While most of the industry’s focus falls on the major shale plays, other independent E&P producers are continuing to drill in areas that many haven’t heard of or thought about in quite some time. Today we’ll zero in on activity in the Rockies, analyzing the latest results from wells in areas outside the radar including the North Park Basin.

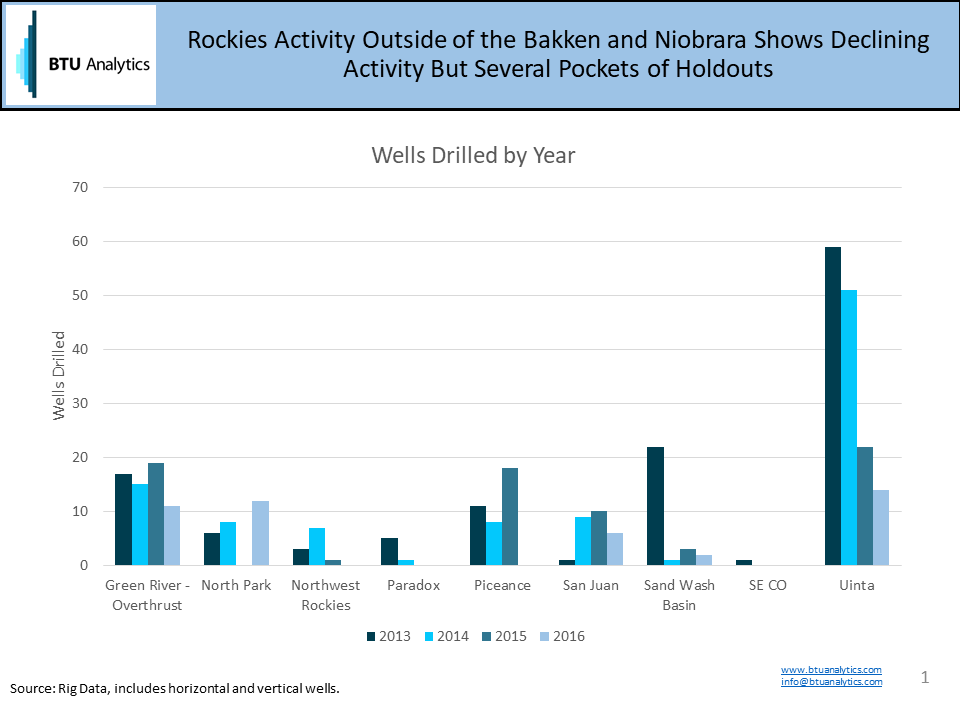

The slide below shows the number of wells drilled by year in Rockies regions outside the Bakken and DJ/PRB regions.

Uinta, Green River – Overthrust and Piceance have held most of the activity in these areas over the past four years. But none of the activity in those regions is growing. Interestingly, North Park hasn’t seen a significant number of wells, and zero drilled in 2015, but the number shows an upward trend, particularly in 2016 activity.

