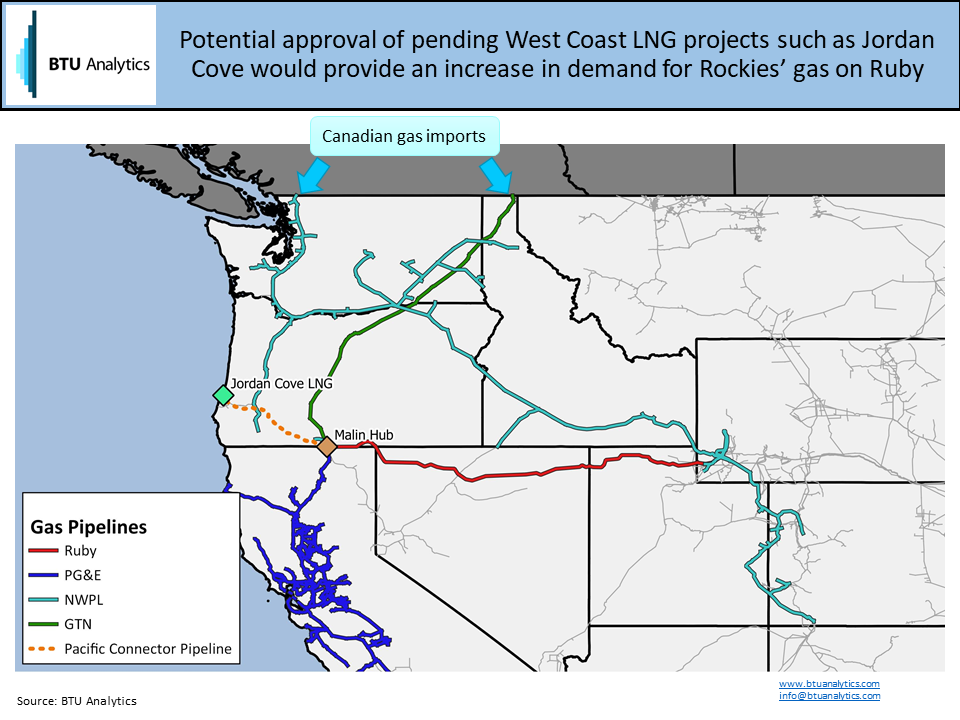

The Jordan Cove LNG export facility in Coos Bay, OR represents the largest single source of new potential demand in the Western US. The proposed 1.08 Bcf/d LNG facility would source supply from the proposed Pacific Connector Pipeline. The Pacific Connector pipeline joins the proposed terminal in Coos Bay to the Malin Hub served by Ruby and GTN pipelines. However, the Pacific Connector Pipeline still faces significant hurdles from local opposition. In a recent court ruling, existing county land use permits for the line were revoked.

In August of 2018, the DOE approved a request to push back the export permit start date for Jordan Cove to 2024 from the original date of 2021. However, most of the Ruby Pipeline capacity commitments are set to expire in 2021, resulting a potential capacity gap for Ruby Pipeline as shippers await new demand sources. The progress made on the Jordan Cove project will be key in the decision to renew capacity commitments on Ruby Pipeline and the rates shippers will be willing to bear.

PG&E’s impending bankruptcy, combined with the upside of future LNG projects, ensures Ruby Pipeline will be a focus of gas dynamics in the West. Find out what BTU Analytics believe will drive the natural gas market by signing up for our free webinar and request a sample of our new Gas Basis Outlook.