The DJ Basin continues to face both regulatory and midstream challenges. In November, Colorado voters rejected a ballot initiative to increase well setbacks. Now, a lawsuit arguing Colorado’s forced pooling statute is unconstitutional further mires the outlook for development in the basin. Not only do producers deal with an increasingly challenging regulatory framework, but lack of midstream in the basin has impacted drilling decisions. Over the last two years, DJ basin natural gas processing capacity bottlenecked gas output. As a result, operators shifted completion activity away from gassier areas of the basin. In late 2018, natural gas processing capacity bottlenecks eased. However, the shift in drilling decisions will have a lasting impact on operators’ future drilling plans.

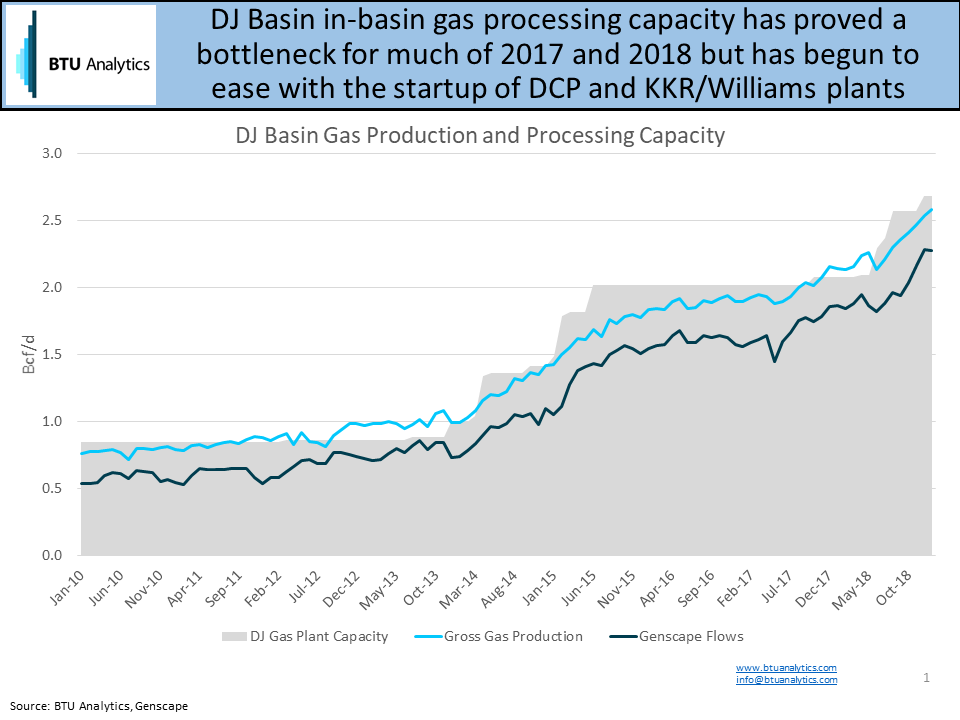

The chart below shows gross gas production and DJ basin natural gas processing capacity. For nearly all of the last 3 years, utilization of in-basin processing capacity exceeded 90%. In the 2H2018, new facilities from DCP Midstream and Rocky Mountain Midstream opened the door for increased production out of the DJ basin. Debottlenecking will continue throughout 2019. New natural gas processing plants from Western Gas, Rimrock, and DCP are expected to enter service and provide additional relief.

There are multiple levers that operators lacking access to gas processing can pull to manage bottlenecks in capacity. One strategy would be to reduce completion activity in the basin. However, in 2017 and 2018, crude prices were rising. Additionally, Niobrara and Codell formations are two of the most economic plays in the US. A second strategy then is to focus operations on areas producing less gas or unconstrained areas. Many producers favored the second approach. Initial production (IP) rates for natural gas in the DJ decreased by an average 16% between 2017 and 2018. However, oil IP rates fell by just 4%, representing a 12% decrease in the gas to oil ratio (GOR) of 2018 wells.

