For the last several years, E&P’s have been boasting a paradigm shift towards Shale 3.0 that favors capital efficiency and returning cash to investors over rampant production growth. As with much of normal life though, that changed with the COVID-19 pandemic. The rapid impacts of COVID-19 and the resulting plummet in crude pricing led most operators to cut dividends, halt share repurchases, and, most importantly, raise debt. That increase in debt that many oil-focused E&Ps relied on to improve liquidity may take years to correct.

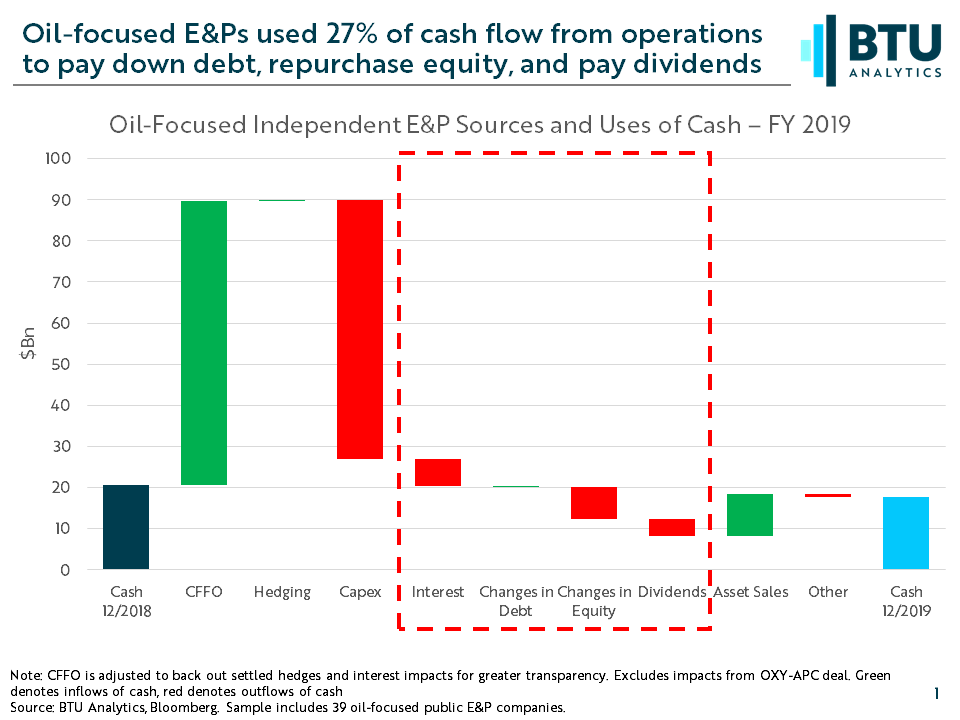

Throughout 2019, E&Ps highlighted their dedication to reducing capital spending on operations, and largely that played out. The chart below details the sources and uses of cash flow among 39 oil-focused E&Ps throughout 2019. Excluding Occidental due to its 2019 purchase of Anadarko, which led to a massive build in debt and equity to fund the acquisition, E&Ps largely held debt flat. Those E&Ps did, however, buyback nearly $7.7 billion in equity and pay out almost $4.3 billion in dividends.

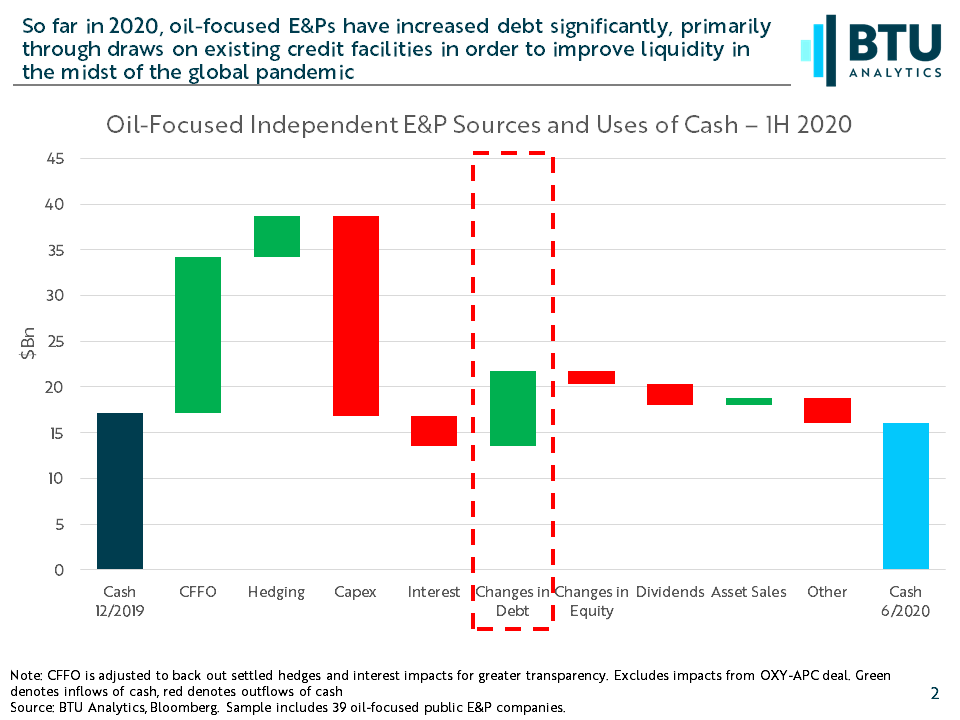

In 2020, largely out of necessity, that picture has fundamentally changed. The chart below similarly shows E&P sources and uses of cash through the first half of 2020. As the COVID-19 pandemic hit, many operators turned to their credit facilities to improve their liquidity, increasing debt by nearly $8.2 billion so far this year. Of the ten largest increases in debt by company through the first six months of the year (including APA, CLR, EOG, FANG, HES, LPI, NBL, OVV, WLL, WPX), half were driven by E&Ps drawing on their revolving credit facility.

These increases in debt are generally short-term in nature but could potentially lead to future increases in long-term debt. Apache recently announced a $1.25 billion notes offering on August 3rd, which will in part be used to pay down its revolving credit facility. To the extent that other E&Ps follow suit will depend on the willingness of capital markets to take on more E&P debt (a concept generally frowned upon over the last couple years). If E&Ps do decide to increase their long-term debt down the road to pay down a revolver, they could be set up for a longer road to recover, one with higher leverage and interest payments. This does, however, also depend heavily on the pace of any recovery in oil prices. To see what BTU Analytics forecasts the oil price recovery will look like over the next five years, request a sample of the Oil Market Outlook.