As 2017 ends, we are continuing preparations for our annual conference in Houston on February 22, 2018. As part of that preparation, we recently reviewed our Best Energy Market Calls in 2017 from our 2017 What Lies Ahead conference.

At our 2018 What Lies Ahead conference, we intend to cover 6 major themes:

- Permian, SCOOP, STACK – The Curse of Abundance

- At Odds with Breakevens: E&P Performance vs Economic Reality

- Hedging and Capital Discipline: The Impacts to Capital Investment and Supply Growth

- At Last? New Pipe Capacity and the Next Phase of Northeast Production

- The ARC of Pain – How New Pipelines, Exports, and Renewables Impact Henry Hub

- The Future of Energy: LNG, Electric Vehicles and US Inventory Depletion

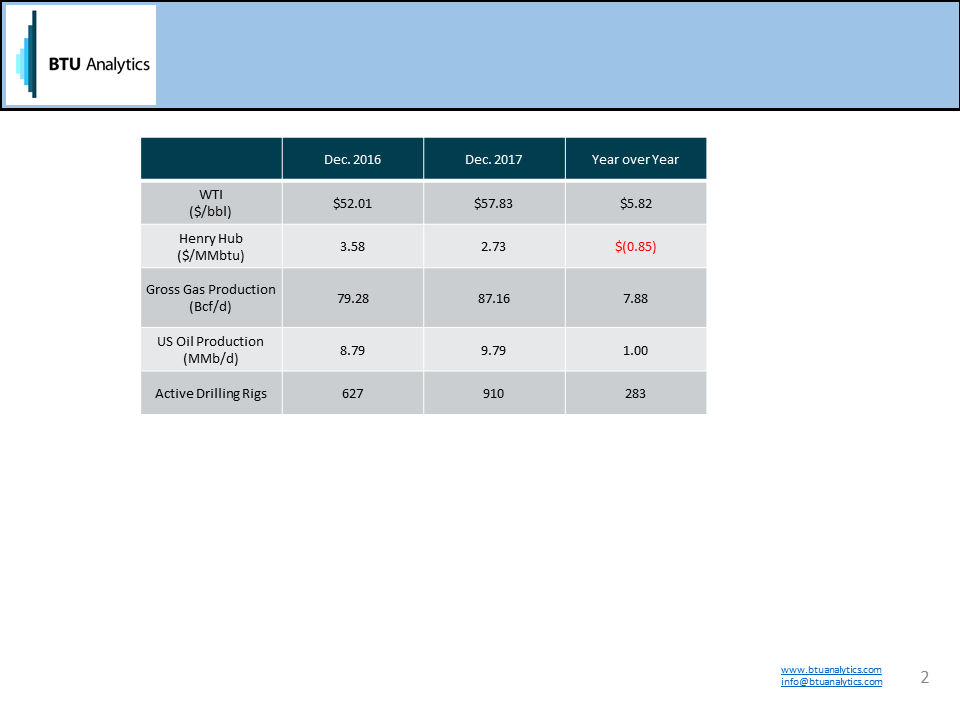

2017, like all years in the energy markets, has been filled with change. The table below highlights the changes in commodity prices, production, and drilling rigs in the US over the last twelve months.

Over the last 12 months, oil prices have risen nearly $6.00 per barrel, spurring a surge in E&P capital spending on acreage acquisitions and drilling in the Permian and the SCOOP & STACK. Additionally, the Marcellus & Utica have added over 3.5 Bcf/d of new pipeline capacity in 2017, prompting producers to increase activity to satisfy pipeline commitments made years ago when Henry Hub prices were much stronger than the $2.73 average in December 2017. New pipeline capacity in the Northeast along with oil investments in other regions have spurred US gross natural gas production to average an estimated 7.9 Bcf/d higher in December 2017 versus a year ago. The rampant growth in natural gas supply has left natural gas prices languishing below $3.00 despite brutally cold weather in the upper Midwest and Northeast this week. Unless US E&Ps bow to shareholder concerns over capital discipline, the outlook for natural gas prices in 2018 may only get worse if crude prices continue to strengthen.

Natural gas volumes aren’t the only volumes that have risen in 2017. Crude production has rebounded from declines and will exit 2017 nearly 1.00 MMb/d higher than a year ago, driven by the 280+ rigs added during 2017. However, the production potential would have been even higher had completion crews managed to keep up with E&Ps drilling plans.

Our 2018 conference (Full Agenda Here) is shaping up to have lots to talk about this year with continued OPEC Cuts, drilling rig additions, continued structural demand growth for natural gas from LNG and Mexico, and new labor and capital market dynamics potentially impacting the ability for US producers to meet changing global demand dynamics.

With only a few days left to sign up for our 2018 What Lies Ahead Conference on a discounted basis, make sure to reserve your seat. We look forward to another interesting year for North American and global energy markets.

Happy New Year from BTU Analytics!