Higher natural gas prices domestically could threaten the feasibility of growing Gulf Coast LNG exports, which has led some exporters to secure additional nearby production and undrilled acreage to de-risk upcoming projects. Tellurian’s Driftwood LNG project was recently announced to begin construction in April 2022 by Executive Chairman Charif Souki, and the company expects to supply Driftwood with Haynesville production. While Tellurian’s production unit in the Haynesville has been growing, it will likely need to grow much larger to provide the ‘physical hedge’ that CEO Octávio Simões has boasted for its integrated export approach. But after a year of heavy consolidation in the Haynesville, what assets remain? What was once predominantly a private E&P company stronghold has quickly inverted due to M&A activity from the likes of Chesapeake, Southwestern Energy, and Comstock. BTU Analytics will examine which opportunities remain for further E&P consolidation or for LNG facilities to secure additional upstream production capacity in today’s Energy Market Insight.

The Driftwood LNG project’s updated construction timeline came as a surprise to some given its lack of traditional FID announcement. Instead, Souki confirmed construction set to start later this year ahead of fully secured financing during one of his “Two minutes with Charif Souki” webcasts (linked above). Phase I of the facility will require roughly 1.5 Bcf/d in feedgas when fully operational in 2026/2027. Tellurian intends to grow their net production of natural gas from a 2021 year-end exit production rate of 70 MMcf/d to 220 MMcf/d at year end 2022 according to their latest corporate presentation from November 30, 2021. The growth in 2022 will be accomplished with a single rig drilling program. However, reaching 1.5 Bcf/d of production when the facility comes online likely won’t be accomplished through the drill bit alone on its current acreage. This could be done through expanding its non-operated production interests or through other means, such as mineral ownership or partnerships with other producers. However, let’s explore the idea of a hypothetical outright E&P company acquisition to cater to the physical hedge strategy.

