Analysts have been calling for the resurgence of the Haynesville shale since drilling fell precipitously back in 2011/2012. But lower cost natural gas supply from oil focused activity and the Marcellus and Utica has blocked any meaningful recovery…. until now.

With new infrastructure projects connecting Marcellus and Utica gas to the rest of the market facing growing headwinds (See Atlantic Sunrise delay announced this morning), is the Haynesville shale finally ready for its moment?

BHP Billiton (NYSE:BHP) announced earlier this month that it was resuming a Haynesville shale program after locking in hedges and supply contracts. This marks a change in strategy for the company, which previously eschewed hedging across its entire minerals and petroleum portfolio and instead sold production on the spot market. Chesapeake Energy (NYSE: CHK) has been buzzing about increasing productivity and efficiency in the Haynesville shale for quite some time (PROP-A-GEDDON!) But at what point does buzz translate to growth in Haynesville shale gas production?

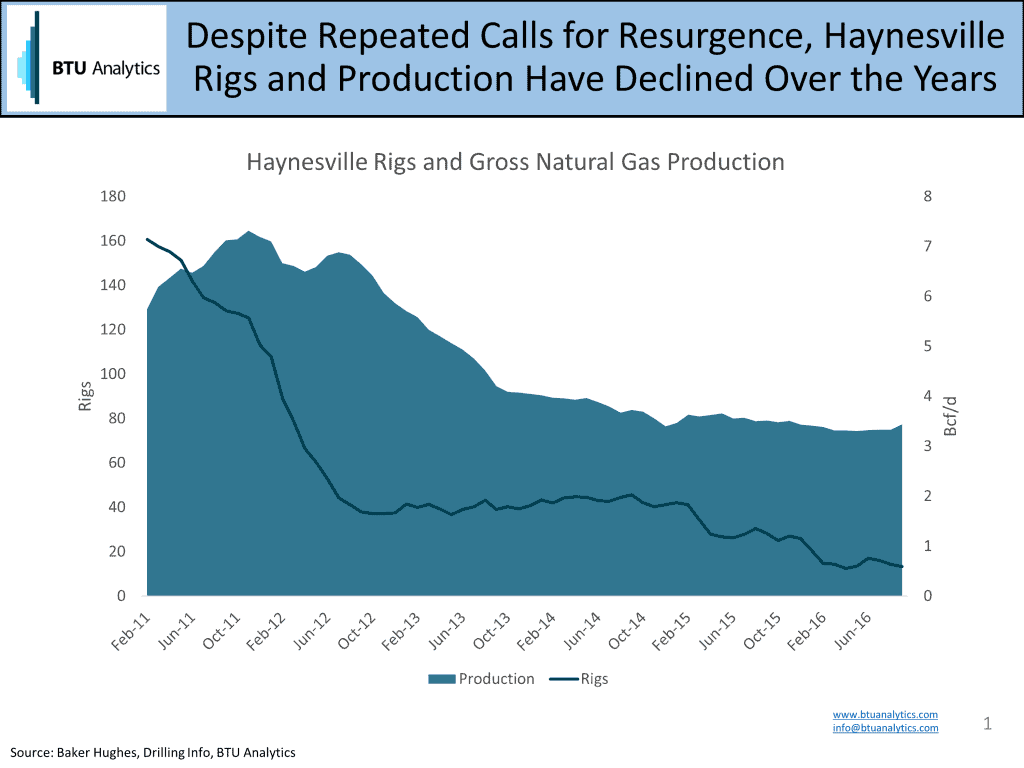

The chart below shows the Haynesville rig count and production. In 2016, an average of 16 rigs ran in the Haynesville, compared to a peak rig count of over 180 rigs in 2010. Production has fallen from 7 Bcf/d in late 2011 to approximately 3.5 Bcf/d today. But notice that the production declines in the Haynesville shale seem to have stagnated more recently. Basin production appears to have reached an inflection point.

