Bernie Sanders said in a campaign speech in Binghamton, NY this week that if ‘you’re serious about combating climate change, we need to put an end to fracking’. One of Sanders’ campaign’s slogans is ‘feel the Bern’ but these comments would make the natural gas market ‘feel the burn’. Banning fracking has all sorts of implications to energy markets, labor markets, state economies, the list goes on. From the natural gas and power market perspective, banning fracking would make natural gas production drop precipitously, natural gas prices would leap higher which would send the electric generation market into a fuel switching frenzy, where despite the most bullish wind and solar forecasts, king coal would be forced to backfill generation. While this policy decision is highly unlikely, this blog will take a closer look at 1) the prospective impact of a fracking ban on US natural gas and oil production and 2) how the US power generation market would likely respond. Unfortunately for Mr. Sanders the outcomes are far from his desired intentions – higher emissions and higher prices.

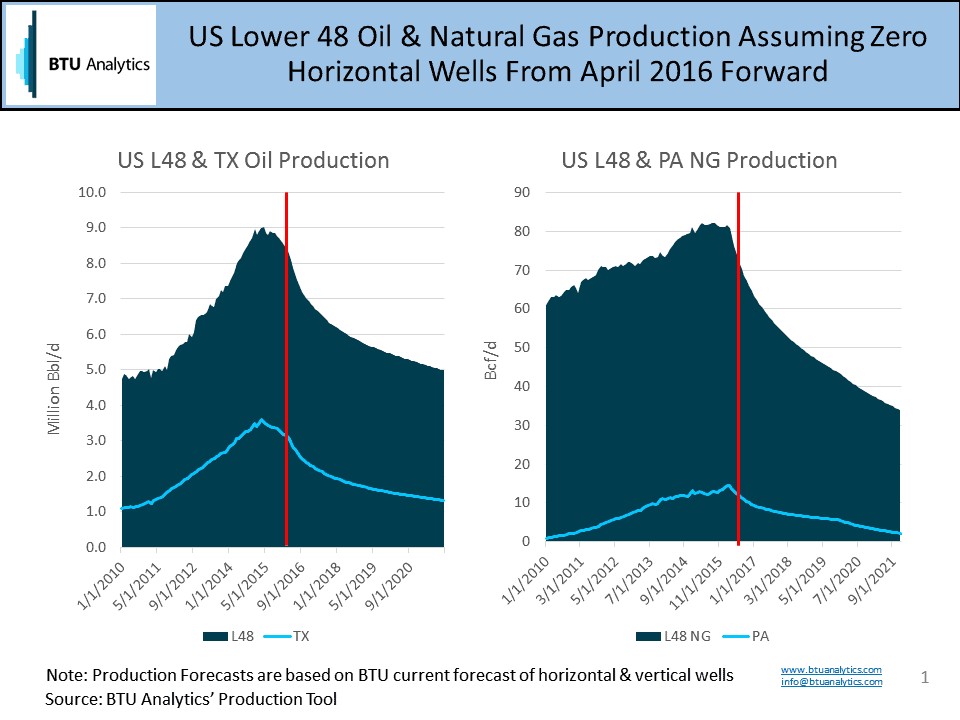

In the slide below, the impact of the current commodity price correction can be seen as oil and natural gas production grew continuously from 2010 to 2014 and then, due to low prices, production rolled over from 2015 to present (shown by the red line). In order to make a simple approximation on the impact of a fracking ban, BTU took our current oil and natural gas forecast and cut all horizontal rigs out of our wells to sales forecast leaving only vertical activity (this assumes a fracking ban would be on all horizontal wells’ multi-stage frack jobs, while smaller vertical completions would remain). The results are staggering showing oil production declining over 40% between it’s peak in 2014 and 2021, down to 5 million barrels a day (for reference Texas oil production is also shown.) Natural gas would decline even harder, declining 58% from the peak in 2014 to 2021 ending at 34 Bcf/d (likewise the impact to Pennsylvania production is also shown).