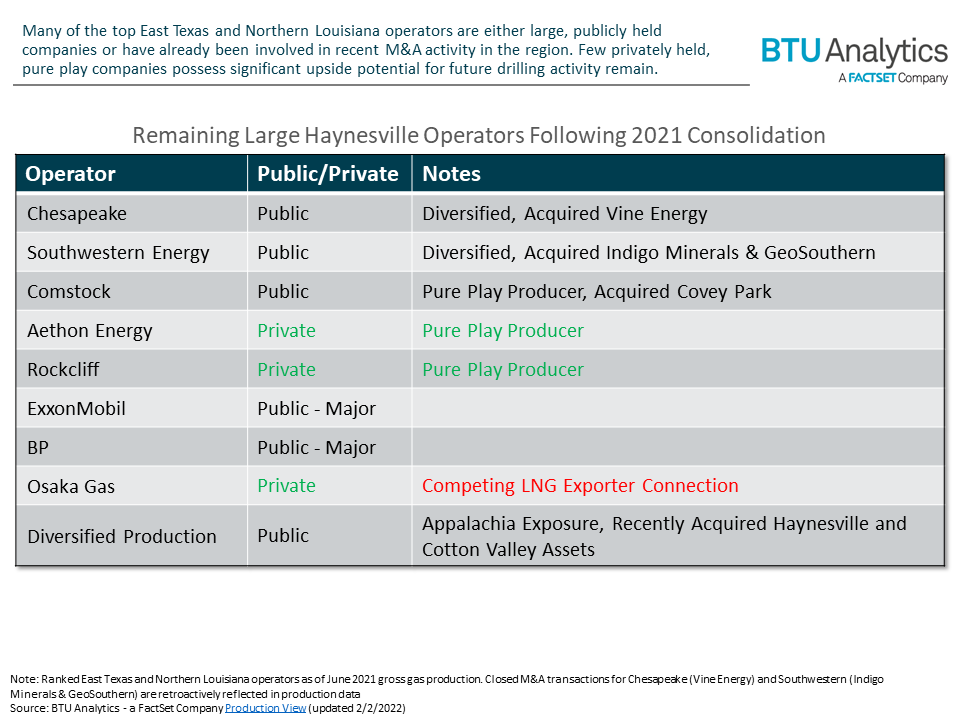

The list of top operators, shown above, highlights the asset ownership changes taking place in the Haynesville in recent months. Chesapeake and Southwestern Energy’s acquisitions of Vine Energy and Indigo Minerals, respectively, scooped up two of the Haynesville producers of considerable size. Additionally, Southwestern just completed acquiring GeoSouthern’s Haynesville assets, removing another private operator from the production mix. Finally, Diversified Energy Company acquired assets in the Haynesville and Cotton Valley from Tanos Energy Holdings III. Of the top operators, that leaves Aethon Energy, Rockcliff, and Osaka Gas as privately held E&P companies of scale. Among these operators, it is unlikely that Osaka Gas could be an acquisition target as it acquired Sabine Oil & Gas’s assets to augment its equity stake in the Freeport LNG export facility.

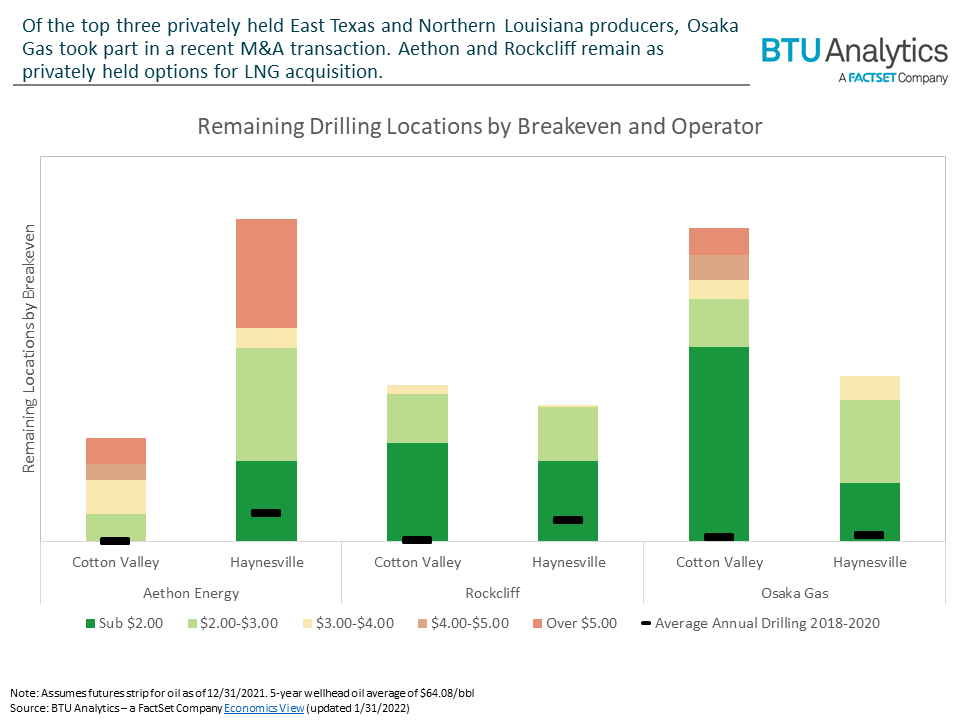

BTU Analytics’ Economics View estimates the number of remaining locations in acreage that has been drilled from 2013-present, providing indicative estimates of potential remaining inventory that has been de-risked by recent drilling. Using this indicative methodology to leverage recently drilled acreage, Aethon appears to have a longer inventory runway than Rockcliff, particularly in the Haynesville. Rockcliff, however, appears to have more than double the number of estimated sub $2 breakeven remaining locations when also incorporating the Cotton Valley horizon remaining locations. Cotton Valley economics are typically more sensitive to natural gas liquids pricing than Haynesville wells, adding complexity to the ponderance of any further M&A activity.

The Haynesville, once a basin predominantly driven by privately held operators, has reached an inflection point in ownership due to several acquisitions by publicly held companies. As companies seek to de-risk gas production by acquiring assets close to the Gulf Coast, few E&P companies remain as potential targets for outright acquisitions by LNG exporters, like Tellurian. Request a demo of BTU View to get additional information about how BTU Analytics can streamline E&P company research with comprehensive breakeven and remaining inventory location analysis.