When times are good, operators tend to look the other way when it comes to taking on additional costs. However, when times are tight, and the future does not seem as bright, all costs come under the magnifying glass, as is the case in the market today. We have seen this in recent announcements by many operators, including Chesapeake who announced they would be laying off 19% of their corporate employees in Oklahoma City in Fall 2015 and Southwestern who today announced they would be releasing almost half of their workforce. With this in mind, BTU Analytics decided to dive deeper and look into which companies have the best track record of doing the most with the least amount of human resources with the idea that the most streamlined companies may weather the current storm better than others.

At BTU we spend a lot of time looking at half cycle economics. In this blog we take a slightly different approach to look at production, revenue normalized to number of employees. Half-cycle economics considers the marginal cost of adding an additional well, for example, while with full cycle economics you must take into account additional costs such as acreage acquisition costs and general and administrative costs, which include employee salaries and benefits.

To keep the analysis relatively simple, we looked at exclusively small and mid-cap companies, as these selected companies operate exclusively in North America and don’t have the massive cash coffers and high staff counts of the large caps. This will help us to avoid any significant revenue made by international operations and the accounting minutia that comes with being a large-cap and/or super major.

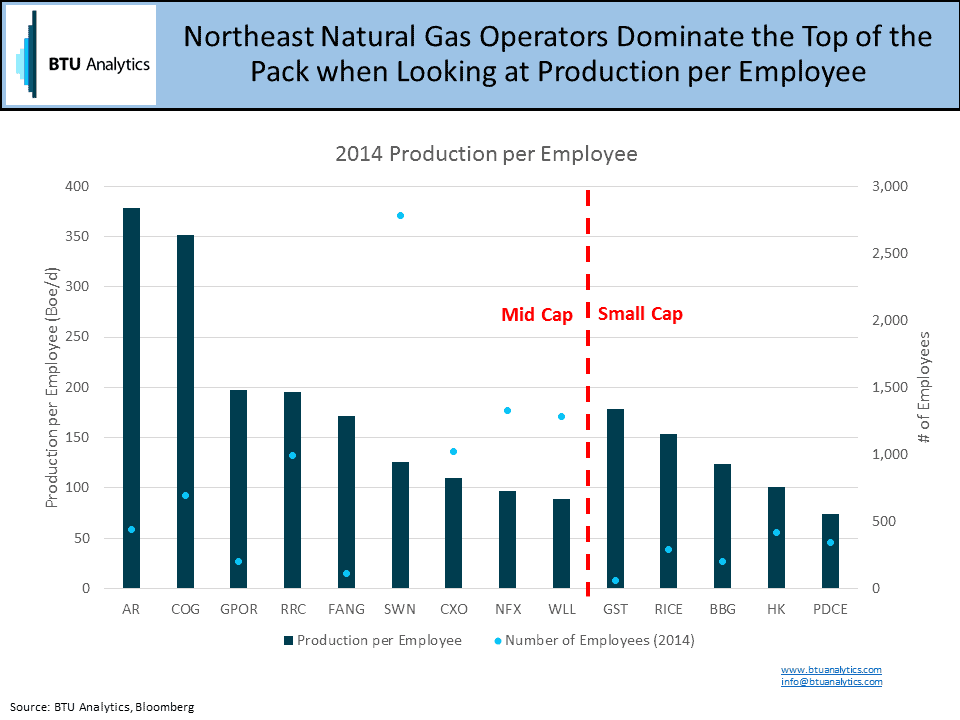

The first metric to look at is production per employee. This gives us insight into the producer’s operational efficiencies when controlled for the number of employees. The graphic below shows the ratio of barrels of oil equivalent produced daily to the number of employees. The first thing that stands out is that the top of the pack is dominated by Appalachian natural gas producers such as Antero (AR), Cabot (COG), and Gulfport (GPOR) who have a relatively small workforce and prolific acreage. The second thing that stands out is the relatively small amount of production associated with Southwestern’s (SWN) large workforce, which, among other things, was surely part of the impetus behind their announcement today.

