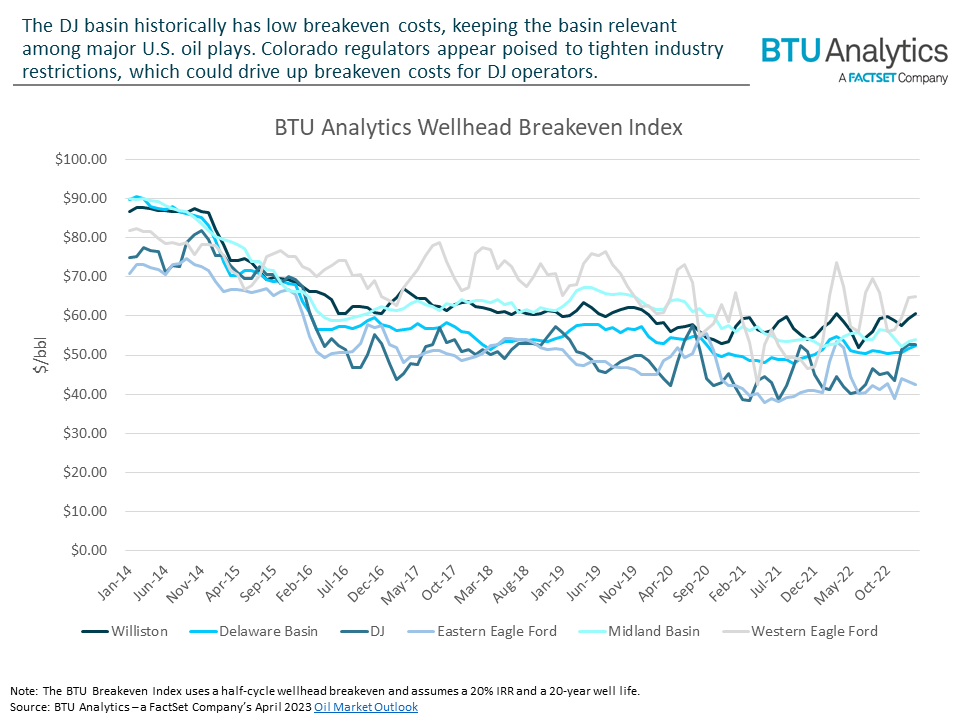

Colorado’s Denver-Julesburg (DJ) basin has historically been a strong region for oil production, producing 590 Mb/d of oil at its peak in November 2019. Some of this strength is attributed to low breakeven costs in the DJ ranking consistently below other major U.S. oil plays, undercutting even the Midland basin. The DJ’s Niobrara formation can accommodate wells with shallower verticals, yielding more wells per active rig than any other major oil-directed basin in the country. However, despite the basin’s advantages, DJ drilling activity began falling in 2019, and a stricter regulatory environment muted the return to historical levels seen in other oil-directed regions last year. Limited breakeven inventory in the basin and more proposals from Colorado legislators suggest the basin may have further to fall from grace.

