With earnings season once again upon us, the market is getting greater clarity on 2H’19 activity levels and production. Back in February, we touched on how public company guidance in Appalachia for 2019 compared to our forecasts which called for slowing growth. The reality of first half activity is now known, and our calls on 2019 look to be coming to fruition. With less capital to put into the ground and the Henry Hub strip averaging less than $2.50/MMbtu through 2022, Appalachian operators are slowing down. Today’s analysis will look at how activity in Appalachia has fared to date in 2019 and what capital remains to be spent.

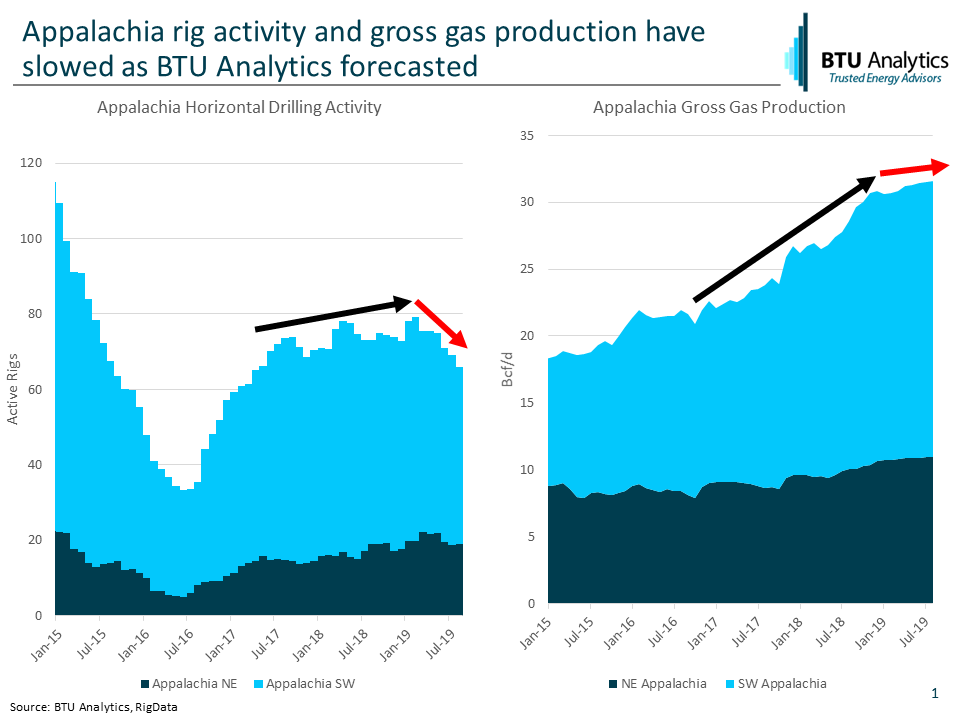

The charts below show rig activity (left) and gross gas production (right) for Northeast Appalachia and Southwest Appalachia. The rig count has fallen considerably throughout 2019. SW Appalachia, which has driven the majority of the rig slowdown, has battled historically low NGL pricing as well as investor pressure on public companies to return more cash to shareholders and be disciplined with capital spending. The number of wells drilled in Appalachia has shown more moderated declines in the first half of 2019, showing that operators are drilling more efficiently.

Beyond the rig count, gross gas production growth is slowing in Appalachia as well. After growing by more than 21% between December 2017 and December 2018, dry gas flows in Appalachia have grown by just 2.5% from December 2018 to July 2019. This is again driven primarily by SW Appalachia, which grew by nearly 23% from exit-2017 to exit-2018, and just 2.4% so far this year. Production growth in NE Appalachia has also slowed, though not at as staggering of a pace as its SW Appalachia sibling.

