Earnings season is officially underway, and this quarter is of particular importance as E&Ps unveil their 2018 capital budgets and production outlooks. Investors have increasingly pressured companies to focus on capital discipline and shareholder returns, and this quarter’s announcements will shed light on how companies respond and what that means for production growth in coming years.

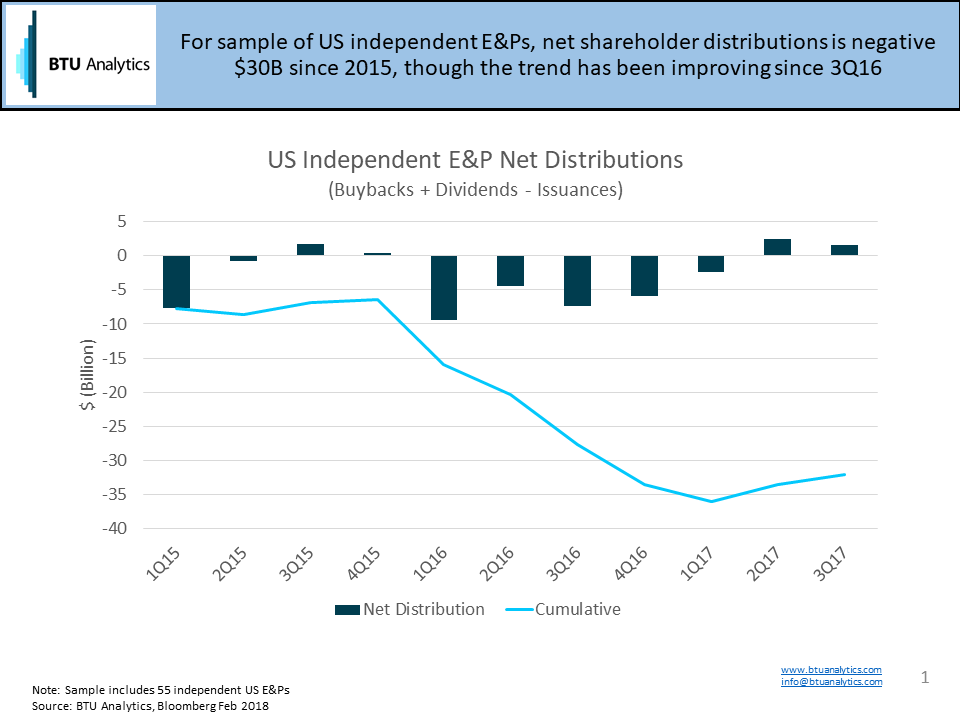

First, let’s begin with a couple of anecdotes. Gulfport (GPOR) announced a $100MM share repurchase program alongside updated production guidance that was about 10% below consensus. Pioneer Natural Resources (PXD) announced a dividend increase and a $100MM share repurchase program. Anadarko (APC) announced an increased repurchase program, 400% dividend increase, and plans to retire $1B in debt. These announcements exemplify the transitioning tone in the oil patch as more focus is placed on capital discipline and even returning capital to shareholders instead of production growth. The chart below shows how the industry has trended (using a sample of 55 independent E&Ps) since 2015 for net distributions, which is defined as Buybacks + Dividends – Issuances.

