Still reeling from the momentum lost during the COVID-19 pandemic, Williston basin producers have struggled to realize the consistent oil production growth seen prior to 2020. In recent years, the basin has faced several hurtles to oil production growth, primarily centered around associated gas production. Rising gas-to-oil ratios, reduced premium inventories, more restrictive flaring regulations, and company-level ESG targets have all led to more in-basin gas. These higher recovery levels, coupled with the inability to flare excess gas, mean producers must secure gas takeaway to grow oil production in the region. While Northern Border Pipeline (NBPL) has historically been the marginal pipe for additional Williston gas, Canadian producers are unlikely to relinquish their firm capacity on the pipeline due to their own flaring and oil growth objectives. Therefore, without additional pipeline expansions out of the area, only modest room for Williston gas production growth remains.

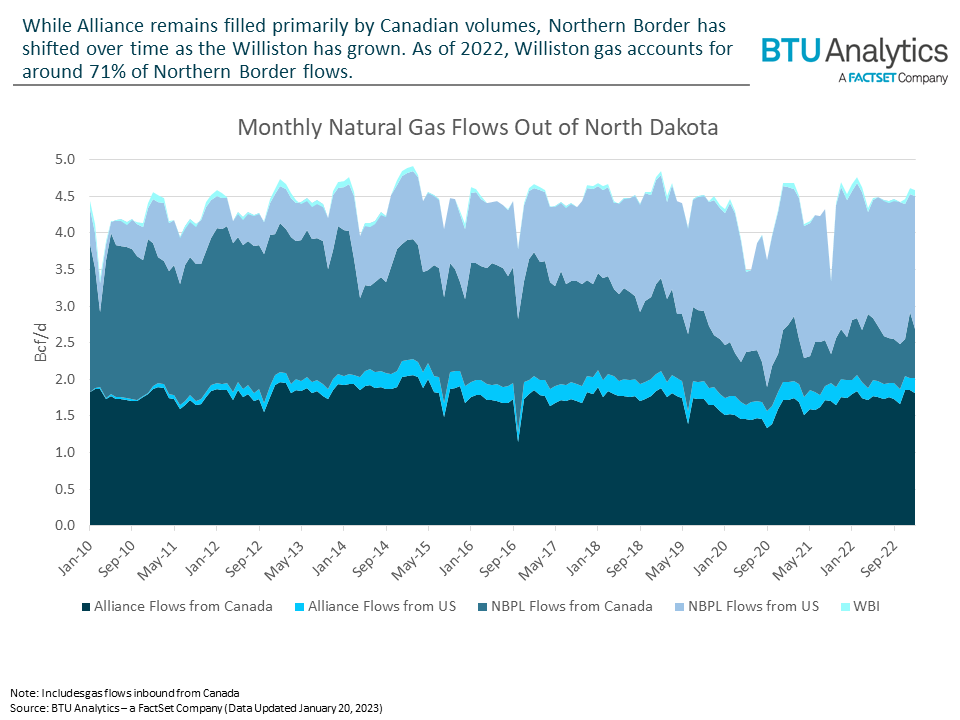

Currently, three main avenues exist for gas to leave the Williston: Williston Basin Interstate (WBI), Alliance Pipeline, and NBPL. WBI, the smallest capacity pipe out of the basin, takes an immaterial 30 MMcf/d of Williston gas to CIG on average each year. While Alliance has 2 Bcf/d of capacity, it primarily functions as a passthrough pipeline for Canadian gas heading to the Midwest, leaving space for only 220 MMcf/d of Williston gas. Originating in Canada, NBPL’s 2.5 Bcf/d of capacity supports the majority of gas flows out of the region. It is also the only pipeline with shifting dynamics, as Williston gas growth has led to gradually displaced Canadian volumes over time. In 2022, an average of ~1.8 Bcf/d of Williston gas flowed on NBPL, accounting for just over 70% of available capacity.

