Shale has become a four letter word. Perhaps not literally, but investor sentiment towards shale seems to move lower by the day as everyone tries to figure out if shale producers have a sustainable business. In the past we’ve discussed equity valuations and the tumble prices have taken as the industry adjusts to a new phase in its life cycle. Today we focus on the other big piece of the capital structure, debt. Historically, shale producers in North America have used debt capital as a tool to ramp production. However, lower prices and slowing growth are exposing industry players who might have flown too close to the sun. Could near-term debt expiration provide the necessary catalyst for weak players with uneconomic assets to stop drilling new wells?

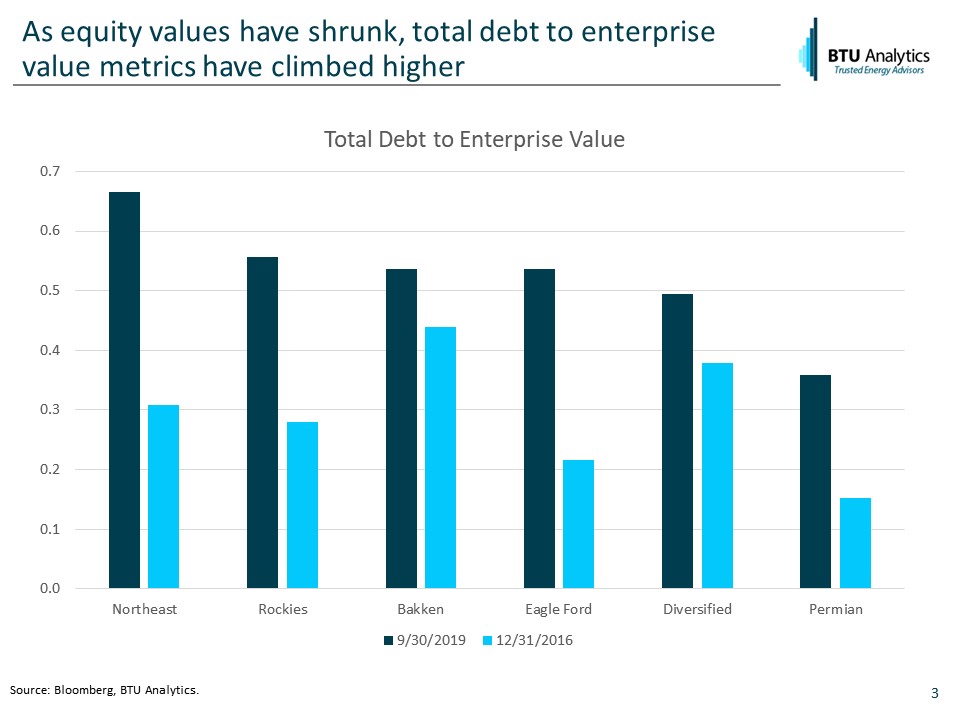

Shrinking equity valuations have made debt a larger component of company enterprise value, particularly over the past year. The chart below compares total debt to enterprise value at the end of the third quarter as well as at the end of 2016 for publicly traded independent shale producers in the major basins. At the end of 2016, most basin categories had a ratio of approximately 0.3x total debt to enterprise value. Today, most basins show an average closer to 0.5x, with the Northeast operators approaching 0.7x on average.