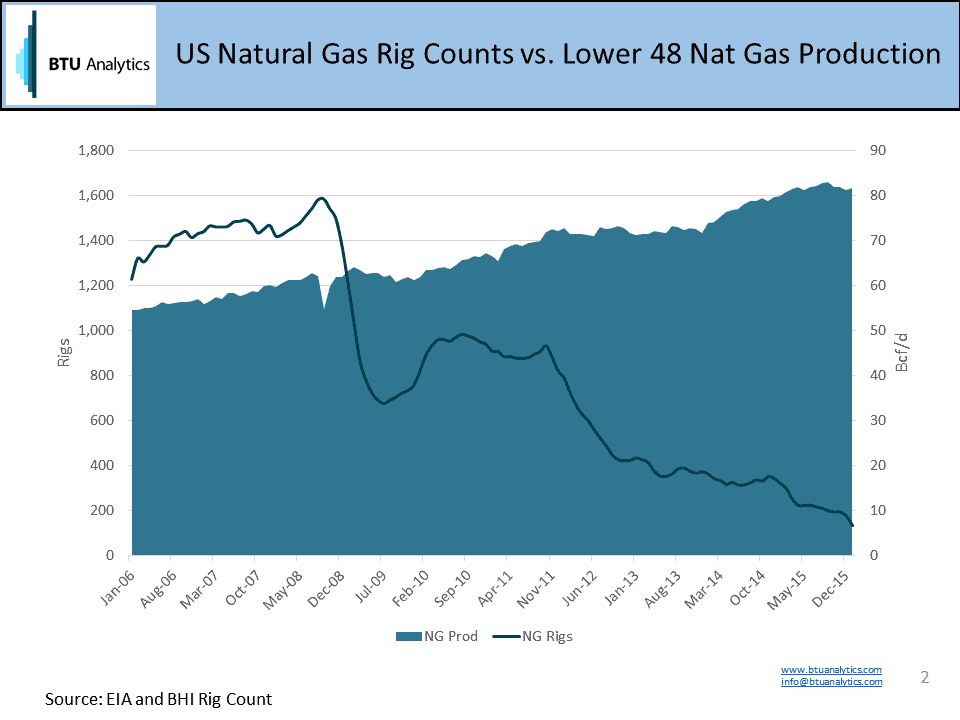

Of course, horizontal rigs make up almost 80% of the current US oil and gas rig fleet. So cutting all horizontal activity has a drastic impact to production and to the marginal cost of production (widely perceived as the dictator of long term natural gas price equilibrium levels). To ban fracking would throw all the efficiency gains achieved by E&Ps over the last decade out the window as shown by the slide below where production climbs higher despite the gas rig count declining over the last decade. The last time the US natural gas market price was set by marginal production from vertical wells was in 2004-2006 when Henry Hub averaged in the $6-$8 per MMBtu price range and spiked to over $15 perMMBtu on volatile days. Currently, Henry Hub natural gas prices trade at about $2.00 per MMBtu today. Further to give some perspective, to keep natural gas production flat through 2021 using vertical wells and current IP rates, the US would have to drill 6,200 vertical gas wells a month for the next 5 years. Today there are 89 gas rigs and 354 oil rigs active in the US.

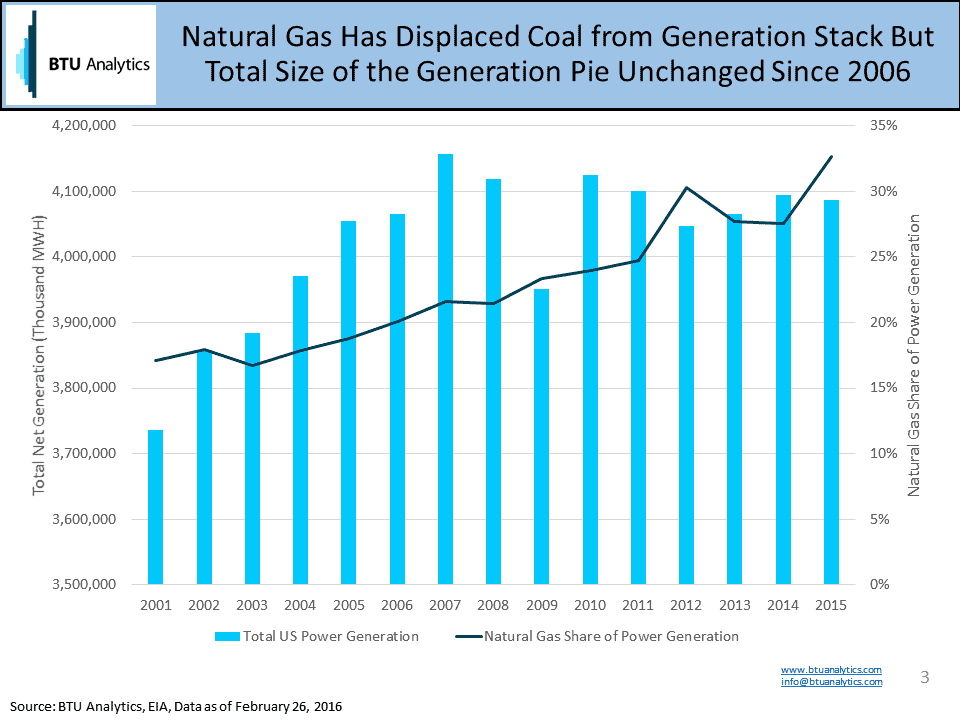

BTU Analytics estimates natural gas-fired power generation, while consistently gaining as a total percentage of US generation (see slide below), has been unable to capture an additional 4 Bcfe/d of demand due to increased generation from solar and wind as state renewable portfolio standards have ratcheted higher over the last 5 years. We estimate by 2021 natural gas will loose another 2 Bcfe/d to wind and solar.

Here is the rub, based on the frack ban estimates above, natural gas production would drop 44 Bcf/d in the next five years hypothetically. If wind and solar have gained 5 Bcf/d of natural gas-fired generation over the last 5 years, the only generation fuel that can backfill natural gas quickly and with scale enough to offset a frack ban production drop, regardless of how bullish a forecast for wind and solar you whip up, would be coal. Quite ironic, considering US coal production is dropping like a rock and Peabody Energy, the largest US coal producer, filed chapter 11 this week. Mr. Sanders’ frack ban plan has renewables and energy efficiency back-filling for fracked natural gas, but in reality, a ban on fracking would increase emissions and prices for oil and gas all to the benefit of coal. If only the rest of the US could be like Vermont, where nuclear generation in 2014 according to the EIA (prior to the shutdown of the Vermont Yankee plant) counts for over 70% of power generation with no emissions – but I forgot Mr. Sanders doesn’t like nukes either.

We are BTU Analytics and we approve the contents of this message.