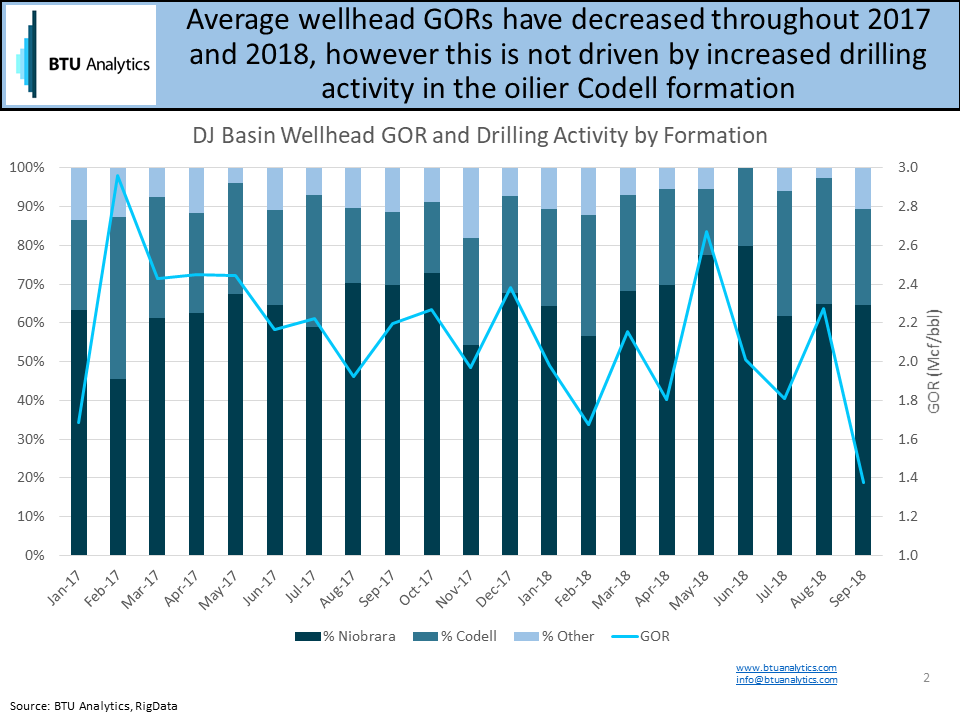

In the DJ Basin, two formations attract consistent drilling activity: the Niobrara and Codell. The Codell is shallower than the Niobrara. In 2017 and 2018, wells targeting the Codell averaged a gas IP rate 12% lower than the Niobrara. Additionally, oil initial production rates remained comparable. However, the Codell typically isn’t targeted heavily in the southwestern core of the DJ Basin and wasn’t targeted any more than usual in 2018. The chart below highlights the distribution of Codell and Niobrara drilling versus average GORs. While GORs decreased over the past two years, the split in formations remained relatively unchanged. 27% of wells targeted the Codell in the first nine months of 2018 compared to 26% for 2017.

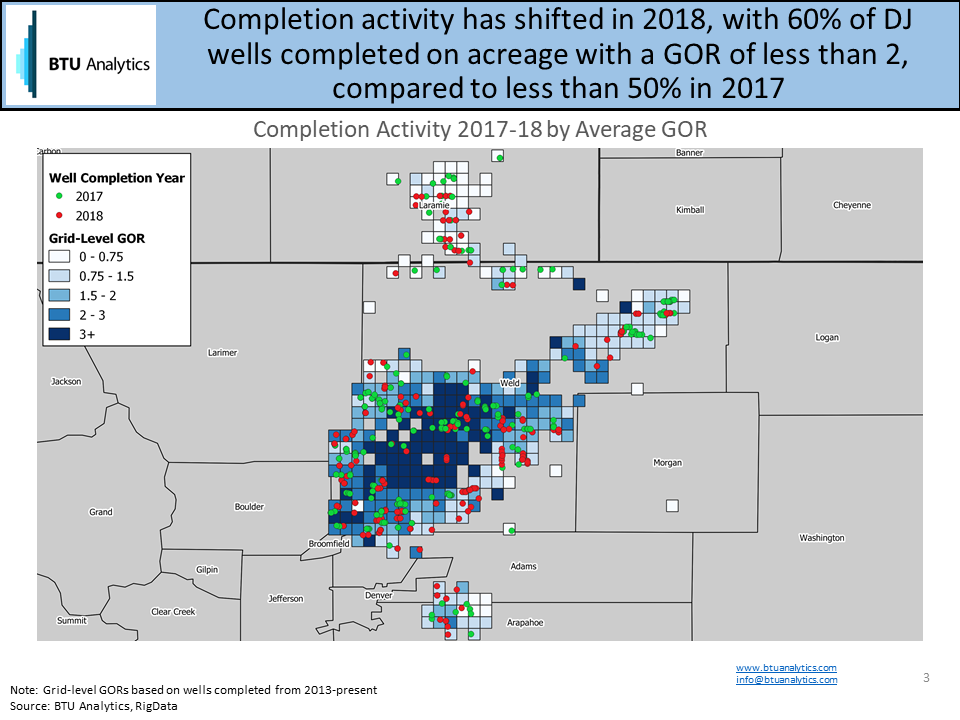

Instead of targeting the oilier Codell, producers tended to drill less gassy acreage on average than the acreage drilled in 2017. The map below shows the wells drilled in 2017 (green dots) and 2018 (red dots) compared to the average GOR seen on that acreage from 2013 to present. In 2018, 60% of the wells were completed with a GOR of 2 or less, while in 2017 less than half the wells completed were drilled on similar acreage.

