Recent announcements from Tuscaloosa Marine Shale (TMS) operators appear to indicate that the play has turned a corner. Prior well results have been inconsistent, with reports of well bore obstructions and wells plugging during flowback. Exploring the TMS isn’t a game for producers on a tight budget either, with the deep wells setting producers back approximately $13 million to $15 million each (compared to $9 million in the Bakken and $6 million in the Eagle Ford, on average), the cost of failure is high.

Earlier this week Goodrich Petroleum (NYSE: GDP) announced a 24-hour average test rate for the C.H. Lewis 30-19H-1 well in Amite County, Mississippi of 1,450 BOE/day, of which 1,387 barrels were oil (96%). Halcon Resources (NYSE: HK) announced a 24-hour average initial production rate of 1,391 BOE/d, of which 1,208 barrels were oil (87%). 24-hour test rates are released to the market for many reasons, the best intention being to indicate to the market the potential of the well when midstream infrastructure isn’t in place to actually flow that well to sales immediately. But 24 hour test rates can also be misleading, as the indicative production potential for a test rate is subject to a number of factors (reservoir pressure, choke, whether the test was actually 24 hours of continuous flow, or the best one hour volume multiplied by 24, etc.).

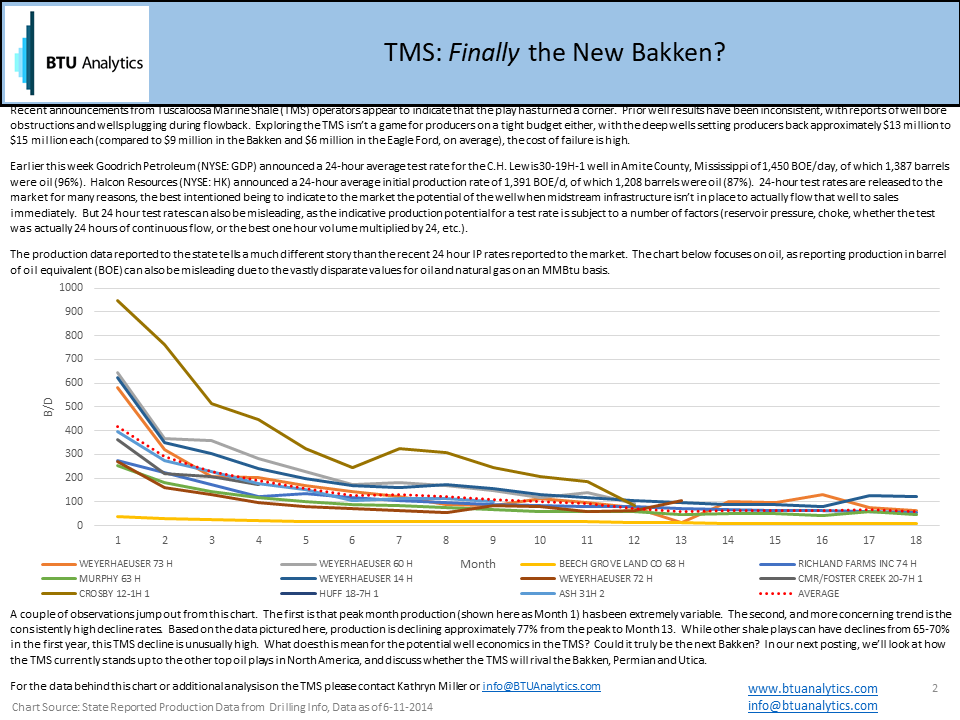

The production data reported to the state tells a much different story than the recent 24 hour IP rates reported to the market. The chart below focuses on oil, as reporting production in barrel of oil equivalent (BOE) can also be misleading due to the vastly disparate values for oil and natural gas on an MMBtu basis.

Source: Drilling Info

A couple of observations jump out from this chart. The first is that peak month production (shown here as Month 1) has been extremely variable. The second, and more concerning trend is the consistently high decline rates. Based on the data pictured here, production is declining approximately 77% from the peak to Month 13. While other shale plays can have declined from 65-70% in the first year, this TMS decline is unusually high. What does this mean for the potential well economics in the TMS? Could it truly be the next Bakken? In our next posting, we’ll look at how the TMS currently stands up to the other top oil plays in North America, and discuss whether the TMS will rival the other oil plays.

Tuscaloosa Marine Shale: Finally the Next Bakken? Part II

So what will it take for the economics in the TMS to rival the major US producing basins such as the Bakken and Eagle Ford? In a $100+/bbl WTI world, the market is a big tent, welcoming even marginal plays to grow. However, given the oversupply scenarios quickly approaching as light oil grows faster than new demand to take it, domestic oil prices are expected to fall dramatically unless changes are made to the crude oil export ban.

So if producers can produce repeatable results in the TMS that match the recent 24 hour rates, and lower well costs through development drilling, can the TMS flourish in an $80/bbl oil price environment? The chart below shows well economics under various oil price scenarios assuming both the current average well performance and well costs as well as an optimistic case ($10 MM well costs and IP rates of 1400 Boe/d).

The optimistic case (590 Mboe EUR) competes well with the Bakken and Eagle Ford. However, current average results (380 Mboe EUR) are a long way from that case.