As the commodity crash began in 2014, we pointed out that producers would likely high-grade acreage (“High-Grading” — Every Producer’s Best Friend in 2015) to sustain production at lower drilling levels and attempt to focus on the rock and technology (High Grading Better Rock or Better Completions?) that would yield the most oil and natural gas. We also analyzed where producers would need to focus activity (The Limits of High Grading) in certain plays in order to achieve the best outcomes from drilling activity in 2015, and that not every producer would be equally positioned in its ability to improve the quality of the wells it drilled in 2015. Now that nearly a year has gone by and state production data is nearly complete for much of the country for the year 2015, we thought it was time to review if producer high-grading was successful.

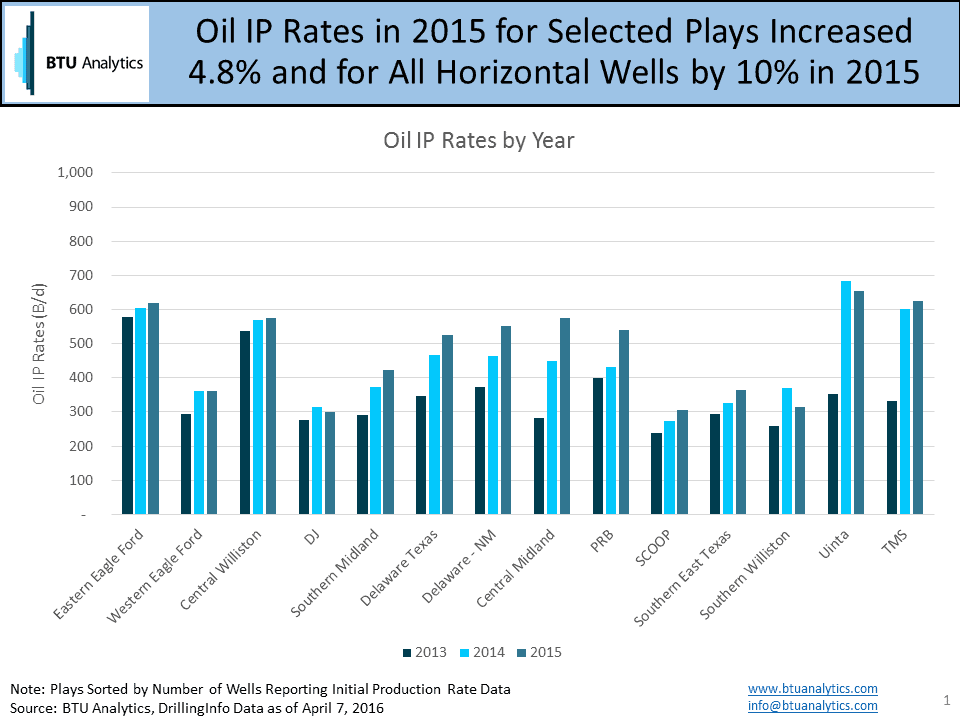

Reviewing the data indicates that nearly every major play saw some improvements in productivity in 2015 measured via initial production rates, but the rate of improvement varied drastically as some areas are quite mature in their development (Bakken and Eagle Ford). The Central Midland area in the Permian Basin has been a clear winner in growth in initial production rates with 677 horizontal wells reporting an average IP rate 27% higher than the 648 wells that were reported in 2014. The second biggest improvement came from the Powder River Basin (PRB) where results from Devon (DVN), EOG Resources (EOG), Chesapeake (CHK), and Encana (ECA) in the Turner and Parkman continue to improve.

While initial production rates are a good measure of short term productivity, it begs the question, are wells holding up over time or are producers juicing initial production rates at the expense of steeper declines?

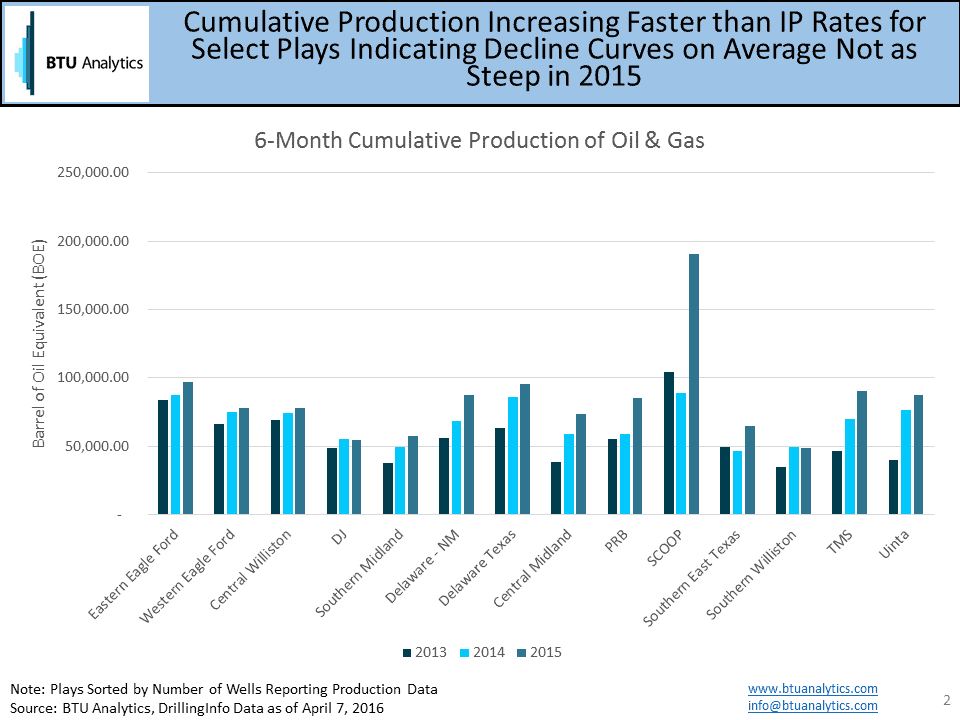

In order to analyze if well performance is holding up over time, we pulled the cumulative oil and gas production for wells with over 6 months of reported production data on barrel of oil equivalent (BOE) . While this data set is smaller than the sample of wells with initial production rates, it gives a strong indication that well performance improved in 2015 compared to 2014. All but two plays showed improvements in 2015, and most plays showed an improvement of 10% or more compared to 2014. Interestingly, the SCOOP region of Oklahoma has seen the greatest improvements as operators like Continential Resources (CLR) have focused on the gassier portions of the play (Big Wells In Oklahoma) which have increased well performance on a BOE basis substantially.

Overall, operator well performance in 2015 shows strong improvement in both initial production rates and cumulative production rates. Will 2016 continue to hold more of the same or has play productivity finally peaked as operators have already focused on the best rock with the best completion designs? Time will tell…

These, and other dynamics, are followed on a monthly basis in our Upstream Outlook publication.