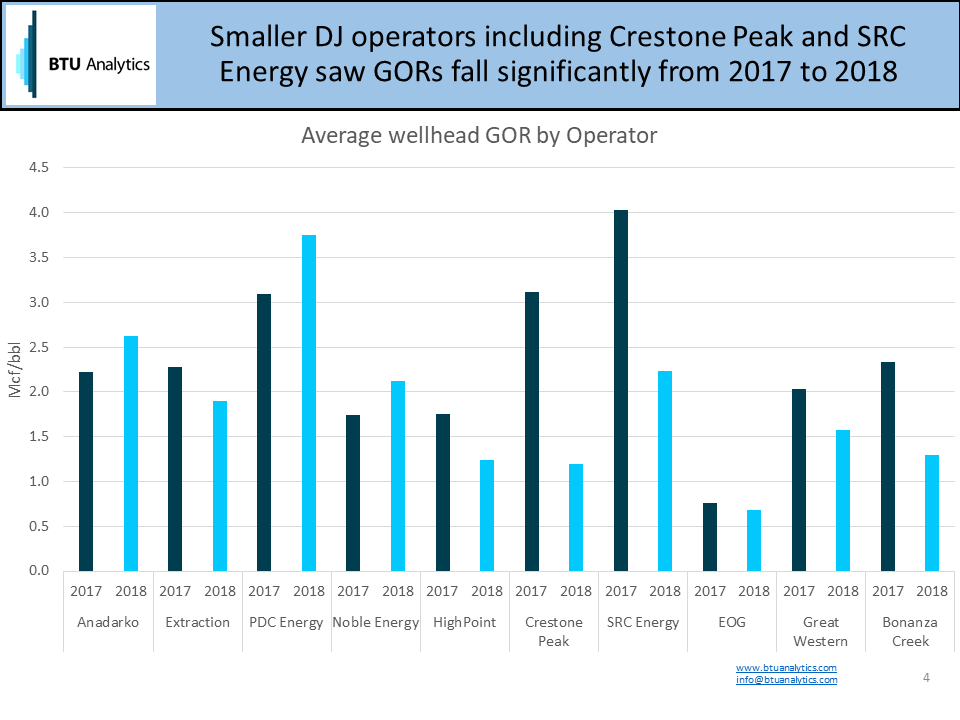

New DJ production in general was oilier in 2018 than compared to 2017. However, not all operators experienced equal changes in GOR. Large DJ operators like Anadarko (NYSE: APC), PDC Energy (NYSE: PDCE), and Noble Energy (NYSE: NBL) likely have greater ability to secure processing capacity compared to smaller operators. Therefore, the large operators have less incentive to target lower GOR acreage. The chart below highlights this trend by showing the average GOR for the top 10 operators in the DJ from largest to smallest operator. Smaller operators like HighPoint Resources (NYSE: HPR), Crestone Peak Resources, SRC Energy (NYSE: SRCI), Great Western, and Bonanza Creek (NYSE: BCEI) all saw their average GOR drop between 23% and 62%.

For smaller companies, it can be more difficult to secure natural gas processing capacity. SRC Energy highlighted yesterday processing bottlenecks posed a significant obstacle throughout 2018. As a result, SRC Energy lowered production guidance in 3Q 2018. Similarly, HighPoint Resources highlighted the impacts of high gathering line pressure on its production in 3Q 18.

For smaller DJ operators, shifting the acreage in which they drill can have lasting impacts on cash flow. New acreage may not be fully delineated or may be less economic altogether. BTU Analytics estimated wellhead breakevens increased in 2018 compared to 2017 for Crestone Peak, HighPoint, and SRC Energy. This is driven by lower oil and natural gas production rates. The drop in productivity signals these companies could have been forced to develop less economic acreage because of the processing constraints.

The DJ Basin natural gas processing constraint is being resolved this year. However, the bottlenecks experienced in 2018 will likely have lasting impacts on some DJ producers. To see more operator-level breakevens, as well as remaining inventory by basin and breakeven, request a copy of our newest E&P Positioning Report released last week. In addition to the gas processing constraints, we track all existing and developing infrastructure constraints in the DJ in our Upstream Outlook Report.