It’s clear that 2020 has brought many changes, both across the world and in the oil and gas industry, and operators are taking note. Two weeks ago, BP outlined its new vision in the organization’s annual BP Energy Outlook. The outlook envisions a global transition away from hydrocarbon-based fuels and commits the company to a 40% reduction in oil and gas production by 2030. Conversely, Exxon Mobil recently affirmed, “[oil] demand will not only recover but continue to grow to satisfy higher energy needs of developing countries.” Today’s energy market insight will review how plans for two of the majors, ExxonMobil and Chevron, have changed for US shale development in response to current oil market dynamics.

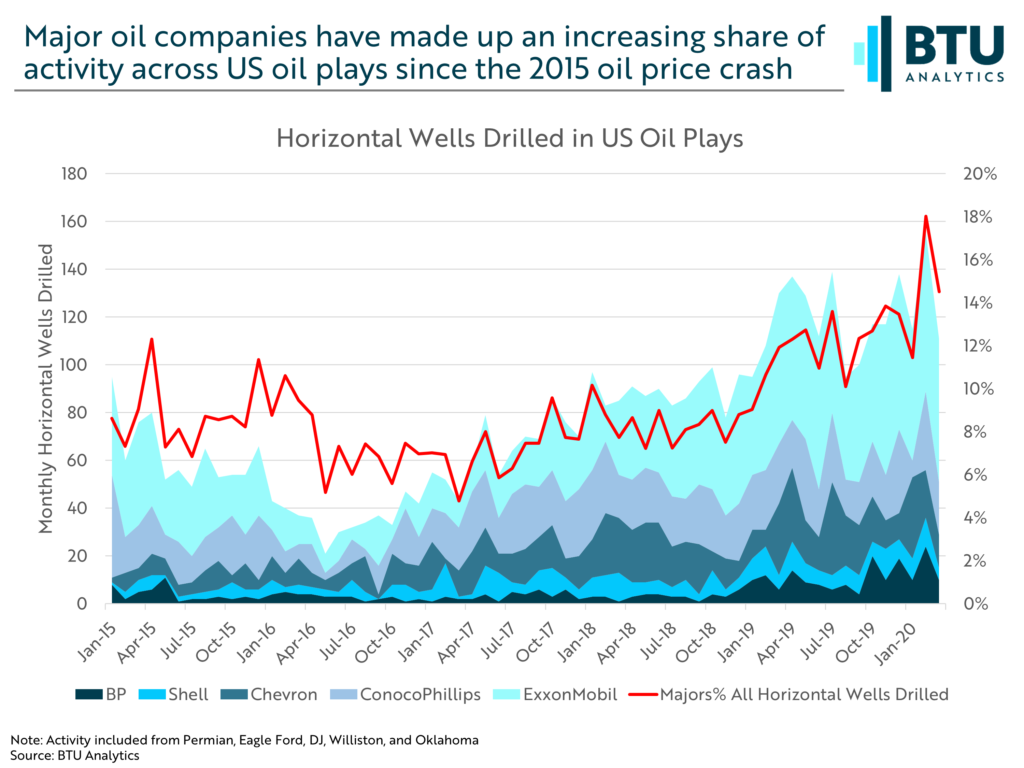

Corporate views on long-term demand dictate company posturing, strategy, and a resulting production response, but the impact on the US upstream outlook must be tempered by the level of exposure each major has to various US shale plays. After the oil price crash of 2015, oil majors have made up an increasing share of US Lower 48 activity. As shown in the chart below, in oil-focused regions, the proportion of horizontal wells drilled by the majors has nearly doubled, from an average of 7.4% in 2016 to 14.3% in the first quarter of 2020, and their share of production per state-reported data has risen from 10.5% to 11.5%. These increases aren’t uniform across basins or operators, however, and their distribution has significant consequences on the resulting production picture.

