Earnings season is just around the corner, which will likely include an update on company outlooks for service costs and a read through to industry profitability. In today’s Energy Market Insight, BTU Analytics will review recent service company operating margins in anticipation of new data points and read between the lines on what recent data and commentary might indicate about the longevity of cost improvements achieved over the last few years.

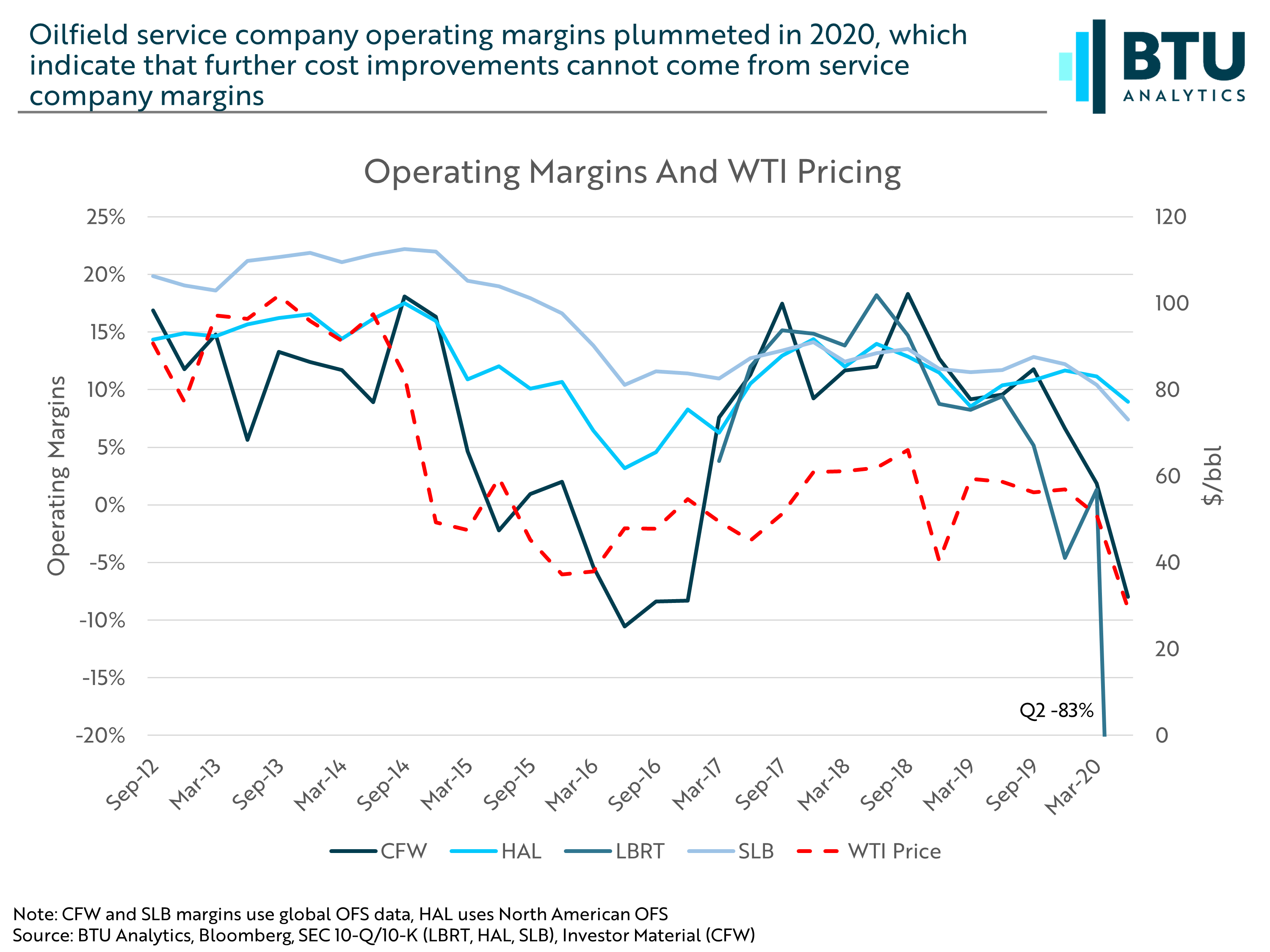

In some ways, the cycle of feasts and famines is a familiar undertaking for the oilfield service sector. When commodity prices warranted drilling and completion activity at a breakneck pace, service companies charged premium rates to deliver the requested resources, which inflated their operating margins at the expense of E&P companies. When commodity prices soured, third-party vendors were often the first targets of E&P company cost-cutting initiatives. While the early innings of the shale revolution were characterized by higher operating margins for companies like Schlumberger and Halliburton, activity in recent years failed to generate quarterly operating margins in excess of 15%, as shown in the chart below.

Note that the geography and services included in each margin vary by company. Halliburton’s North American oilfield service operating margin traditionally lagged Schlumberger’s analogous global metric, but the first half of 2020 proved to be a reversal of this relationship. As drilling and completion activity came to a screeching halt in 2Q 2020, Schlumberger’s operating margin fell to just 7.4%, which lagged Halliburton’s 9.0% over the same quarter. Following 2Q 2020 earnings announcements, Schlumberger announced the sale of its onshore hydraulic fracturing business in the United States and Canada to Liberty Oilfield Services (NYSE: LBRT). BJ Services and Calfrac Well Services, two notable fracturing competitors, filed for bankruptcy protection in July. Declining service costs have provided initial relief to E&P companies’ capital budgets, but the resulting famine service pricing can only sustain service companies’ bottom lines for so long, even following bankruptcies and consolidation in the service sector.