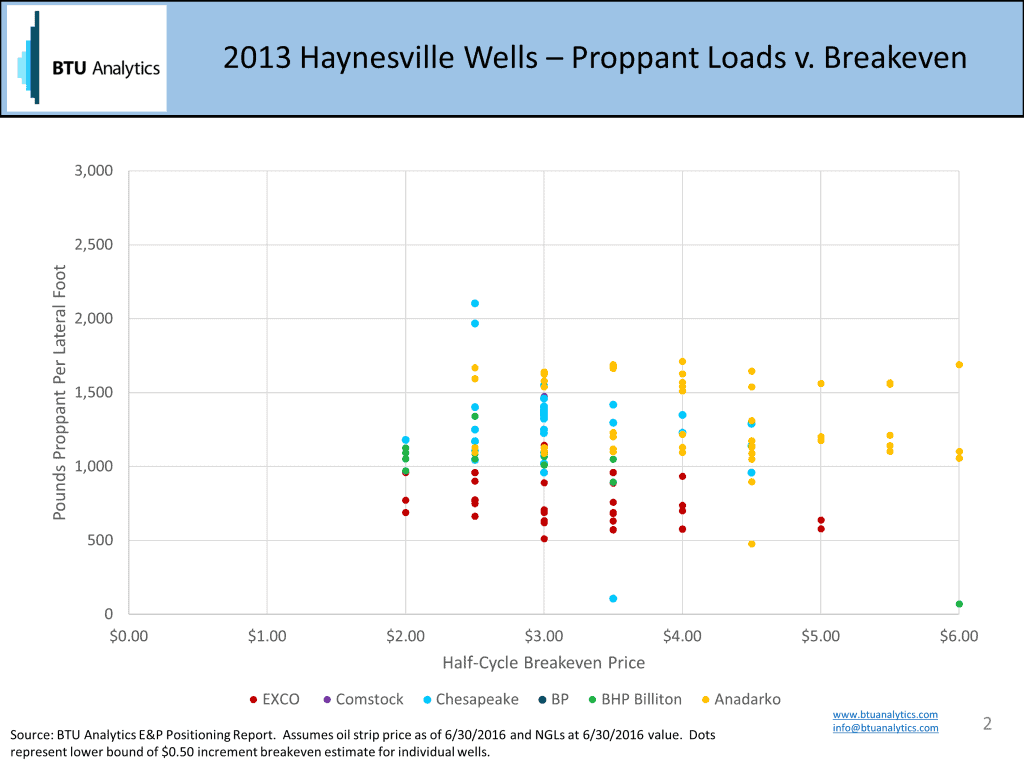

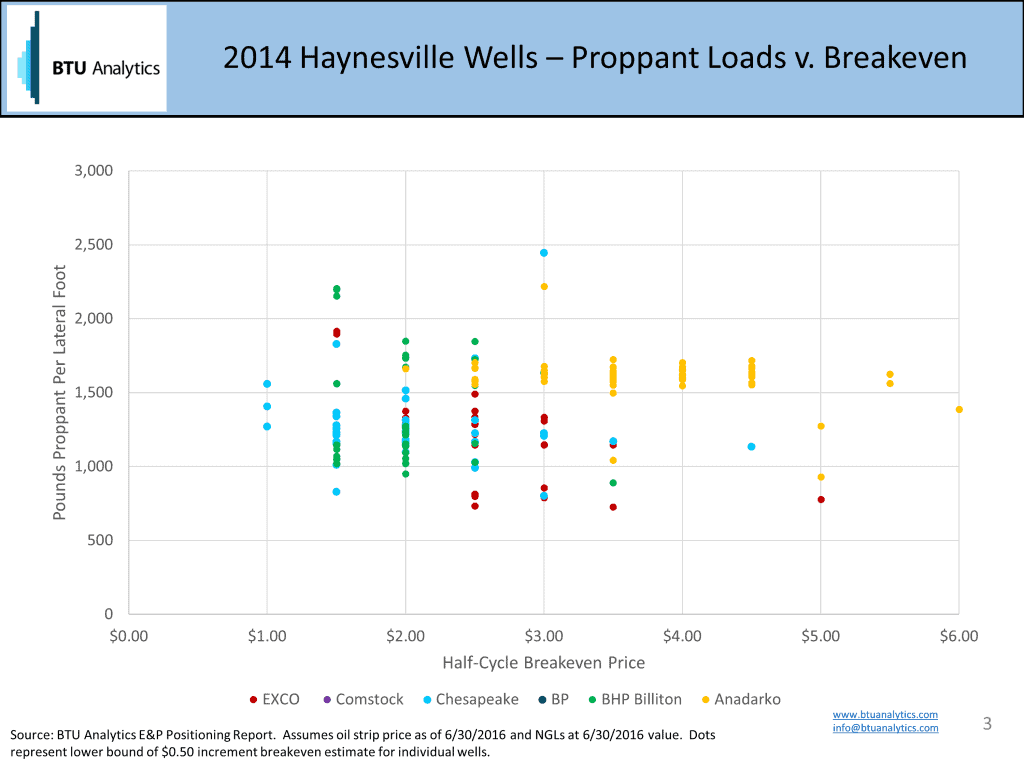

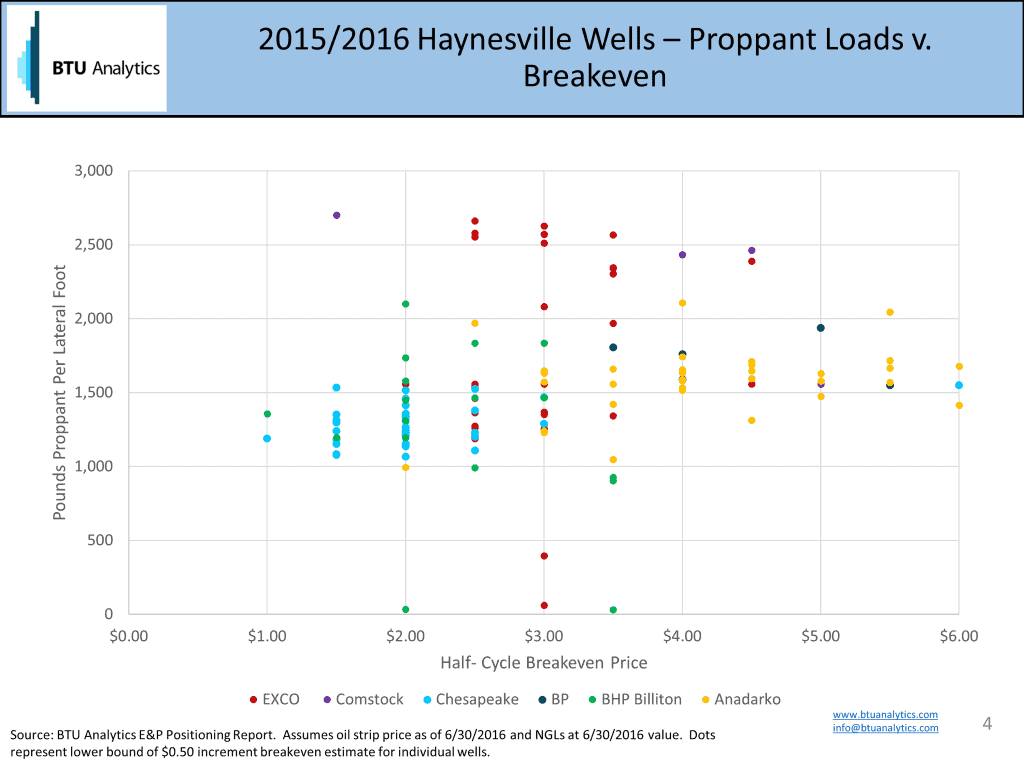

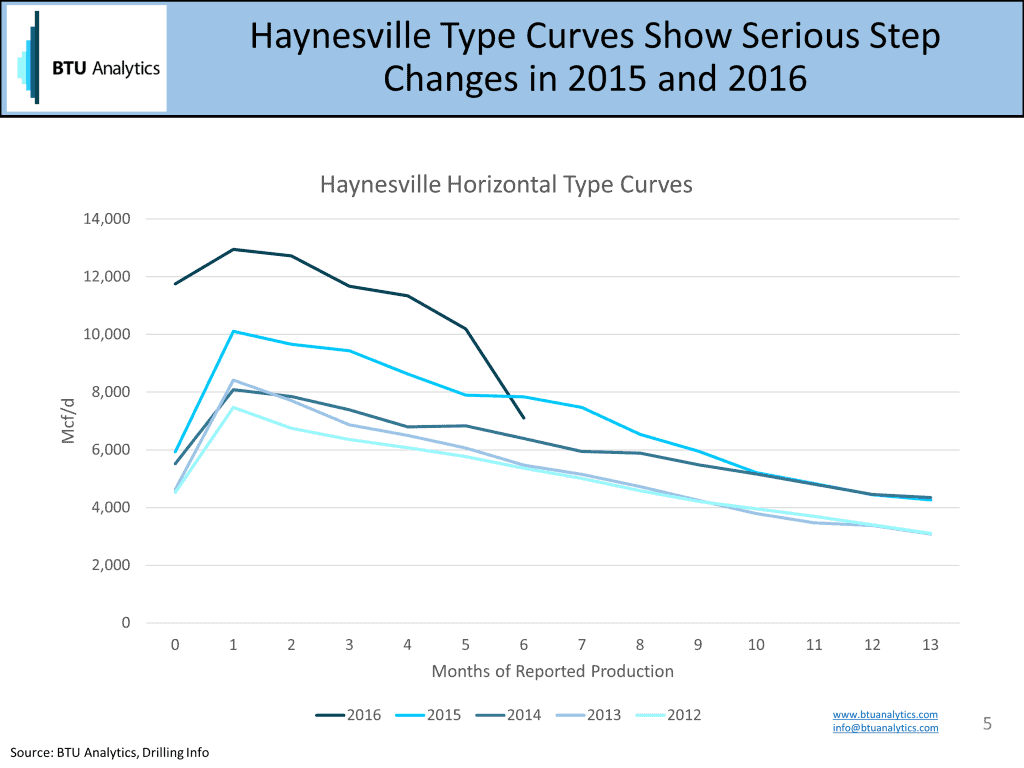

But why now? The natural gas strip and rig count were significantly higher back in 2014, and production declines continued. While we generally remain skeptical of producer claims that we can’t verify (see: Buyer Beware), well productivity and cost efficiency are lowering the breakeven costs of some operators. The next three charts show how breakeven prices have been impacted over time by one factor, proppant intensity. Note that each dot reflects an individual well, and the breakeven price in the chart is actually the lower bound of a $0.50 range (a $3.00 dot represents a well in the breakeven range of $3.00-$3.50.) In 2013, wells turned to sales generally had proppant loads of 500-1,500 lbs of proppant per lateral foot, jumping to 1,000-2,000 in 2015/2016.

It is interesting that even though proppant loadings continued to change from 2014 to 2015/2016, breakeven prices didn’t necessarily fall for the majority of operators as they did from 2013 to 2014. It seems that there are limits to the idea that more sand is always better for economic outcomes.

Even if 3,000 lbs of proppant per lateral foot dosen’t become the norm, lower breakeven costs for many of the basin’s largest operators in combination with a constructive outlook for the gas market over the next few years provides a meaningful opportunity that we expect select producers to jump on. And faster drilling times along with average basin IP rates 75% higher than 2012 mean that if rig additions seen in the past few weeks continue, it won’t be long before Haynesville shale production is growing once again.

For more detailed analysis on the Haynesville shale and its expected impact on the natural gas market, learn more about our Upstream Outlook and E&P Positioning Report services. The Q3 E&P Positioning Report is being released next week and features detailed thoughts on the factors impacting Haynesville shale production and growth.