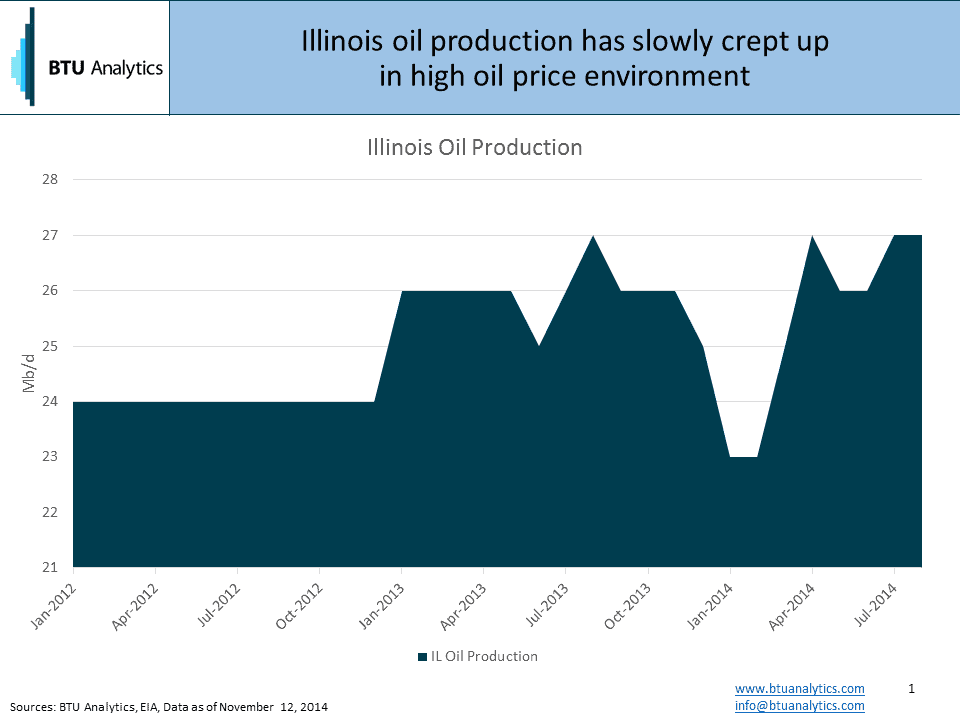

With oil prices falling to below $80, the focus has been keenly on the “marginal” barrel of production both domestically and internationally to identify which plays and producers will suffer the most from falling oil prices. We have covered this topic over the last several weeks providing sneak peeks and snippets from analysis in our Upstream Outlook on the Bakken, the Eagle Ford, and the Permian. Today, we wanted to address an emerging play and what it might mean to the oil market. Last week, Illinois approved regulations to permitting use of modern hydraulic fracturing techniques. You are already probably asking yourself, why do I care about Illinois, I didn’t even know it produced oil and gas. Illinois used to be one of the largest oil producing basins in the US, but has mostly been ignored over the last 60 years. Production peaked during the Second World War at over 350 Mb/d, but today stands at a meager 27 Mb/d according to the latest statistics from the EIA. However, production is up 3 Mb/d over the last two years.

At higher oil prices, dedicated local operators have been able to squeeze new barrels from shallow conventional pools of production. With the changes in legislation, operators, like Strata-X, are now gunning for the source rock of all this historical production, the New Albany Shale. While we are not ready to bet the farm that this is the next Bakken or Eagle Ford, the first horizontal well result is interesting and could prove to be quite disruptive to the market if continued commercial viability is established over a large aerial extent. The first well from Strata-X produced over 300 b/d from an 1,800 foot lateral and cost less than $4 M to drill making it comparable to early results in the Niobrara. Furthermore, data from RigData indicates that Pioneer Oil Company (not to be confused with Pioneer Natural Resources) has also initiated a horizontal well in Clay County, IL.

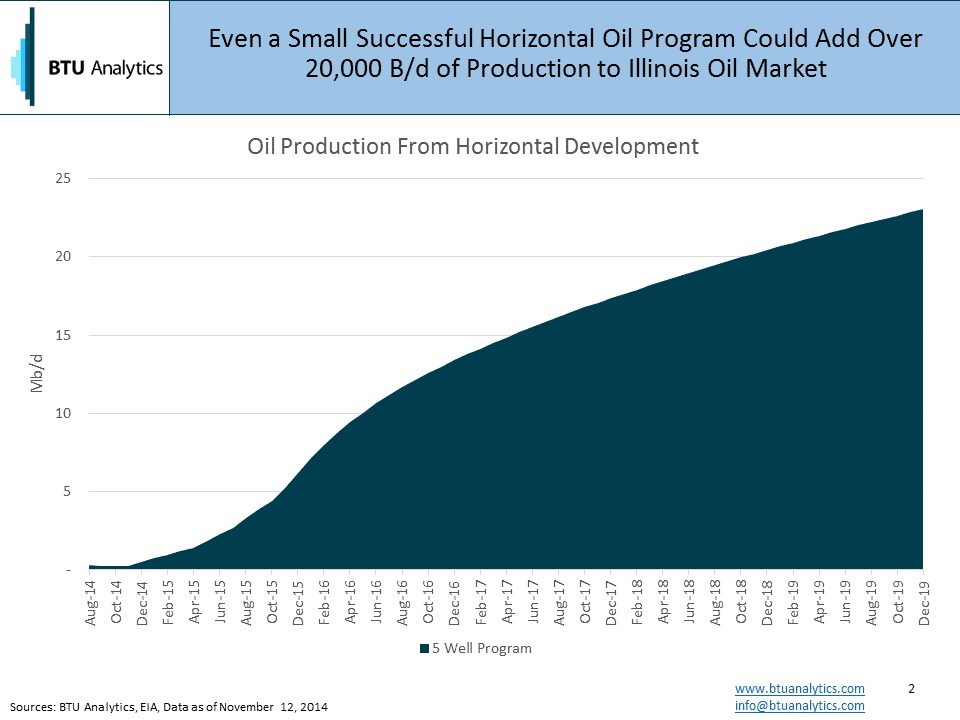

With a slew of new pipelines set to bring unconventional oil production through Illinois, could the New Albany shale prove disruptive to producer plans in other basins? Energy Transfer Partners (NYSE: ETP) and Phillips66 (NYSE: PSX) recently completed a successful open season for the Dakota Access Pipeline which is set to deliver up to 450 Mb/d of Bakken crude to Patoka, IL, (just one county over from the new developments) and then the ETCO pipeline will take that Bakken crude from Patoka to Nederland, TX. So how disruptive could the play be? In order to explore that, we put together a simple forecast increasing horizontal activity from 1 well per month to 5 wells per month by the end of 2015. Assuming those wells came on at 300 B/d, the play could surpass 20 Mb/d by the end of 2019.

While 20 Mb/d is certainly not enough to divert Bakken producers attention away from reaching new markets in Patoka and the Gulf, it does give those pipelines and refineries in the market another potential source of supply. Should the play take off to a greater extent though, producers should be wary of another potentially low cost play closer to market.