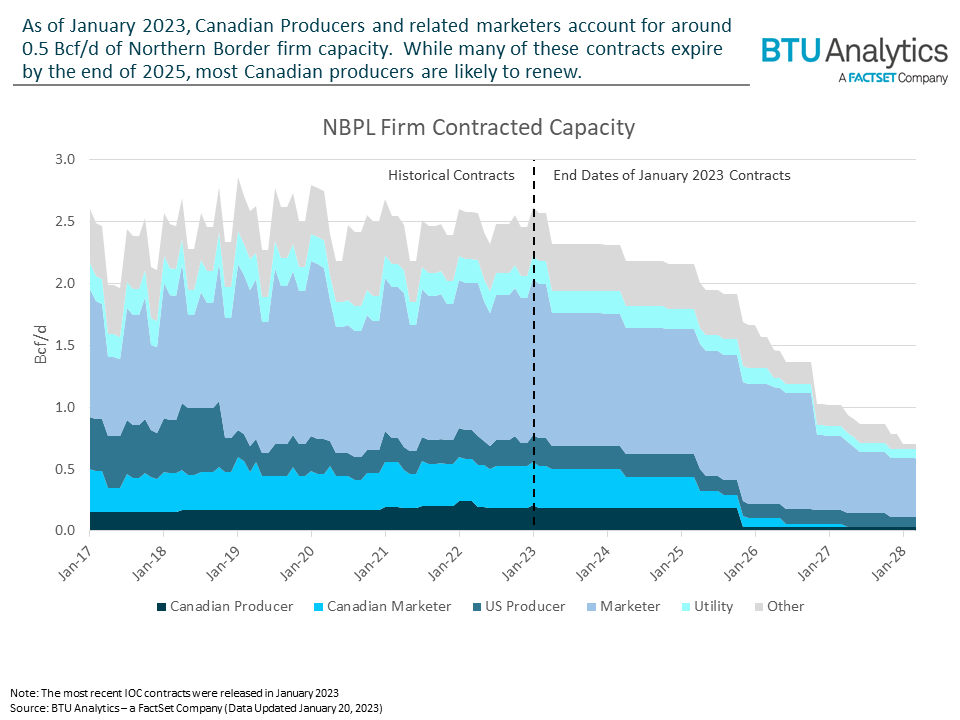

However, it is unlikely this NBPL displacement dynamic will be able to extend through the pipeline’s entire capacity. Since 2017, Canadian producers and associated marketers have consistently held around 0.5 Bcf/d of firm transport capacity on NBPL. Similar to the Williston, Canadian producers are subject to flaring regulations that ultimately require them to find markets for their gas to continue liquids production. This has led some Canadian producers to secure capacity with firm transportation (FT) contracts, which are evergreen and provide renewal preference. This makes them particularly difficult, if not impossible, to displace. In 2022, an average of 0.7 Bcf/d of Canadian gas flowed on NBPL. Even if Williston operators are able to broker deals with Canadian marketers, this leaves 0.5 Bcf/d of space, at most, for Williston gas growth.

