With crude prices holding near $40/bbl for the better part of a month and frac spreads returning in some basins, many clients are asking when shale production will return and at what price?

The answer can be both simple and frighteningly complex. Today’s commentary will stick with the most simple framework for understanding that answer, well economics.

The trajectory of US crude oil production is a function that historically considers both the natural declines of production that is already online as well as production from new drilling. An added variable in the current market is production that was curtailed or shut-in as physical constraints cratered pricing, which BTU Analytics estimates to be roughly 1.3 MMb/d in June. Returning shut-in or curtailed production generally requires less capital than drilling new wells. Producers should return that production to the market as crude prices move above the variable cost of production, which includes costs such as gathering fees and water disposal, but producer-specific considerations can also be a factor.

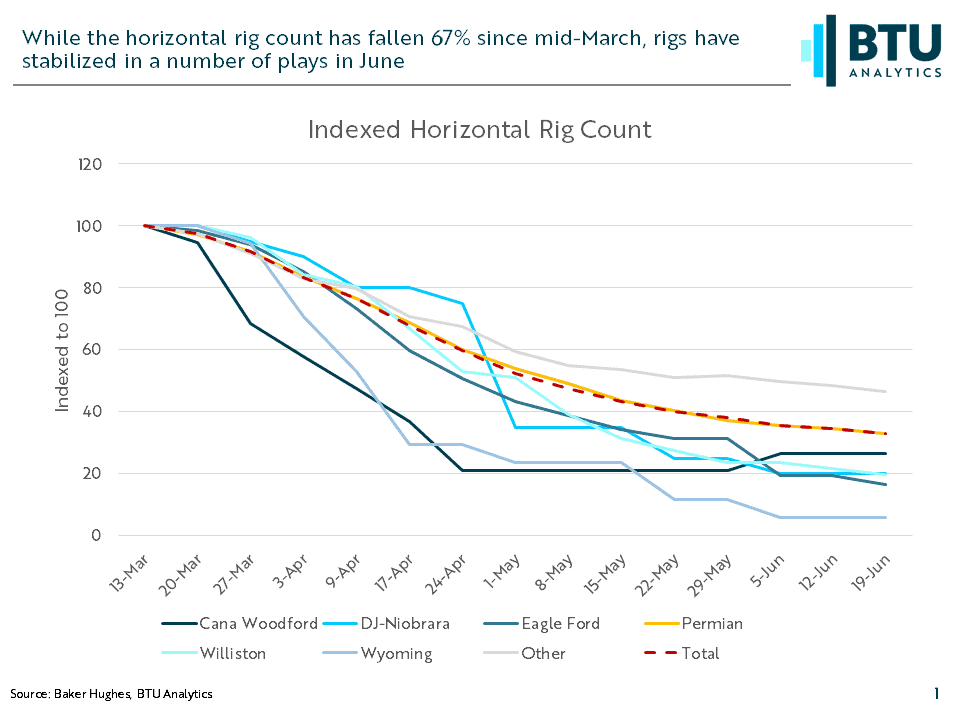

That brings us to new wells. Horizontal rig counts are down 67% overall since mid-March, but specific basins have taken an even bigger hit, with Wyoming rigs down 94% and Eagle Ford rigs down 84%.

Indexing and charting the relative decline in rig counts by basin shows that a number of basins have seemingly arrested their rig declines in June. BTU forecasts that the low in drilling activity will be reached between June and August for oil-focused plays. This overall pace of drilling declines will depend heavily on Permian activity, since that basin represents ~55% of the horizontal rig count.

What will bring the rigs and frac crews back will vary by producer. While management teams will all make different decisions based upon individual company considerations including base declines, proved reserves, leasehold expirations, hedges, contracts and cash flow, the economics of new drilling will be a central focus. Producers in the same play can have starkly different economic results.

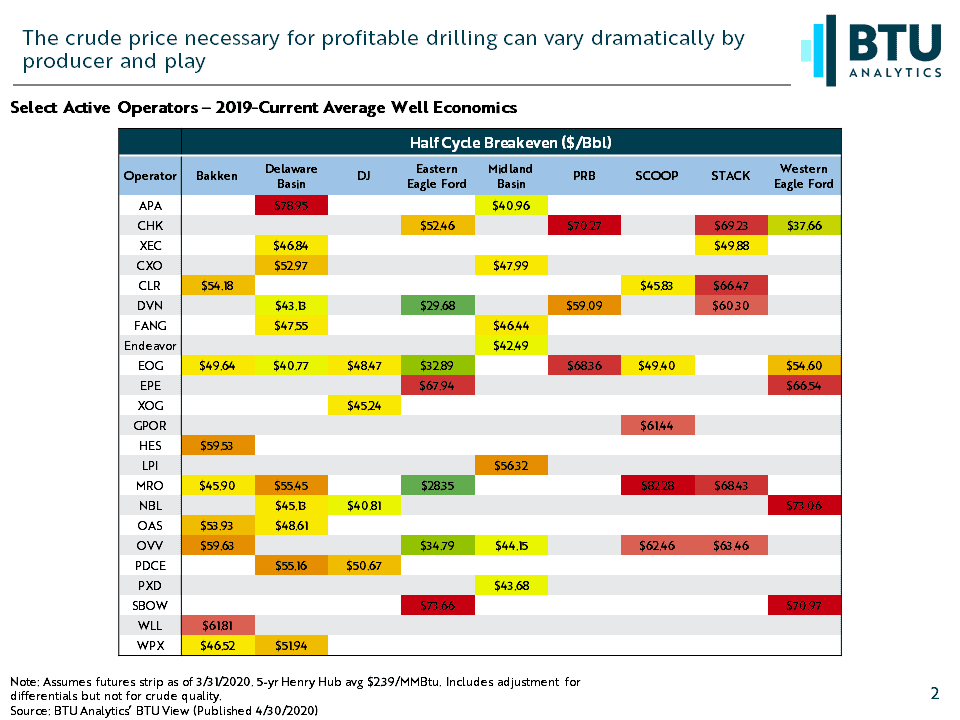

The table below is sourced from data that feeds the BTU View Economics tool and will be a part of the snapshot summary of quarterly changes in the tool sent to tool subscribers. It shows average well-level economics for each operator based on wells that were turned to sales since the beginning of 2019.

At the low end of the spectrum, some producers have average Eagle Ford breakeven prices under $40/bbl based on wells that have come online since 2019. Average producer breakeven pricing in the Midland is in a tight band of $40-$45/bbl for most operators. Most of the Delaware producers listed have half cycle averages in the $45-$55/bbl range, followed by producer results above $50/bbl for most operators listed in the Bakken, PRB, SCOOP and STACK. Notably, these breakeven estimates do not consider the corporate costs associated with running an oil and gas business, which can add up to an additional $5 – $10/bbl.

Breaking and maintaining a crude price above $40/bbl will bring back significant activity off historic lows, but activity alone shouldn’t be an indication that all is well in US shale companies.

Want access to more leading edge economic data or granular and thoughtful written analysis of the complexities that impact producer cash flow, profits and performance? Request trial access to our BTU View Economics package.