Over the past two years, BTU Analytics has written extensively about DUCs or drilled but uncompleted wells, with our first energy market commentary on the topic posted all the way back in January of 2015. But over the past several months, we’ve been telling our clients that the market impact of DUCs is essentially done, and the correlation between rig activity and production will again improve as that hangover from the shale boom is lifted. DUCs may be done, but is the market being set up for a new hangover? One caused by the collective excitement and potential of the Permian Basin? Make way for PUCs.

The term “DUC” well gained traction in the months following the oil price crash in 2014. Prior to the price collapse, wells were drilled and typically completed within a predictable time frame, generally one to six months, depending on the region and whether pad drilling was being employed. But when oil prices crashed, many producers slowed any activity that they could, hoping to reserve cash and future production until higher prices were on the horizon. Some producers were so bold as to publicly highlight a time frame in which they expected the market to recover, and communicated to the market that they would wait to complete wells until that time.

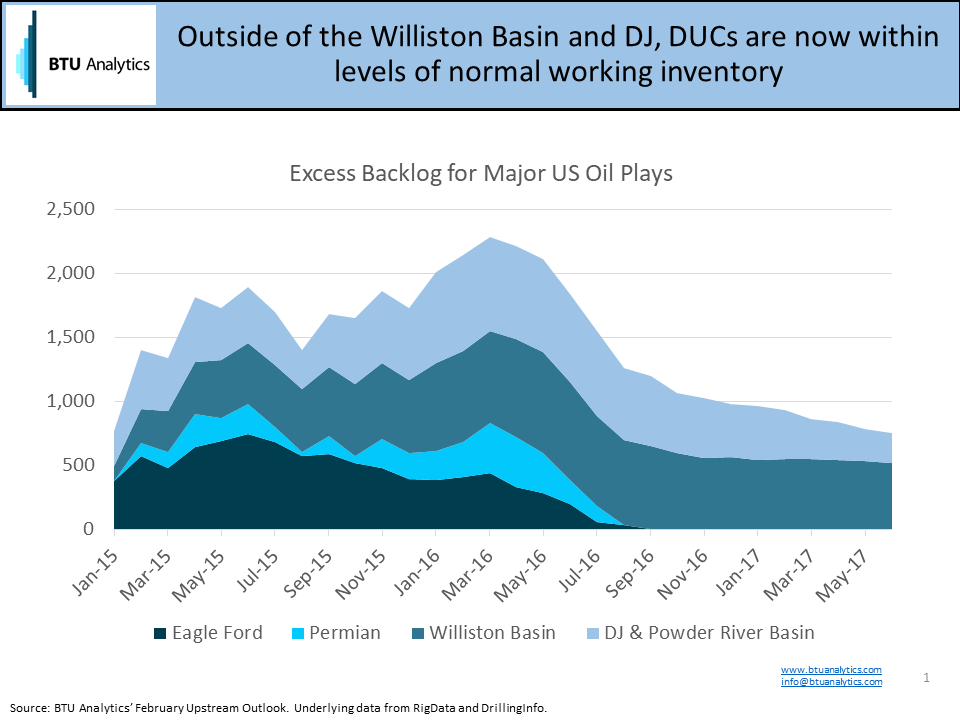

The halted momentum from 2014 left US producers with over 1,000 wells across the major US oil plays in excess backlog in the first quarter of 2015, as illustrated in the chart below.

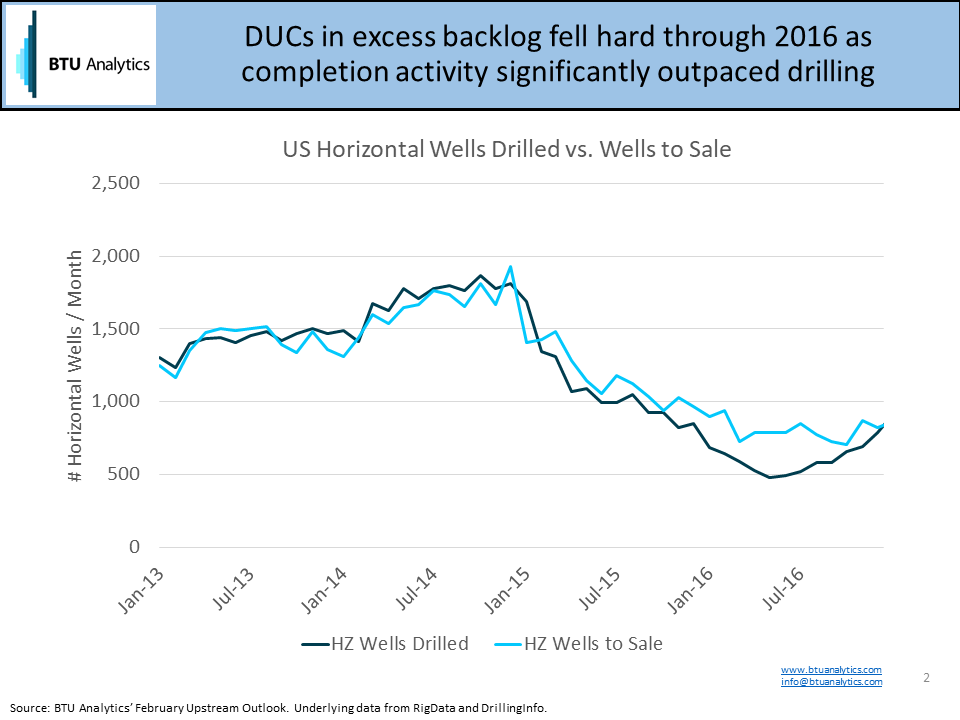

Note that BTU Analytics attempts to differentiate between all DUCs and a level of DUCs outside of what we consider to be normal working inventory by only focusing on the number of wells beyond normal working inventory, which we define as excess backlog. This number grew to over 2,000 by Q1 2016 as oil prices fell to new lows and producers cut both drilling and completion activity further. However, completion activity exceeded new drilling for 2016, and the current number of DUCs falls within BTU Analytics’ estimate of working inventory in all major plays other than the Williston and DJ.

With the DUC backlog being exhausted across many of the major US oil plays, rig activity returns to the forefront. The ramp in rigs in the Permian has the industry regaining some of its former swagger. But production associated with current rig activity in the Permian will begin testing takeaway infrastructure later this year. As producers in the basin push ahead with their development plans without fully considering the impact of herd mentality, BTU Analytics expects excess backlog in the basin to grow once again (Permian Uncompleted Wells? PUCS!).

And now the teaser: for more details on our excess inventory forecast in the Permian, the timing and intensity of takeaway constraints, and what’s going to happen to all those Williston DUCs, request more information on BTU Analytic’s Upstream Outlook.