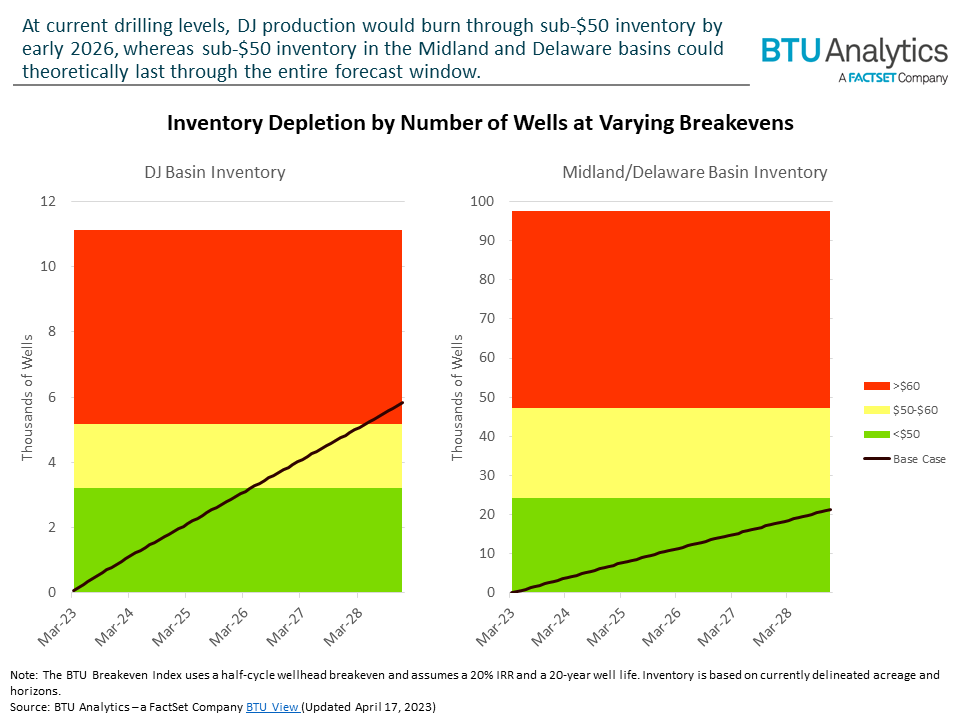

The most immediate risk to the basin’s prominence is the status of remaining inventory. BTU Analytics’ currently estimates the DJ basin has slightly over 11,000 undrilled locations. Assuming all low-cost inventory is drilled first, BTU Analytics’ projects less than three years’ worth of sub-$50 breakeven wells remain in the DJ basin. Under BTU Analytics’ latest WTI forecast, the majority of wells are economic when confining the lens to the wellhead breakevens and thus make the decision to produce appear easy. However, the higher corporate breakeven price combined with a restrictive regulatory environment could quickly make the DJ less economic within the medium term.

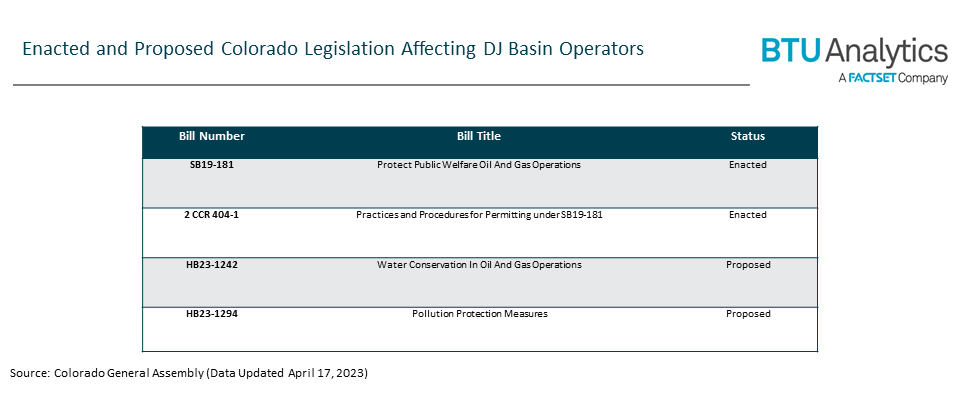

The financial viability of DJ wells may be further challenged by a series of proposed bills from the Colorado legislature. House Bills 1242 and 1292, respectively proposed on March 11th and April 13th, 2023, indicate a continued appetite for tighter regulation on oil and gas companies operating in the state. In 2019, Senate Bill 181 was signed into law and altered the well permitting process. Economies of scale became especially advantageous as operators sought to capitalize on a well-batching clause, driving significant operator consolidation. From the start of 2014 through August 2019, 106 operators drilled in the DJ basin. Since then, the number of operators in the basin dropped 57%, and activity is down from a height of 30 active rigs per month to averaging only 11.

This renewed regulatory momentum in 2023 could further inhibit production growth in the DJ basin as well. The Colorado House of Representatives introduced HB23-1242 to limit freshwater use in oil and gas operations to a maximum of 25% of total water use by 2027 and a maximum of 10% by 2030. The hurdle the industry would face in order to comply with this regulation is seen in Civitas’ 2022 Sustainability Report in which the large DJ basin producer states that around 97% of their total water use is comprised of freshwater. A month after HB23-1242 was introduced, the House introduced HB23-1294, which would, among other things, penalize producers for emissions violations that occur during system start-up, shutdown, and malfunctions. The bill appears to take tangible steps toward Colorado Governor Jared Polis’s mandate to cut the oil and gas industry’s ozone pollution by 30% by 2025 and 50% by 2030.

As producers come to terms with the growing challenges of operating in the DJ basin, forecasts risk overestimating basin activity. In fact, Jeremy Nichols, Director of Climate and Energy Programs at WildEarth Guardians, told the Colorado Sun in March that the ozone mandate “…will necessarily require [the oil and gas] industry to reduce its footprint, eliminate infrastructure, and scale back its future expansion plans.” BTU Analytics expects the DJ’s comparatively low breakevens to be driven upwards by the increased costs of reducing nitrogen oxide emissions and sourcing, recycling, and storing produced water. As operator behavior in the DJ basin responds to shifts in basin dynamics, be sure to read more coverage in the May 2023 edition of BTU Analytics’ Upstream Outlook.