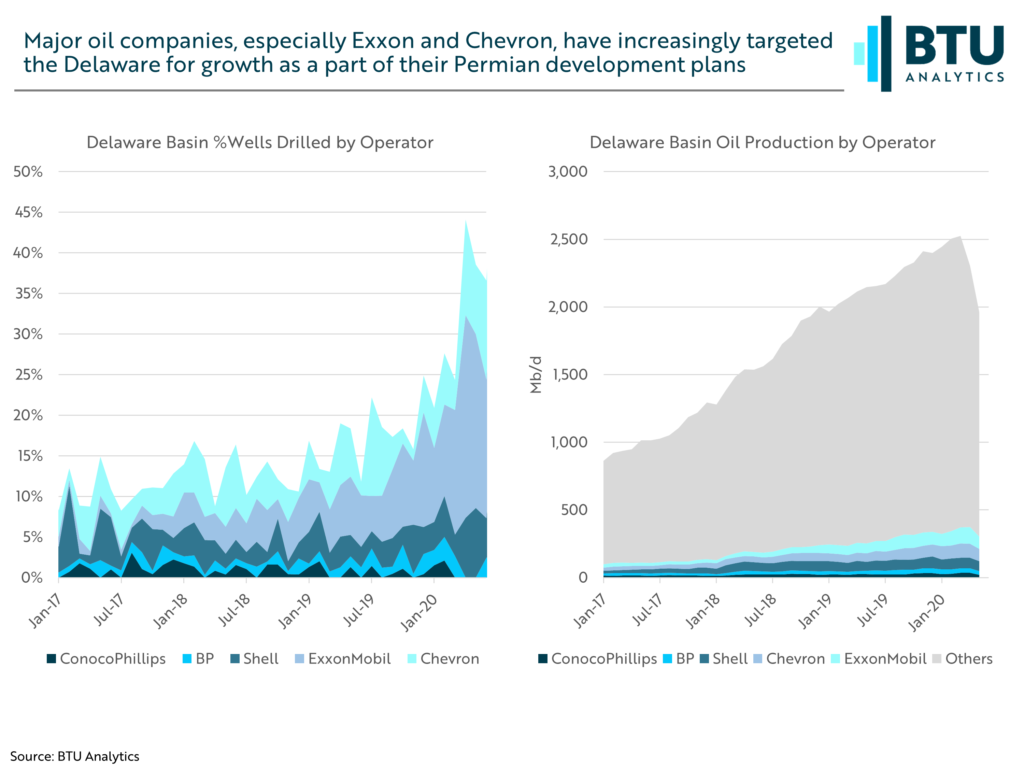

The Delaware Basin has seen a marked influx of activity by the majors since 2017. Their share of horizontal wells drilled in the basin increased from 10.7% in 2017 to 24.2% in 1Q 2020, driven primarily by investments by Exxon and Chevron, which are responsible for nearly 86% of this increase in activity. These two majors’ state-reported, company-operated production has increased from 53 Mb/d to 205 Mb/d over the same period. In addition to increasing their share through higher activity levels, M&A activity is heating up and leading consolidation. Chevron is currently working to acquire Noble Energy, who accounted for 54 Mb/d of Delaware oil production in 1Q 2020 and 2.2% of activity.

