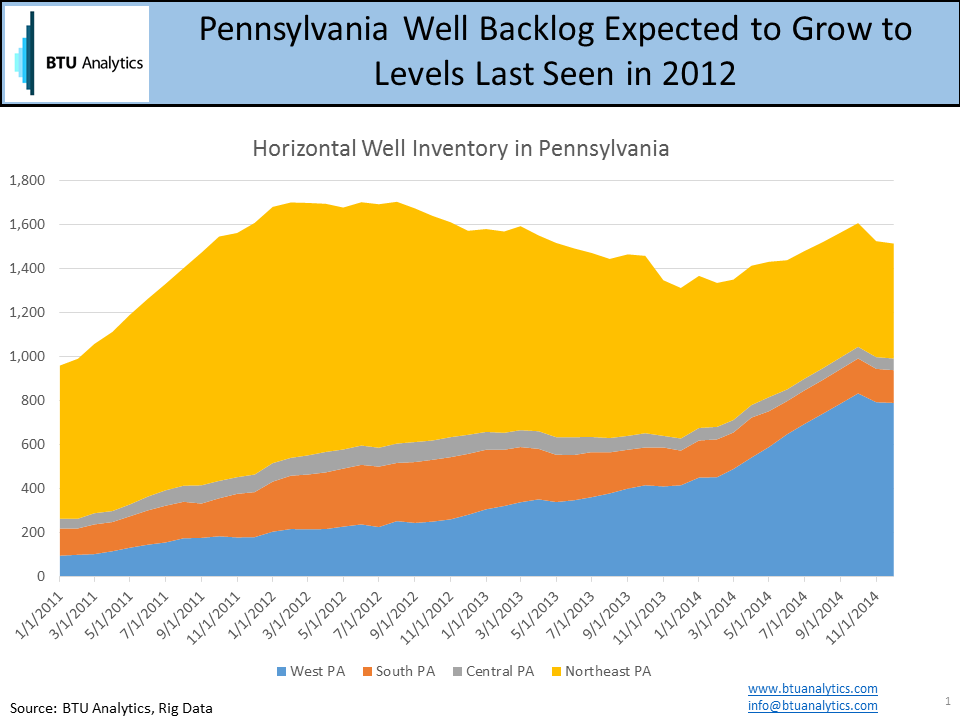

With over 9 Bcf/d of new pipeline projects proposed to evacuate natural gas production out of the Northeast, and new projects seemingly announced weekly, one might question where all of this will end. With Marcellus & Utica pushing Northeast production to 16 Bcf/d, can drilling inventory support prolonged production of over 25 Bcf/d? In the short term, BTU Analytics expects the incremental pipeline additions to fill rapidly due to the large backlog of drilled and completed wells awaiting infrastructure. Based on PA DEP, Genscape flow data, and BTU analysis the backlog of wells waiting to come to market is expected to grow to levels not seen since the early boom days in the Marcellus.