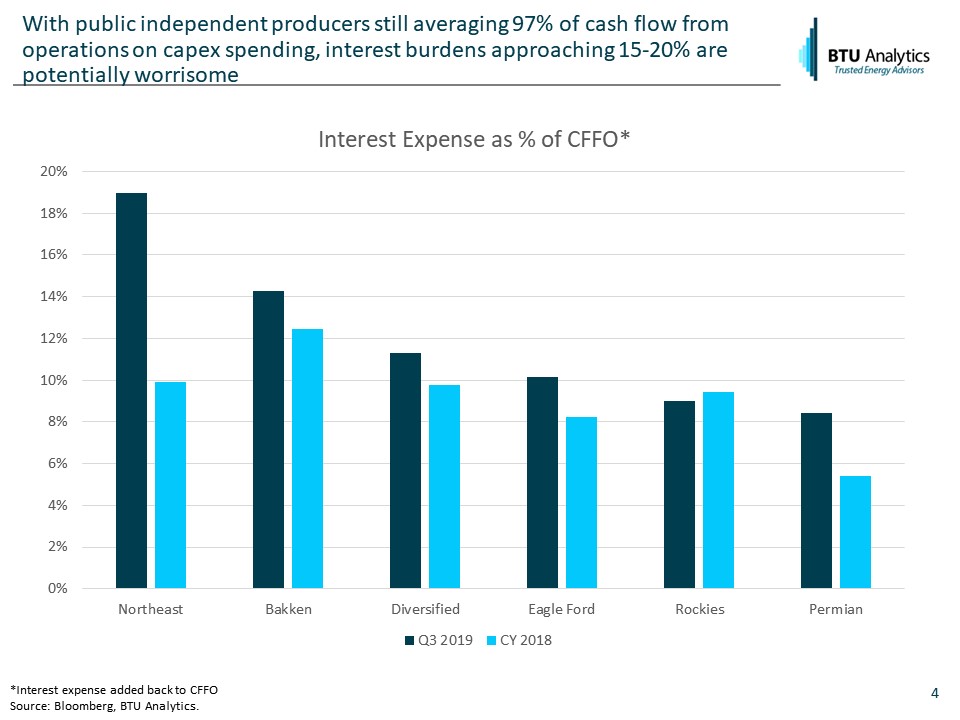

One of the next logical steps to take to understand whether or not these levels are concerning is to look at interest expense relative to cash generated from operations. The chart below shows that the average interest burden as a percent of cash flow from operations grew in most basins in 2019, and is now approaching 15-20% of cash flow from operations in some areas.

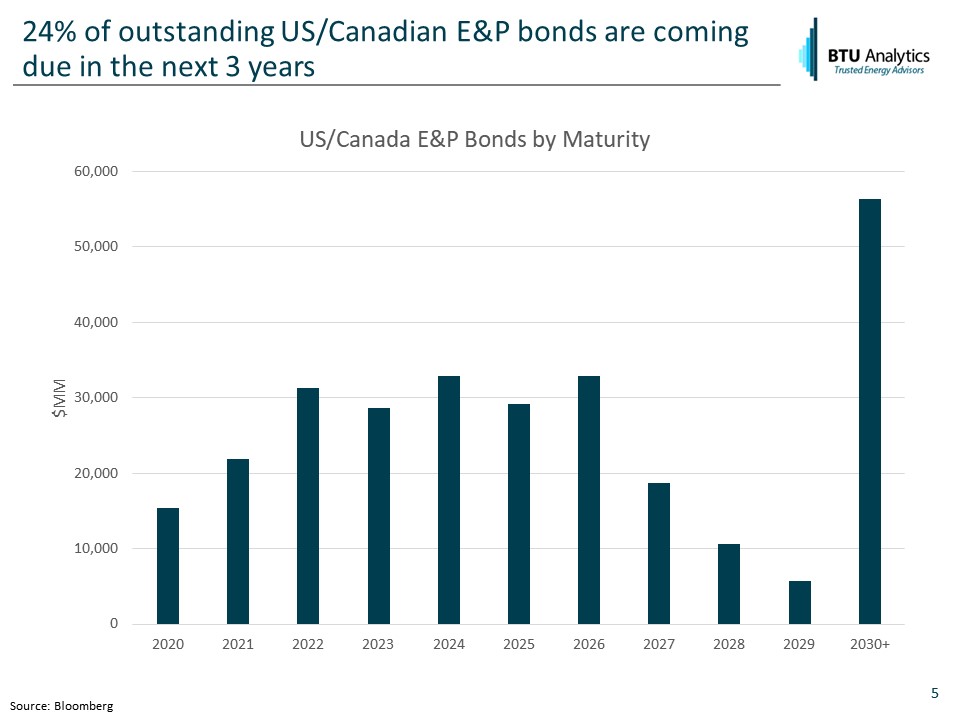

The chart below expands the analysis from public producers to all outstanding bonds for US and Canadian E&P companies.