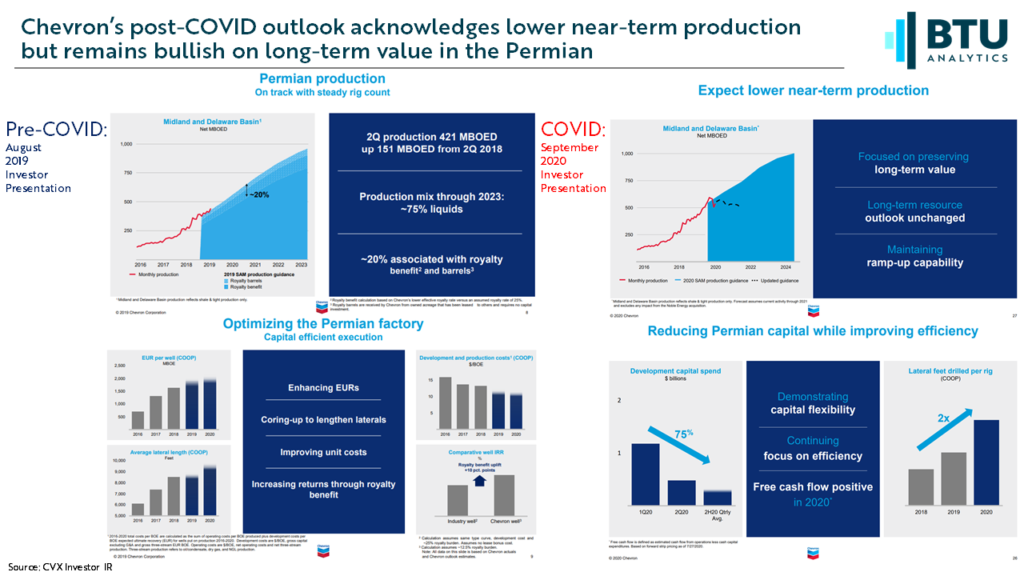

Prior to the onset of the pandemic, the Permian was central to Chevron’s plans to steadily grow oil volumes in 2020 and beyond, with a forecasted compound annual growth rate between 3 and 4%. Chevron’s unconventional Permian production grew steadily through 2019 and into early 2020, peaking at 580 Mboe/d net in 1Q 2020 on their way to a company-projected 900 Mb/d by late 2023.

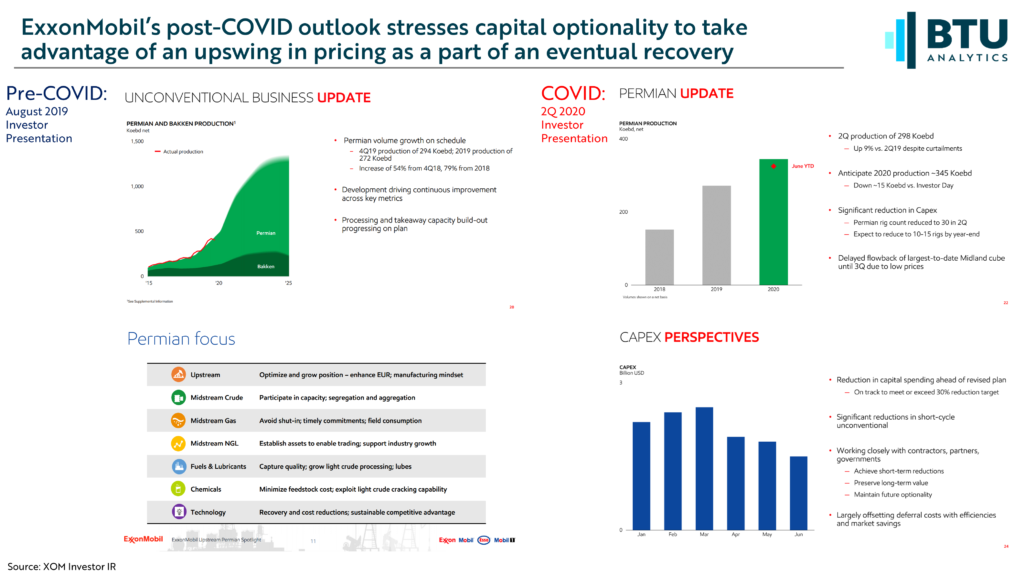

ExxonMobil also built a significant and growing presence in the Permian prior to the pandemic. The company’s unconventional oil volumes in the Permian, which reached 294 Mb/d net in 4Q 2019, were expected by the company to rapidly scale to over 1,000 Mb/d by 2025 by capitalizing on their contiguous acreage position, modular/manufacturing approach to development, and vertically integrated wellsite services.

In response to COVID-19 disruption in 2Q 2020, both Exxon and Chevron quickly adjusted their near-term strategy, curtailing production in the basin while rapidly scaling down drilling and completions activity. Curtailed volumes have moderated into 2H 2020, however, their near-term outlook in the basin still appears subdued. At current activity levels, Chevron anticipates Permian production to decline between 6% and 7% in 2021. Exxon reduced rig counts to 30 in 2Q 2020, and, amid ongoing pricing weakness, expects to further reduce counts to 10-15 rigs by 2020 exit.

Despite the current headwinds across the basin, both Chevron’s and Exxon’s long-term Permian outlook remains unchanged. In Exxon’s 2Q 2020 conference call, the company explains its current balancing act of pacing near-term investment while providing optionality for additional capital investment to capture an upswing in pricing when markets recover. Instead of steady and consistently increasing Permian growth, the near-term focus has shifted to capital flexibility – a ramp down in volumes and activity while maintaining the ability to quickly ramp up if pricing improves.

Even with this new paradigm of optionality and tepid near-term growth in the Permian, the basin is still set to play an integral role in US energy production now and in the future. Amid an uncertain recovery from COVID-19, will the Permian remain the US’ most steadfast swing producer? For BTU Analytics’ full production outlook on the Permian as well as other US shale basins, request a sample of our Upstream Outlook Report.