Two weeks ago, BTU Analytics published a free analysis of how the market has been rewarding capital discipline versus overspending in the E&P space over the last year. While rewarding / punishing the stock price is a critical element to influence decision makers within each company, management compensation incentives are also meant to influence behavior. Some investors have openly criticized the industry for chasing production growth rather than profits, and this analysis looks at how executive incentives at twenty of the largest US producers could play into those claims.

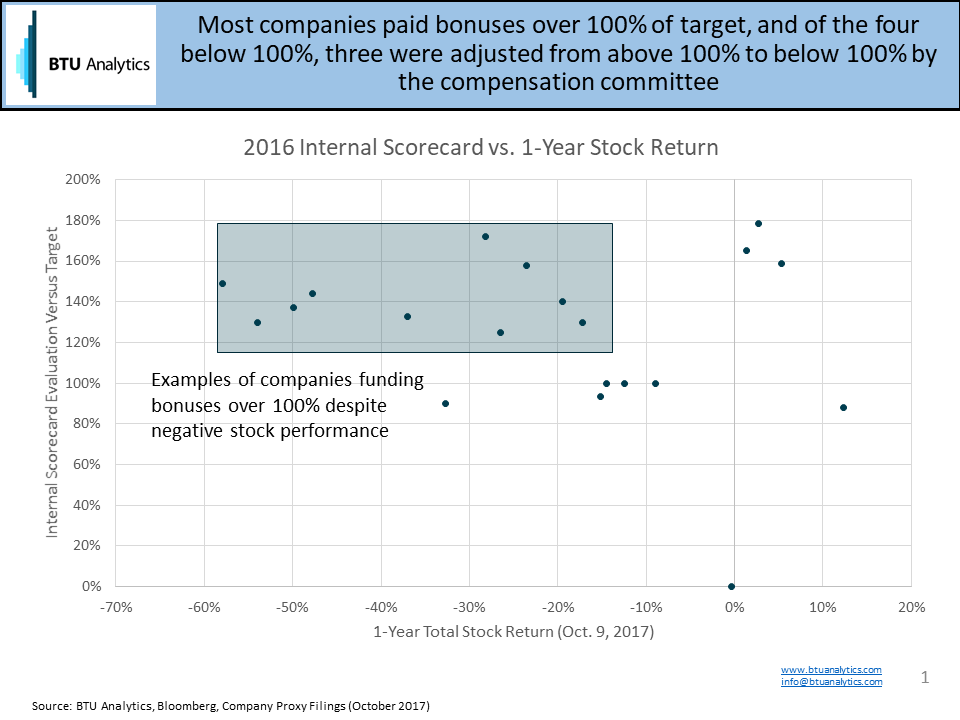

On the surface, it’s not difficult to understand why an investor might be upset if executives receive extra bonuses for reaching performance metrics, including production growth, while stock prices and profits are down significantly. As seen in the chart below, this has happened frequently over the last year.

Almost all companies have a performance scorecard with many performance metrics (production, EBITDA, safety, expenses, etc.) that are weighted to calculate an overall performance score. This impacts executives because if the overall score is 150%, then their bonus is 50% higher than the target bonus, which can increase their pay by millions of dollars.

Simply believing that executives shouldn’t receive bonuses above the target bonus level because the stock performed negatively is an oversimplified conclusion. Perhaps a company’s stock would have performed even worse if not for exceptional leadership and decision making by executives. One might argue that executives cannot control commodity prices, so should they really be punished because of the price environment? But the question still looms – should production growth be a primary metric influencing executive compensation?