Approximately 24% or $70Bn of the industry debt shown above is maturing in the next three years. Over the past ten years, shale companies have generally been able to refinance maturing bonds without making headlines. However, producers are now under the microscope as the industry comes to grips with low prices squeezing margins and production outlooks with much lower growth rates than in past years.

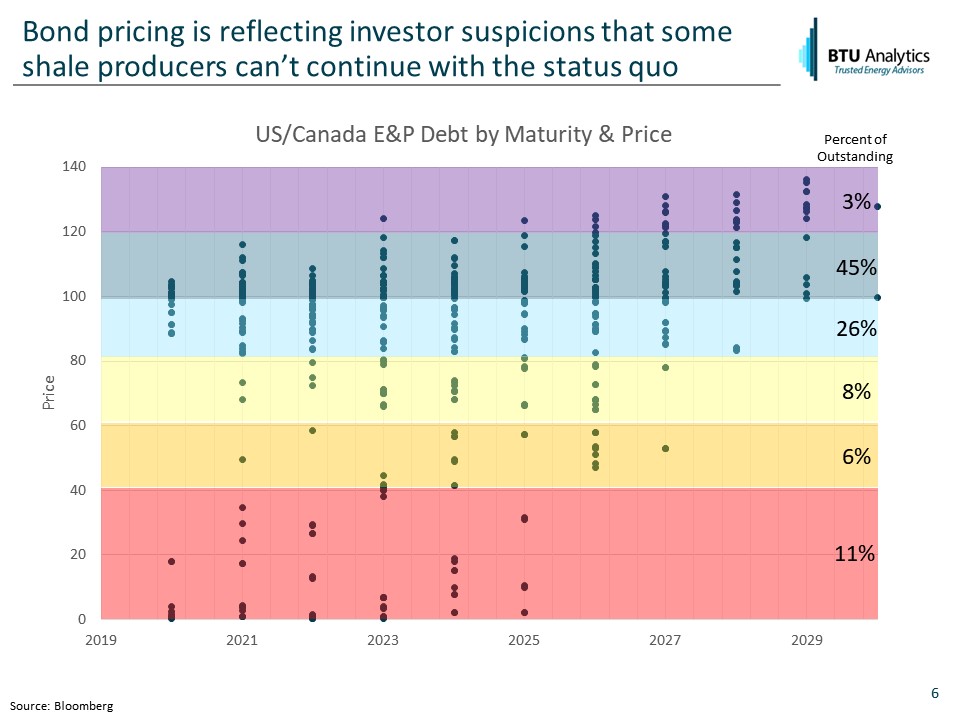

Moving a level deeper and looking at bond pricing shows that debt investors are calling into question their ability to collect future interest payments. Note that bond pricing doesn’t necessarily reflect distress (for example, zero coupon bonds) but in this sector, bond pricing generally reflects the risks highlighted in the prior slides.

About 11% of outstanding debt is priced below 40. Many producers who have declared chapter 11 have their bonds in this category including Sanchez Energy, Ultra Resources and Approach Resources. Another 6% of outstanding debt is priced below 60, including bonds from Chesapeake, Extraction Oil & Gas and Whiting. The 60-80 price bucket includes bonds from Gulfport and Antero. 71% of outstanding E&P bonds are trading between prices of 80-120, with the remaining 3% trading above 120.

Can looming debt maturities be a catalyst for change or will debt investors and their incentives delay the actions necessary to build a sustainable business model for shale? Request a sample of BTU Analytics’ Upstream Outlook service to get our latest monthly thoughts on the evolution of shale production.