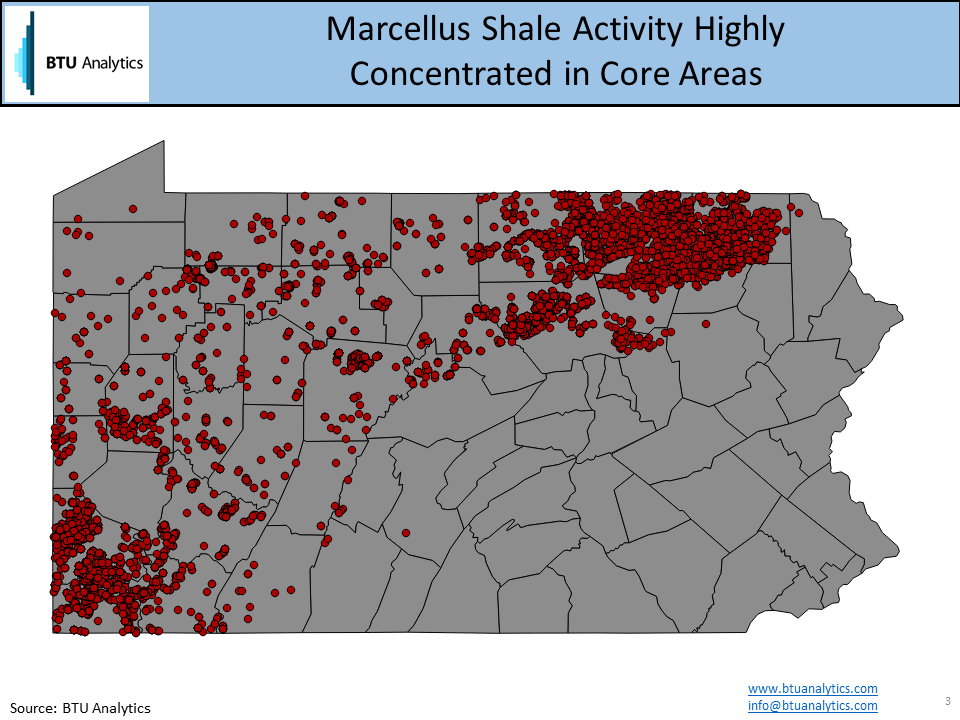

Horizontal Marcellus, and to a lesser extent Utica wells, have been drilled in over 40 counties in Pennsylvania alone as shown in the map below. Producers have already drilled over 6,000 wells since 2008 with almost 75% of those wells concentrated in Bradford, Washington, Susquehanna, Lycoming, & Tioga counties.

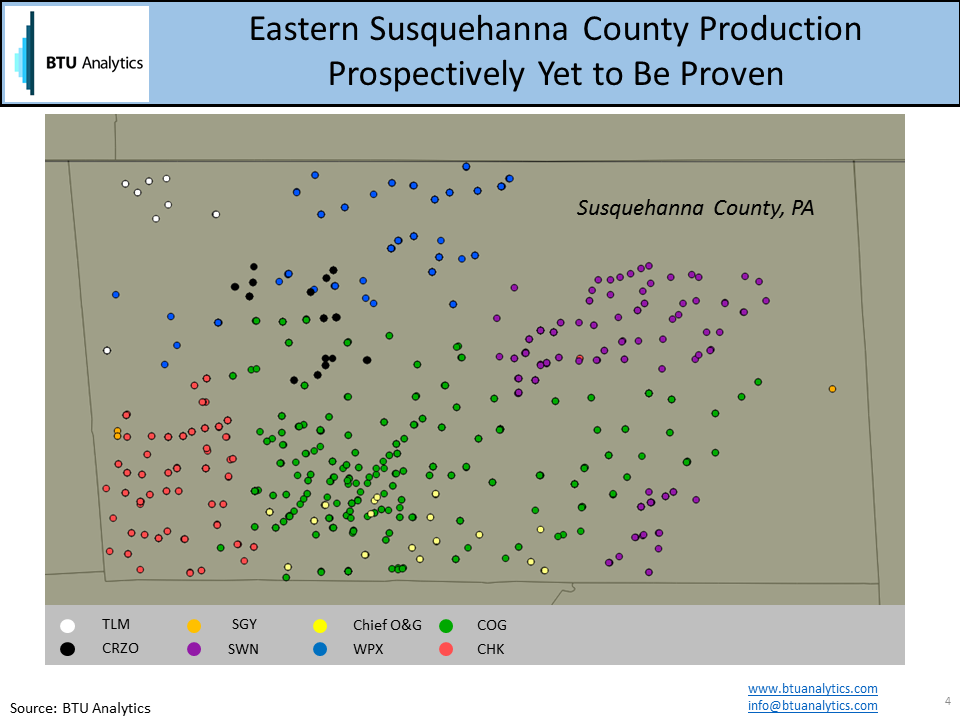

In order to quantify just how long production could be sustained in the Marcellus & Utica, BTU Analytics picked a case study of one of the most active counties in the basin, Susquehanna County, Pennsylvania. Susquehanna drilling is dominated by 6 producers as shown in the map below.

Drilling in the county shows relatively large gaps between well locations indicating producers aren’t yet in full development mode. Also, looking at the map above, BTU Analytics estimates that approximately 30% of the county has yet to be fully delineated, which could indicate lower productivity potential for those areas. Operators are currently developing their acreage on 80-120 acre spacing, with lateral lengths in the 6,500′ ballpark. Utilizing the data points above, we estimate that Susquehanna has approximately 3700 drilling locations with over 2900 of those yet to be drilled. Data from Datawright Rigdata indicates producers in the county are drilling on average 9 wells per month or 108 wells per year. At that pace producers have over 25+ years of drilling inventory in Susquehanna county alone.

But can current drilling and well backlog support additional infrastructure buildout? Stay tuned.