Following a volatile 2022 that spurred a wave of rig additions and sped up service cost inflation across the oil and gas industry, producers are well on their way towards implementing 2023 activity plans. WTI pricing has fallen 40% from its June 8, 2022 peak, and Henry Hub has fallen nearly 80% from its August 22, 2022 peak. Even though oil pricing remains strong relative to average breakeven levels across the U.S., BTU Analytics forecasts activity to moderate from current levels as public producers remain committed to shareholder returns over production growth. However, as we discuss in today’s Energy Market Insight, the slowdown in activity so far this year is far from what is necessary to avoid further downward pressure on pricing, especially in natural gas markets.

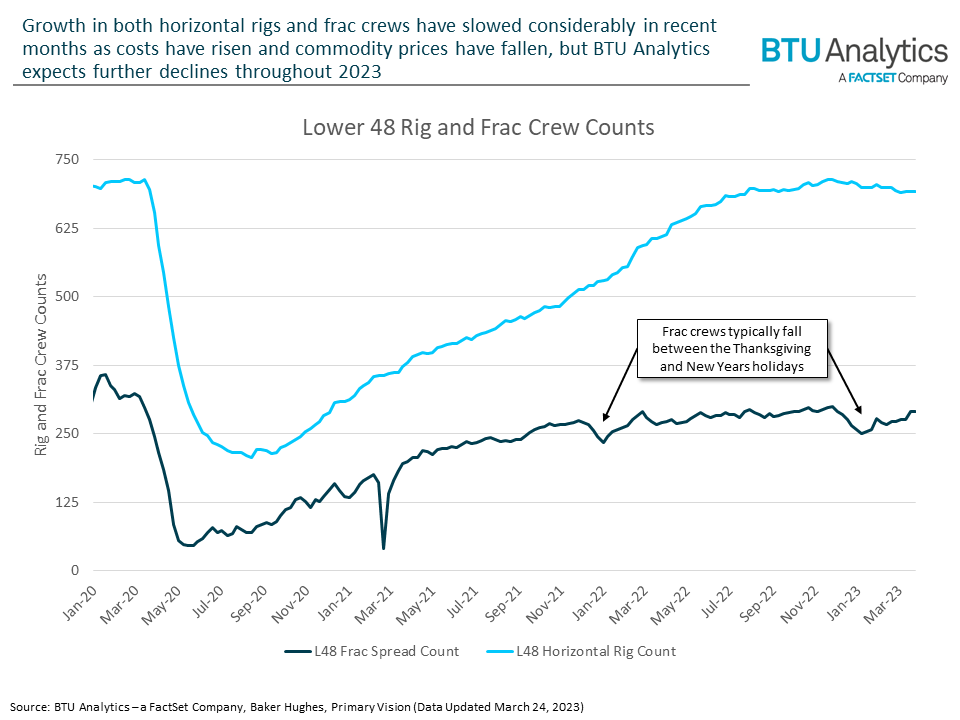

As shown in the chart below, growth in both drilling and completion activity has slowed in recent months following the recovery in rigs back to pre-pandemic levels. Oil-directed rig activity declined following recent WTI price weakness, driven by the Eastern Eagle Ford, SCOOP & STACK, and the Rockies, while Permian producers, especially publicly traded producers, continue to slowly add activity. In contrast, Henry Hub pricing has descended towards $2/MMBtu, but horizontal rig activity in natural gas-directed regions has yet to post a significant decline. This is especially prominent in regions like the Haynesville, where rigs have fallen by just two (or 2.5%) from the September 2022 peak of 79.