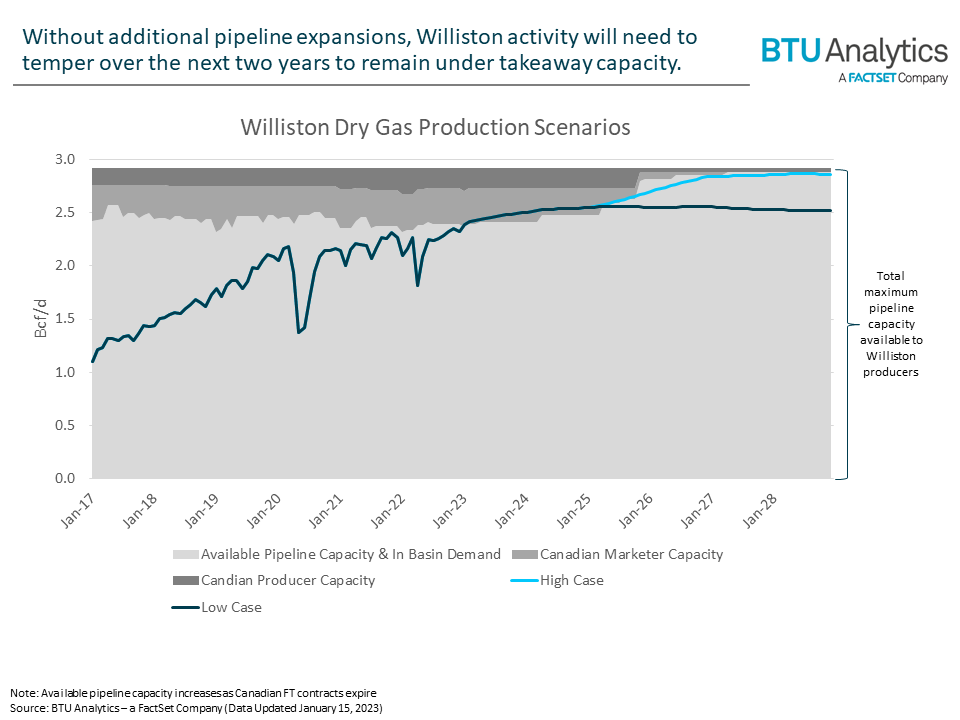

Regardless of the fluidity of Canadian FT contracts, the Williston must temper gas production growth over the next two years. Assuming Canadian marketers are indifferent to where the gas originates and are willing to purchase more Williston volumes, the basin can expect around 325 MMcf/d of growth through 2024. At that point, two scenarios arise. If Williston producers can take over expiring Canadian contracts, the basin can continue growing in 2025 and fill NBPL by 2027. However, if these final Canadian volumes cannot be pushed out, Williston producers will be forced to hold gas production flat.

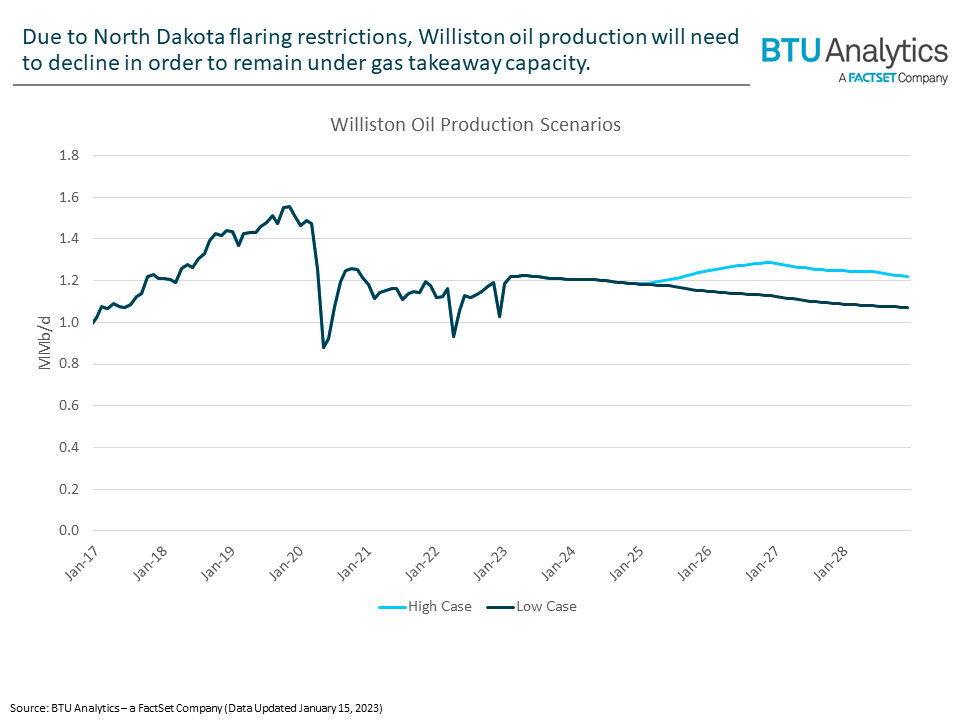

Both production scenarios have notable impacts on oil outputs. These scenarios suggest Williston oil production would decline over the next two years due to limited gas takeaway. Similar to the gas scenarios, if Canadian contracts can be captured in 2025, oil production can again grow through 2026 before stalling.

A reversal of Bison Pipeline has been proposed as a potential partial solution to the issue. Bison is currently designed to flow north from Wyoming into the Williston but now stands empty. The proposal would reverse flows south to Wyoming and add 430 MMcf/d of capacity on NBPL north of the Bison interconnect to create space for NBPL flows to fill Bison south. However, the expansion has garnered little interest from producers so far. As NBPL is a rich pipeline, higher rates of ethane recovery could stand as another option. BTU Analytics currently models the Williston to be rejecting 147 MMcf/d of ethane onto NBPL. Provided there is the necessary gas processing infrastructure, recovering these volumes could provide additional space on NBPL. In the March edition of the Upstream Outlook, BTU Analytics will dive deeper into these issues and their effects on the Williston forecast moving forward.