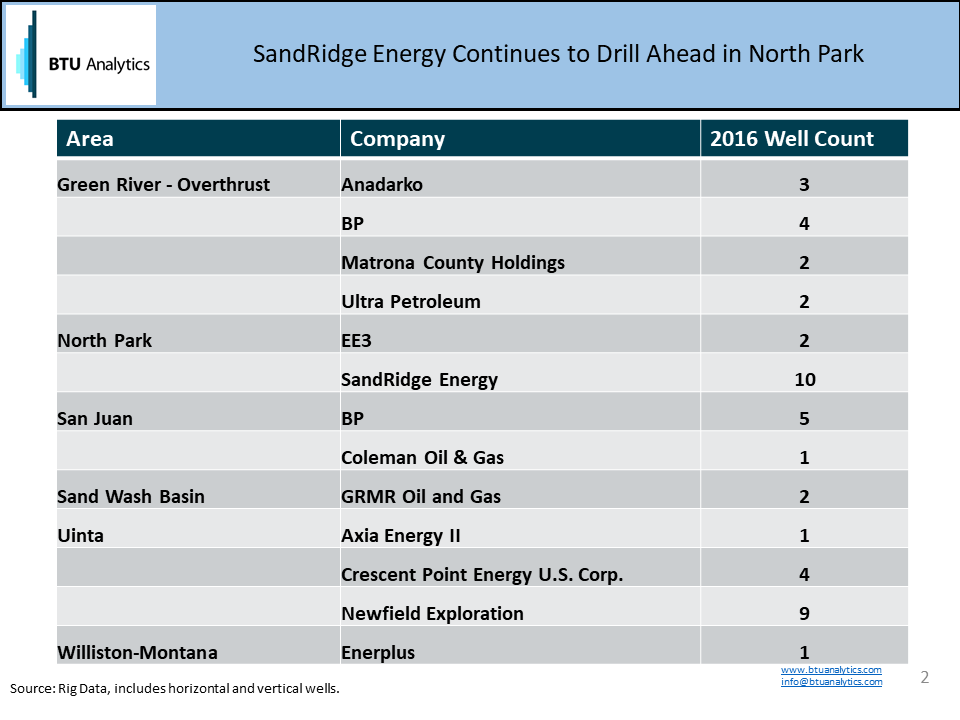

Digging further into the 2016 data, SandRidge Energy is responsible for the majority of activity.

SandRidge announced an acquisition in the North Park Basin back in November of 2015. Just six months later, SandRidge filed for Chapter 11. On the 9th of September, the company announced that the U.S. Bankruptcy Court for the Southern District of Texas had confirmed the company’s plan of reorganization, allowing SandRidge to target emergence from bankruptcy protection within the next 30 days. Do the results from North Park deserve a look from investors as SandRidge emerges?

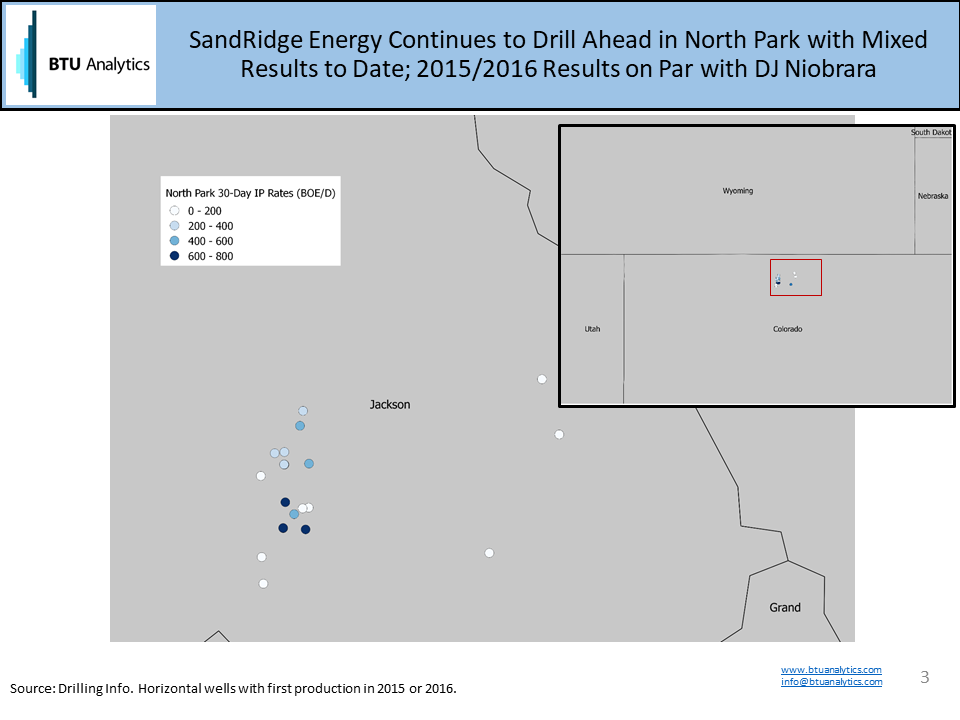

The map above shows IP rates for SandRidge operated wells (both wells drilled by SandRidge and acquired in the acquisition.) Average 30-day IP rates for wells with first production in 2015 and 2016 (6 wells) is 258 b/d. This is actually comparable to historical oil IP rates of 295 and 259 b/d across the combined DJ/PRB regions in 2015 and 2016, respectively. SandRidge noted back in 2015 in a slide focused on returns in the North Park Niobrara, that D&C costs for those wells were $3.6MM. Without having more operators in the area, that figure is difficult to verify (and recall how we highlighted the importance of verification in our previous commentary), however, it does seem to be in the same ballpark as some of the less expensive wells in the DJ Basin. ($3.5MM to $5.0MM)

Is the North Park Niobrara the next great play? Probably not, but it looks like an asset that could provide a fresh start for SandRidge as the company begins its next phase.

For data to benchmark company IP rates, EURs, well costs and remaining inventory calculations, request samples of BTU Analytics’ Upstream Outlook and E&P Positioning Report data files.