In the Spring of 2005, Offshore Gulf of Mexico (GOM) oil and gas production was at its pinnacle reaching record highs of over 5 MMbl/d of oil and over 10 Bcf/d of natural gas. However major events, such as the hurricanes of 2005 and unconventional production, were laying in wait and would trigger a long slow decline for the GOM to recent lows of 1.1 MMb/d in September 2011 for crude and just under 3.5 Bcf/d in spring 2015 for gas.

In this low priced hydrocarbon market everyone is still trying to figure out where the cards fall as the whole global hydrocarbon supply chain is getting reshuffled. OPEC produces away, while in North America certain well capitalized E&Ps with core shale play acreage positions are optimizing operations to compete for their share of the market. In this market, Offshore GOM oil has been getting a fair bit of attention but offshore gas hardly warrants a mention, which made BTU Analytics want to take a look.

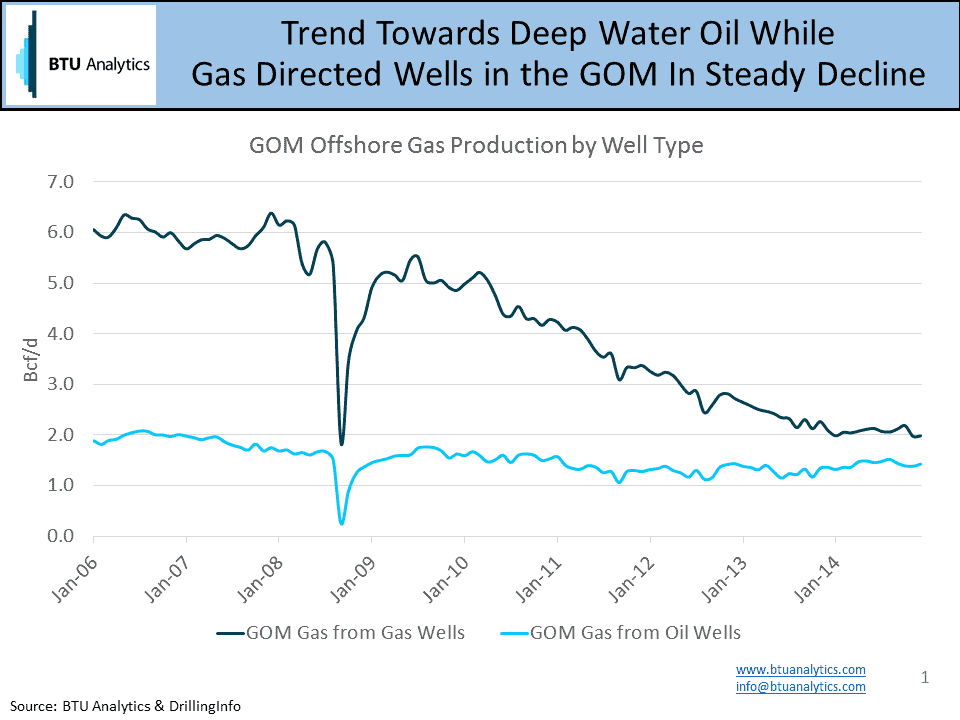

If we look at gas production data by well type, we can see the changing trends in offshore activity as shallow natural gas targeted activity has all but stopped while production from targeted oil wells has remained steady (see chart below).