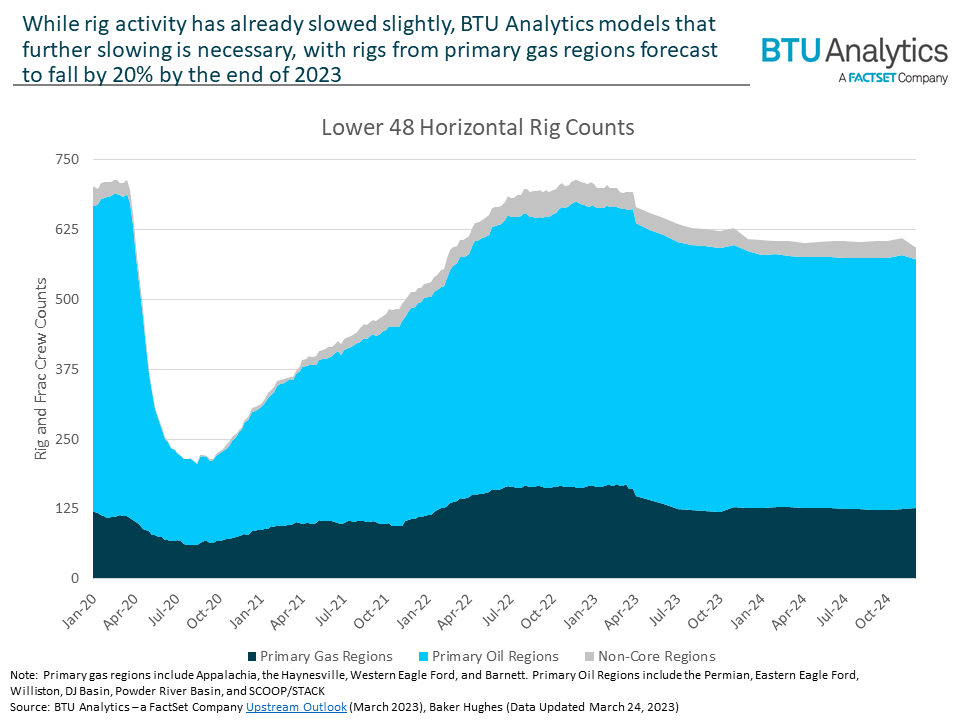

Going forward, BTU Analytics expects the decline in horizontal rig activity to accelerate, as shown in the chart below. As BTU Analytics expects Henry Hub pricing will fall below $2/MMBtu several times this summer, horizontal rigs in gas regions are expected to fall by more than 20% through the end of the year. Throughout 2022, rig growth outpaced completion crew growth as operators rebuilt drilled but uncompleted (DUC) well inventory following large draws from inventory in 2021. BTU Analytics models producers in oil-driven regions will moderate activity slightly throughout 2023, as DUCs have returned to more normal levels, while also focusing on shareholder returns in a higher cost environment.

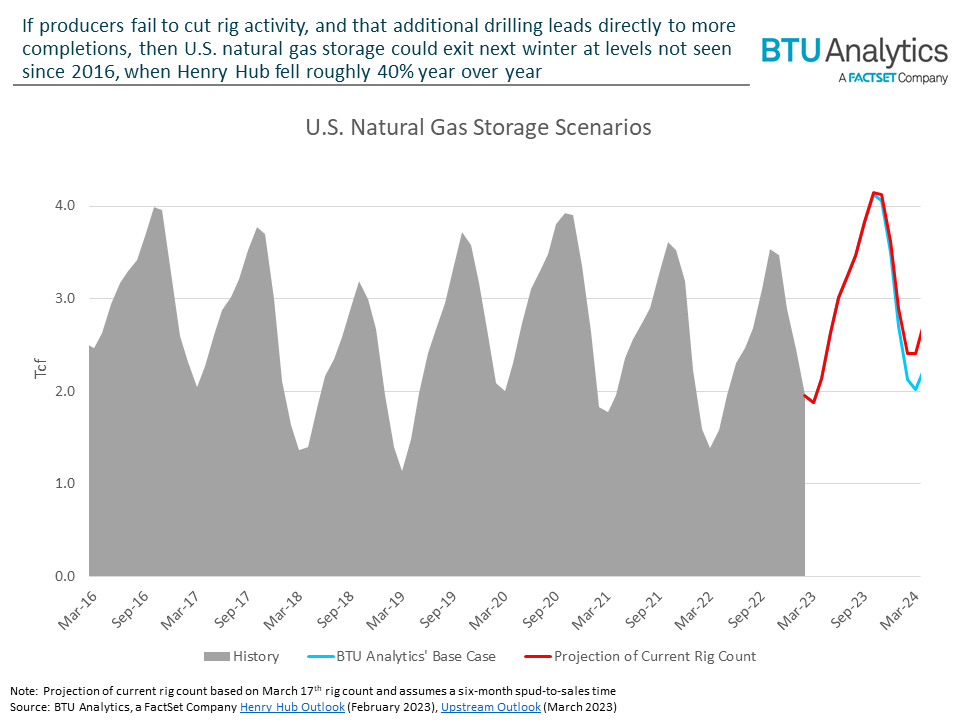

To date, though, operators have been slow to curtail horizontal rigs across the shale paths, even in the face of lower pricing. It is important to emphasize that horizontal rig activity is just one step in the upstream supply chain and many other factors could impact any production growth, such as availability of frac crews or labor and materials constraints. However, if producers fail to lay down rigs at a faster pace, and subsequently turn those wells online, then natural gas pricing risks even further downside than what BTU Analytics currently models. The chart below shows two potential outcomes for U.S. natural gas storage. Under BTU Analytics’ Base Case, storage levels are expected to be elevated throughout this year, but a slowdown in activity is expected to drive end-of-winter storage in March 2024 to roughly 2.0 Tcf. In the other case, where current drilling activity is held flat in perpetuity and those additional wells are completed in normal working order, natural gas storage would exit next winter (all else equal) near record seasonal highs, at 2.4 Tcf.

Those elevated levels of storage would set up Henry Hub to be far lower in 2024 than BTU Analytics’ current forecast that calls for an average $3.19/MMbtu for the year, already well below the current 2024 strip. However, as BTU Analytics has previously highlighted, natural gas production growth from oil-driven regions also has a major impact on Henry Hub pricing. So, without a decline in drilling and completion activity in both oil and gas-directed plays, the current near-term Henry Hub view may prove too optimistic. For more information around BTU Analytics production and pricing forecasts, request copies of our Upstream Outlook and Henry Hub Outlook.