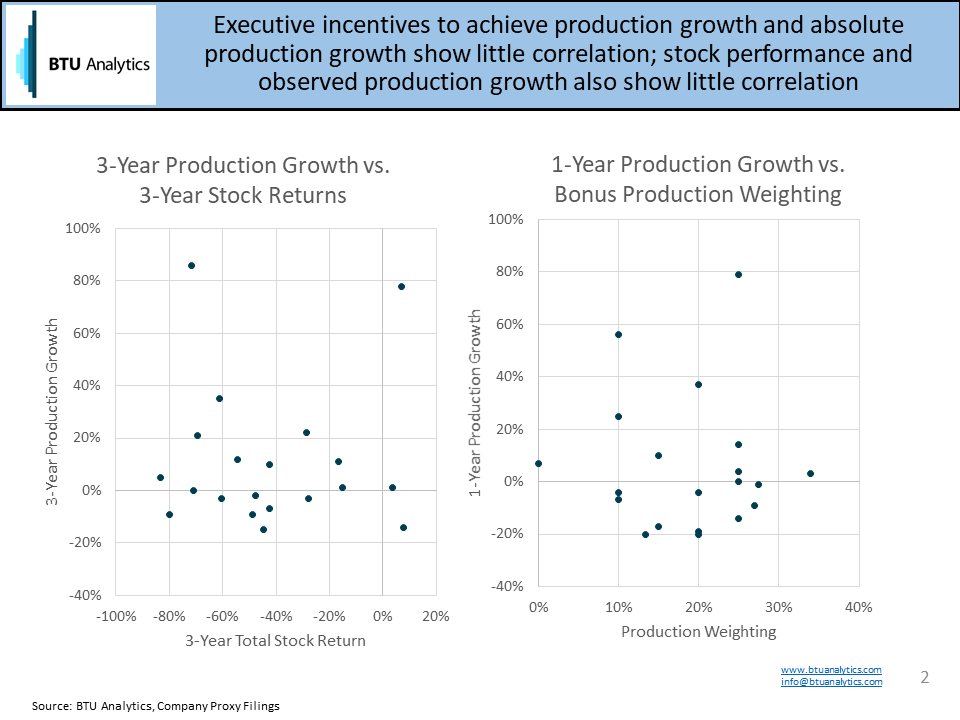

Investors should care about incentives because they don’t want companies chasing any specific metric at the expense of long-term value creation. The analysis below shows little correlation between production growth and stock returns, with similar finding for the relationship between production growth and the weight given to production growth in executive compensation packages. This supports the finding that executives and the market are focused on more than just production growth.

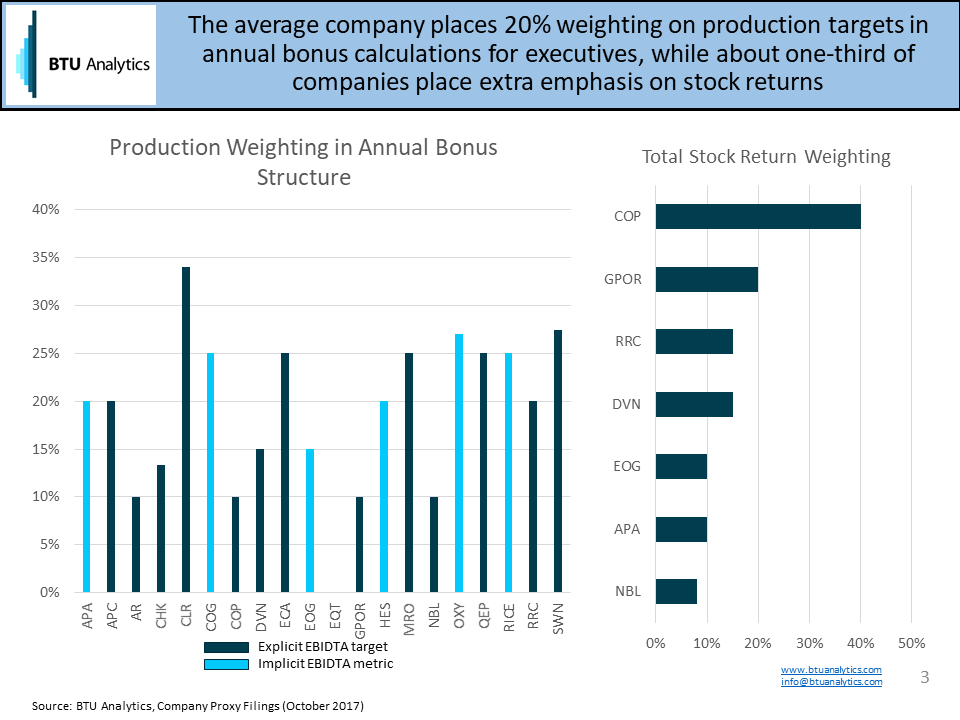

Almost all of the companies in this sample place significant emphasis on production growth in their incentives, and all companies either implicitly or explicitly emphasize EBITDA. In addition, about one-third of the companies in the sample also included one-year stock performance relative to a peer group in the annual bonus calculation.

In response to investor demands, many companies have announced updates to incentive structures over the last year to further align with shareholder interests. EQT removed production metrics from their long-term compensation program last month, and numerous others have reduced the emphasis on operating metrics or added more financial benchmarks. BTU Analytics continuously monitors and models how cash flow, spending, and production trends will impact the market, and the dynamics will continue to shift over the next month as third-quarter earnings are announced. Get the updated operator-level insights in the E&P Positioning Report, and create customized production or cash flow scenarios using BTU Analytics’ proprietary models.