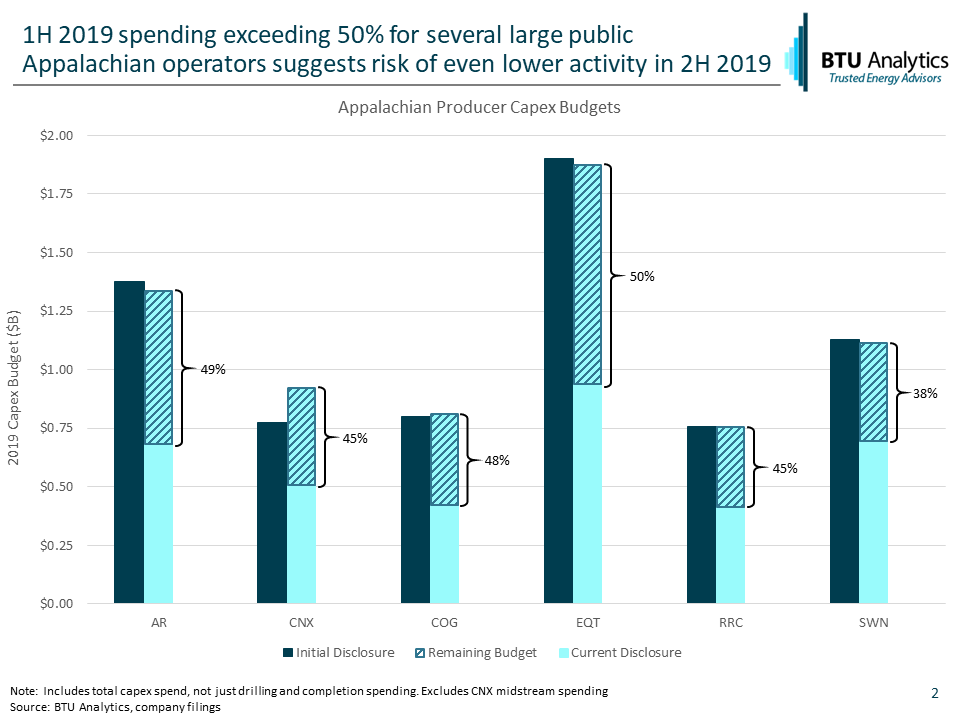

With more than two-thirds of 2019 drilling activity driven by publicly traded companies, it’s no surprise that the decrease in capex spending that we talked about in March has slowed growth in the region as a whole. Now that most of these companies have reported 2Q’19 earnings, how much is left in the tank?

The chart below shows the initial capex budgets released by six of the largest independent public operators in Appalachia. In 2Q’19 earnings releases, Appalachian operators have either maintained or moderately lowered their capex budgets. On top of that, most operators have utilized more than half of their announced capex budgets in the first half of the year. This leaves even less capital for second half development. It’s important to note that initial 2019 capex budgets in the Appalachia were roughly 20% lower than 2018 levels.

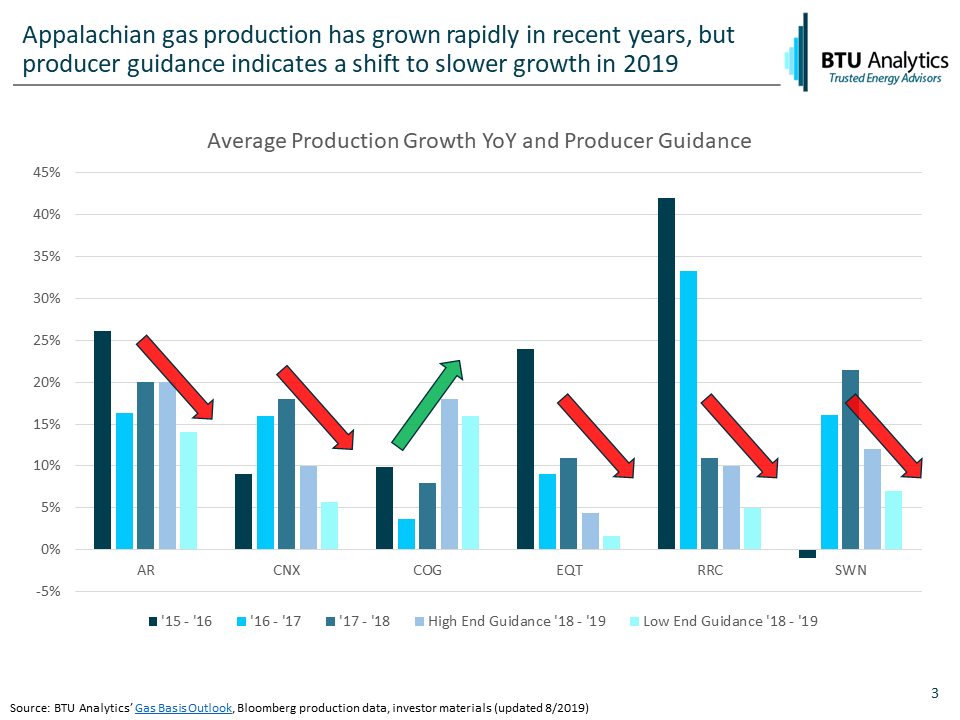

With fewer capex dollars to spend in the second half of 2019, and first half activity already lower than 2018, it’s reasonable to think that Appalachian activity will fall even further. The chart below highlights recent production growth and 2019 guidance for key Appalachian operators. For each operator outside of Cabot, these Appalachian E&Ps are forecasting growth below what they have achieved in recent years. However, less capital won’t only translate to slower production growth in 2019. The relationship between capital spending and production depends on the ratio of capital spent on drilling versus completions as well as the timing of spud to sales. A slowdown in 2019 drilling could be felt more acutely in 2020 production.

BTU Analytics currently forecasts completion activity to decrease in 2H’19 from 1H’19 levels and fall even further in 2020. With fewer completions, overall production growth is also expected to slow. What does the future hold for Appalachia? Will LNG bring back double digit growth? Request a sample of BTU Analytics’ Upstream Outlook to follow these trends.