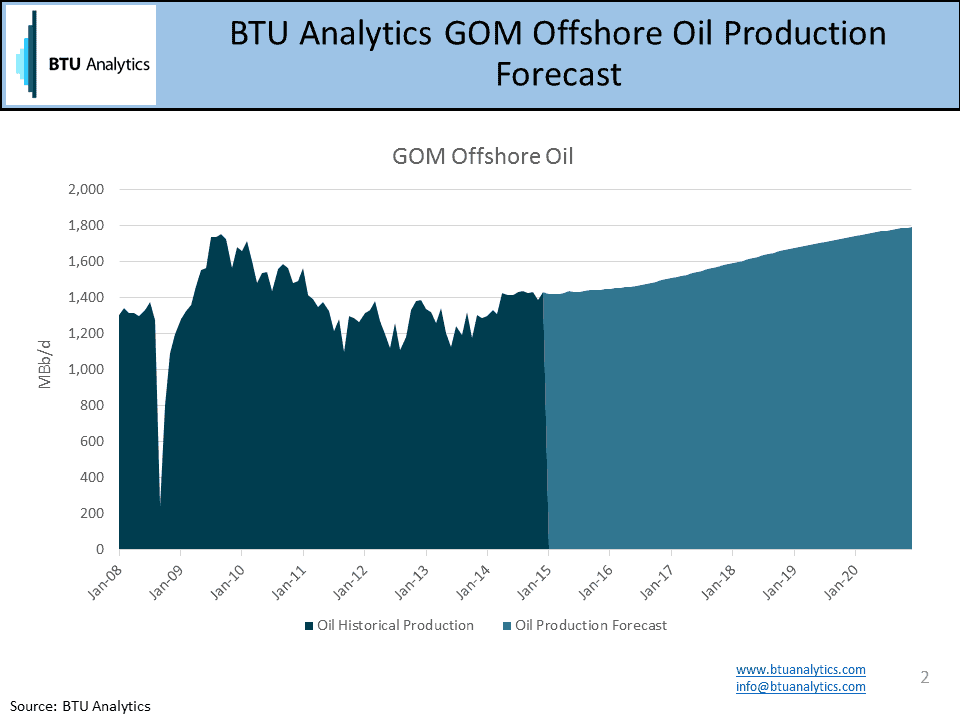

In early 2015, various consulting firms and the EIA released recent pieces highlighting the 13 deepwater offshore GOM oil projects that will come online in 2015-2016 that will push oil production higher. This follows solid 2014 GOM oil offshore results as oil focused activity has moved further into the deepwater with the Mississippi Canyon, Keathley Canyon and Walker Ridge blocks rising to top hot spots. And if we look at BTU Analytics’ oil forecast for the GOM, we see an incremental 200 MBb/d of growth through 2020 (see chart below).