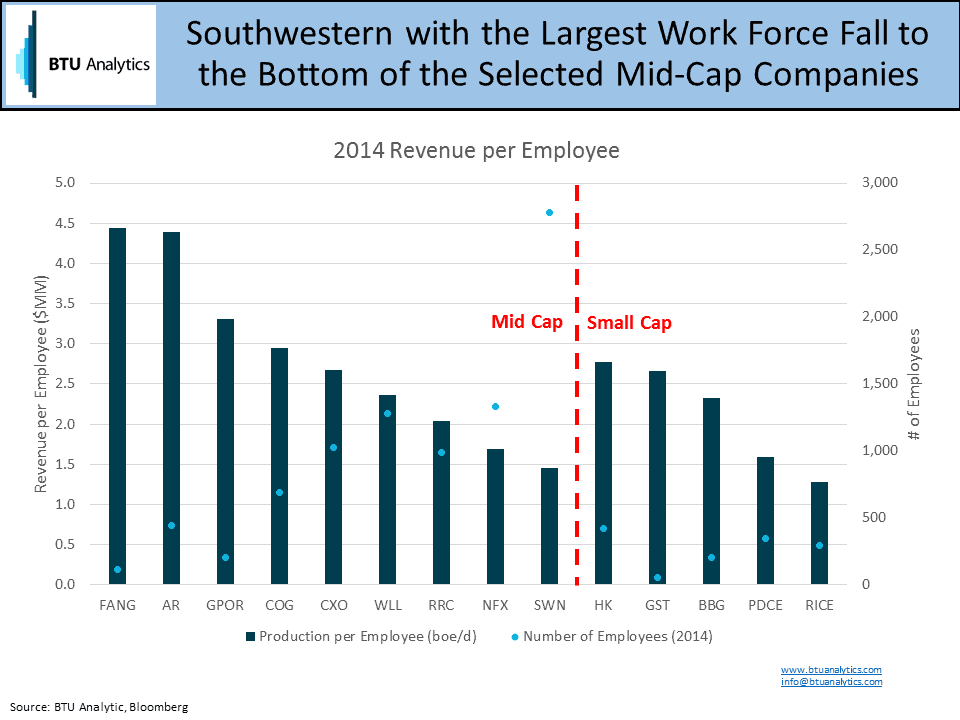

We can go one step beyond looking at production and incorporate additional aspects of the business, such as the effects of hedging, marketing, and realized prices, by looking at revenue as it relates to the number of employees. Diamondback Energy (FANG) moves to the top of the list, most likely due to a combination of a very low employee count, acquisitions made in 2014, and somewhat favorable realized prices, while Antero’s position is due to its strong portfolio of hedges.

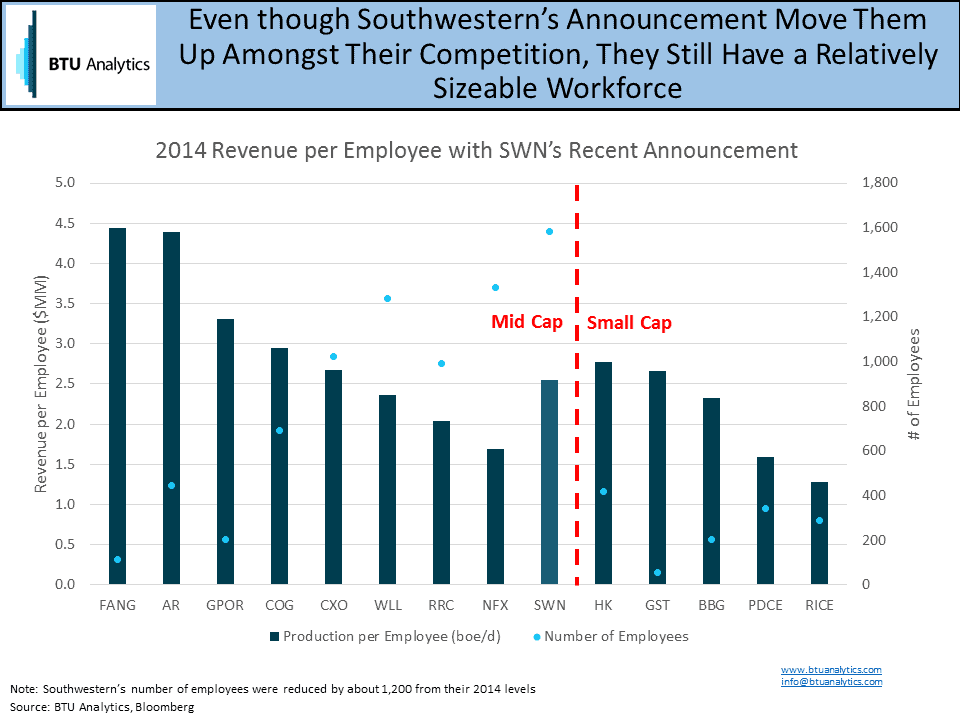

With Southwestern hovering near or at the bottom of the pack for both metrics, let’s look at how their announcement today will affect their standing within our chosen set of mid-cap operators. Since we still do not have full revenue data for 2015 we will use their 2014 data as an approximation. The graphic below shows that even with Southwestern’s announced layoffs, while they do move up among their competition, they are still middle of the pack and still have a sizable workforce.

While this only provides a look at historical performance, it gives us an insight into how companies will perform moving forward in a lower-for-longer oil and natural gas price environment. To hear more about BTU Analytics’ market views, join us for our What Lies Ahead Conference in Houston, TX on February 4, 2016.