The WTI price has tumbled 30% to the high $60s since August, forcing the market to take a hard look at oil breakeven prices in the major oil producing plays across the US. We’ve discussed this in the past, using the Bakken as an example in our post “Bear Market to Test Bakken Breakevens“. While many E&P companies have yet to clarify what the drop in crude will mean to their 2015 spending plans, even the best positioned operators will have to reconsider their pace of activity as cash flow from existing production shrinks.

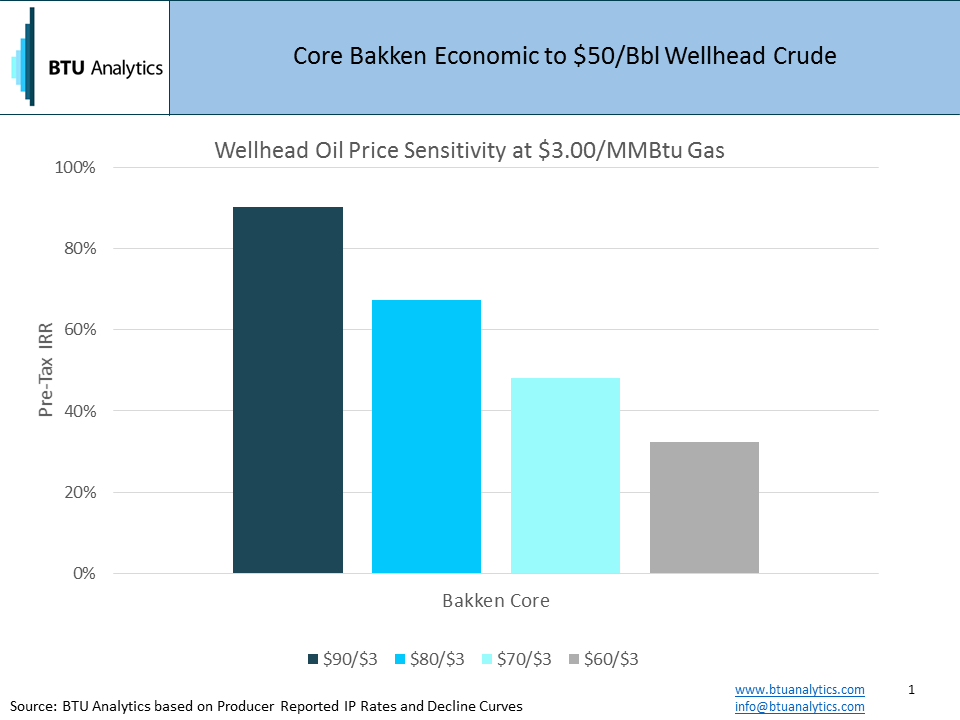

The chart below shows average wellhead economics for the Bakken core. While the chart shows that the Bakken will produce economic returns at a 10% cost of capital at $50/bbl, lower oil prices mean that an individual well will turn cash flow positive much later in its life. (Note that these are wellhead price assumptions that do not factor in the transportation cost to market.)

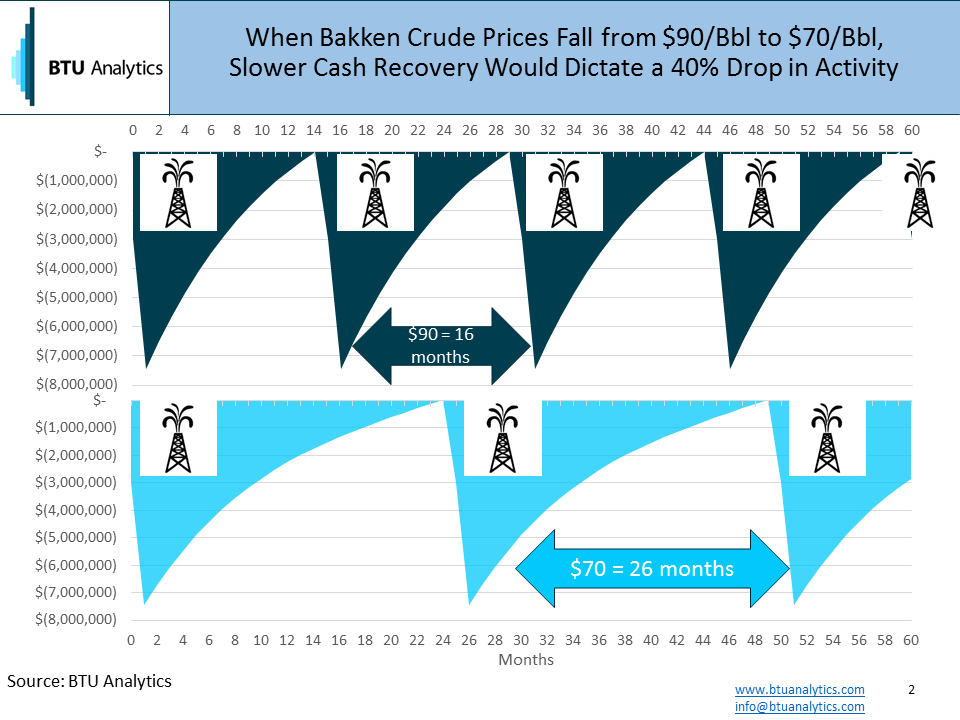

The next chart shows the number of months that it takes for a well to turn cash flow positive at various wellhead oil prices. At $90/bbl crude oil and $4/Mcf natural gas, the Bakken well turns cash flow positive in 16 months. When the wellhead crude price falls to $70/bbl, the Bakken turns cash flow positive in 26 months, a slowdown of approximately 60%.

Why does this matter? Because the primary source of capital for new drilling is cash flow from operations. And the most difficult time to obtain capital from banks and the capital markets is when the market becomes anxious about commodity prices.

So how does the slowdown in cash recovery affect the pace of drilling? The graphic above illustrates the effect using a Bakken well. Assuming an operator needs to recover capital from the first well before drilling the next well, again with 10% assumed cost of capital, the operator can drill 4.0 Bakken wells in five years at $90/Bbl crude. At $70/bbl crude that number falls to 2.4 wells, a reduction of 40%. Hedges, leverage, and the willingness of the capital markets to support production growth in a weaker oil price environment will impact the equation for individual companies, but over time, slower return of capital will win out.

This analysis first appeared as part of a larger feature in BTU Analytics’ Upstream Outlook Report published in November.