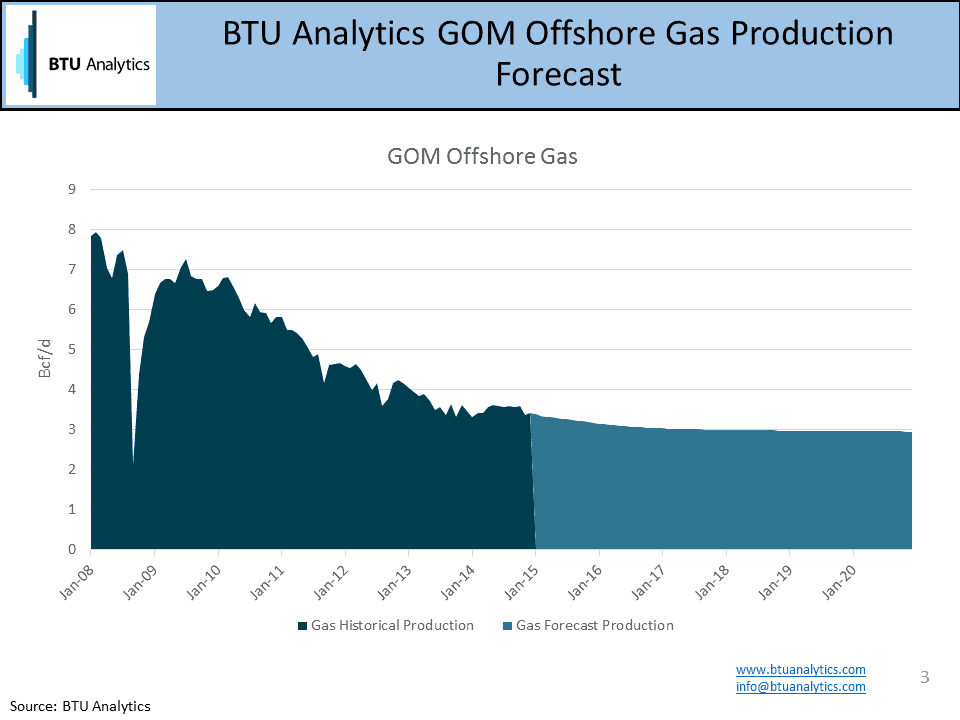

Meanwhile, BTU Analytics’ GOM natural gas forecast calls for gas production to decline by approximately another 0.5 Bcf/d through 2020 (see chart below). The question is, with rising GOM oil production, could GOM gas surprise to the upside? There is no shortage of offshore natural gas infrastructure considering gas declined from 10 Bcf/d down to 3.5 Bcf/d over the last 10 years. However, a large portion of this infrastructure was put in place to handle shallow gas wells. Enbridge claims it transports 35% of offshore gas and 45% of deepwater gas. In fact, Enbridge is scaling up its 100 MMcf/d Walker Ridge gas gathering system in 2014-2015 while DCP in 4Q 2014 put into service its 400 MMcf/d Keathley Canyon Connector.

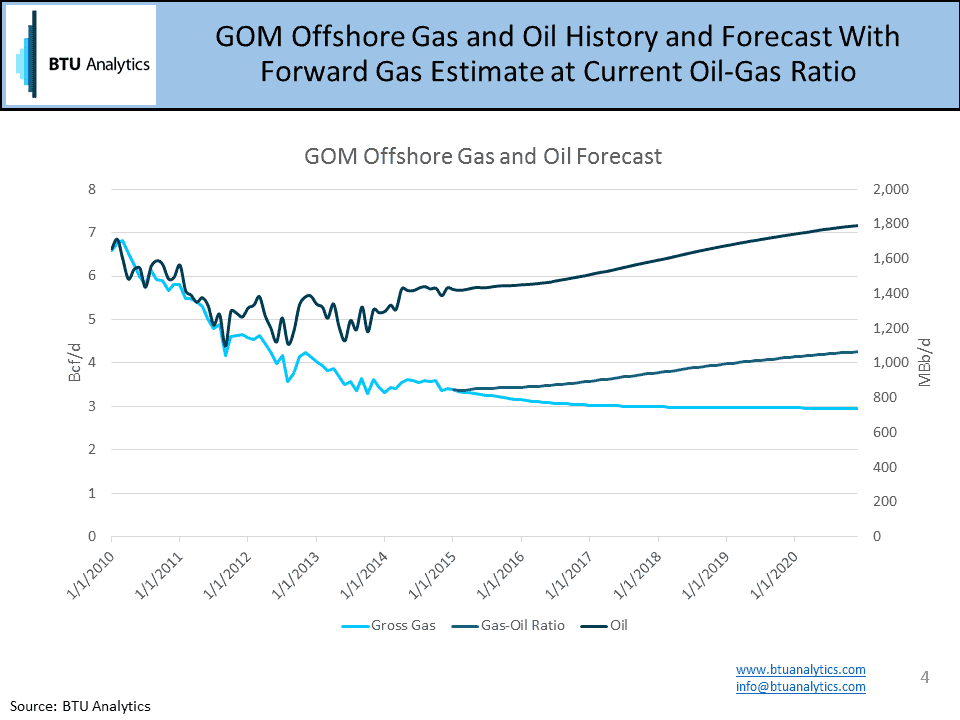

Back to the question – could offshore GOM gas surprise? A look at the GOM gas to oil ratio over time shows it has declined from 4 Mcf/Bb to about 2.5 Mcf/Bb currently. If in fact the majority of gas targeted offshore activity has been rung out of the system as the production data by well type above suggests, could that ratio flatten at current levels? Looking at recent results from Exxon’s Hadrian South prospect in the Tubular Bells field, located 230 miles offshore in Keathley Canyon, reveals a target of 300 MMcf/d and 3,000 b/d of liquids. This bucks the trend in the ratio. Back to the BTU foreceast, if we force gas production going forward to follow oil production gains based on the current 2.5 Mcf/Bb, offshore GOM gas production grows by about 1 Bcf/d by 2020 (see chart below). That would be a surprise and perhaps an unwelcome one for an over supplied gas market.

As the US natural gas market continues to look for relief valves in the form of power demand, industrial demand, LNG and Mexico exports, another 1 Bcf/d form the offshore would pressure that balance. BTU Analytics will continue to follow natural gas developments in the GOM in the Upstream Outlook with a keen eye to see if gas production surprises to the upside through 2020.