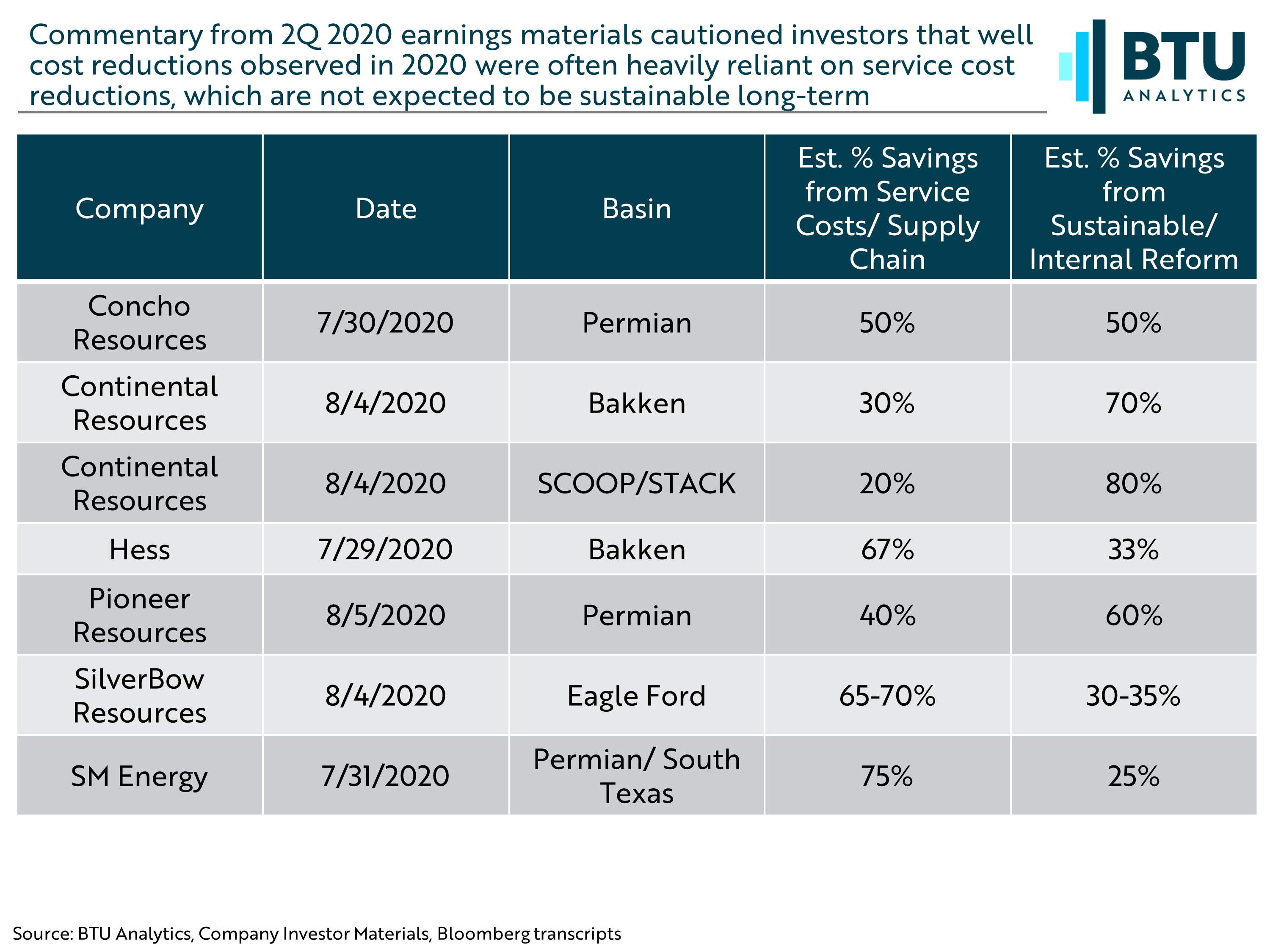

Producers’ 2Q 2020 earnings commentary contained multiple mentions of well cost reductions compared to prior guidance for the activity planned for 2020. However, well cost reductions from several operators were caveated with detail about how costs were reduced. Heavy reliance on service cost reduction would achieve rapid drilling and completion cost improvement, but like commodity prices, service cost levels are subject to market conditions. Continental Resources and Pioneer Resources expect that over 50% of their well cost savings are structural or sustainable, which would dampen the impact to well costs when service cost inflation rebounds. Companies whose recent well cost improvements are predominantly driven by service cost reductions will likely give those gains back when recovery occurs, and recovery will need to occur for service companies to remain viable long-term.

Commodity price strength shapes the trajectory of overall drilling and completion activity, but not all operators’ boats are expected to rise with the tide equally as crude pricing improves and service costs eventually recover over the next several quarters. How will changing well costs and leading-edge economic indicators impact breakevens? Which E&P companies maintain operational competitive advantages to weather the storm created by COVID-19’s disruptive forces? What does a slower pace of drilling mean for long-term shale inventory? The answers to these questions and more can be found in BTU Analytics’ Economics View. Request a trial today by emailing info@btuanalytics.com.