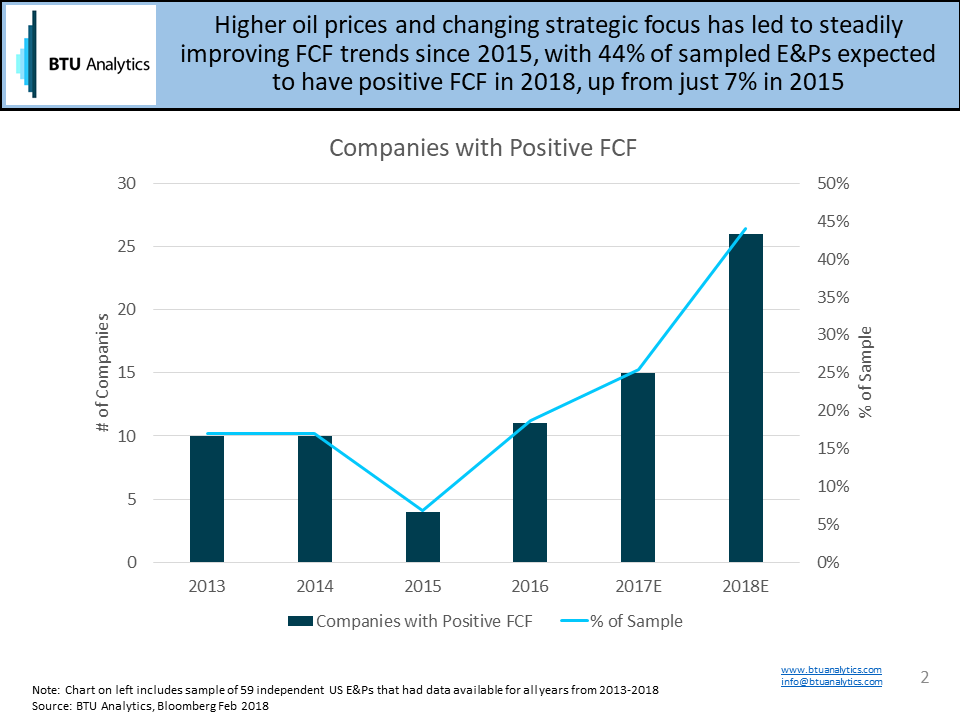

Across the group, net issuances since 1Q15 are $30B in the red; however, the trend has been improving each quarter since 3Q16. Operating within cash flow is a closely related topic that BTU Analytics has analyzed previously, and that trend also appears to be improving. The chart below shows historical results and the latest 2017 and 2018 Bloomberg consensus estimates for free cash flow (FCF).

Based on this data, the capital discipline trend has been steadily improving, with nearly 45% of all sampled E&Ps projected to generate positive FCF this year. While it is difficult to speculate what will happen with excess cash flow, announcements like those from GPOR, APC, and PXD indicate that some companies will discuss the potential to return capital to shareholders. However, particularly for companies with oil exposure, will the temptation to maximize production while oil is above $60 be too great to resist? There is likely no region where the temptation is greater than the Permian.

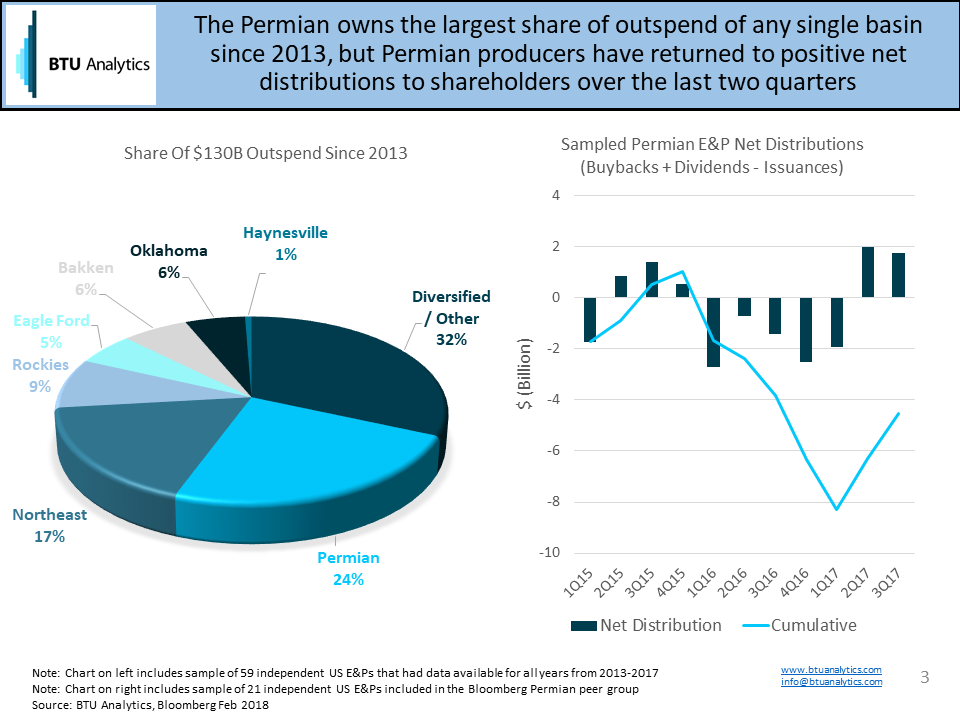

Since 2013, total outspend across our sample of independent E&Ps is nearly $130B, with Permian producers contributing nearly 25% of that. Returning to the concept of net distributions to shareholders, the Permian has shown improvement over the last few quarters, perhaps signaling changing priorities.

BTU Analytics is watching these trends closely because a general strategic shift towards capital discipline would have material impacts on production. In 3Q17, we published a scenario analysis showing that the impact from operating within cash flow could be 10 Bcf/d for gas and 2 MMb/d for oil in the US.

We will be doing a deep-dive into the topic of drilling within cash flow, hedging, and sources of capital at our third annual What Lies Ahead conference in Houston on February 22nd, in addition to other special features including Permian and Oklahoma exuberance, impacts from new pipelines, inventory and economics, and more. If you can’t make it to the conference, request a copy of the Upstream Outlook to see how we see these changing dynamics shaping the market.