The recent wave of mergers and acquisitions (M&A) allowed many producers to add contiguous acreage and reduce go-forward costs through newfound synergies. However, the surviving company will rarely find every acquired acre to be a perfect fit for their long-term strategy. Additionally, concentration of acreage has given operators a vast runway of drillable locations that in a capital-restrained environment may not be developed in the next five to ten years by the current owner of the acreage. In today’s Energy Market Insight, BTU Analytics will review remaining Permian Basin horizontal drilling locations by operator to identify potential for acreage to become a stranded asset if drilling doesn’t accelerate.

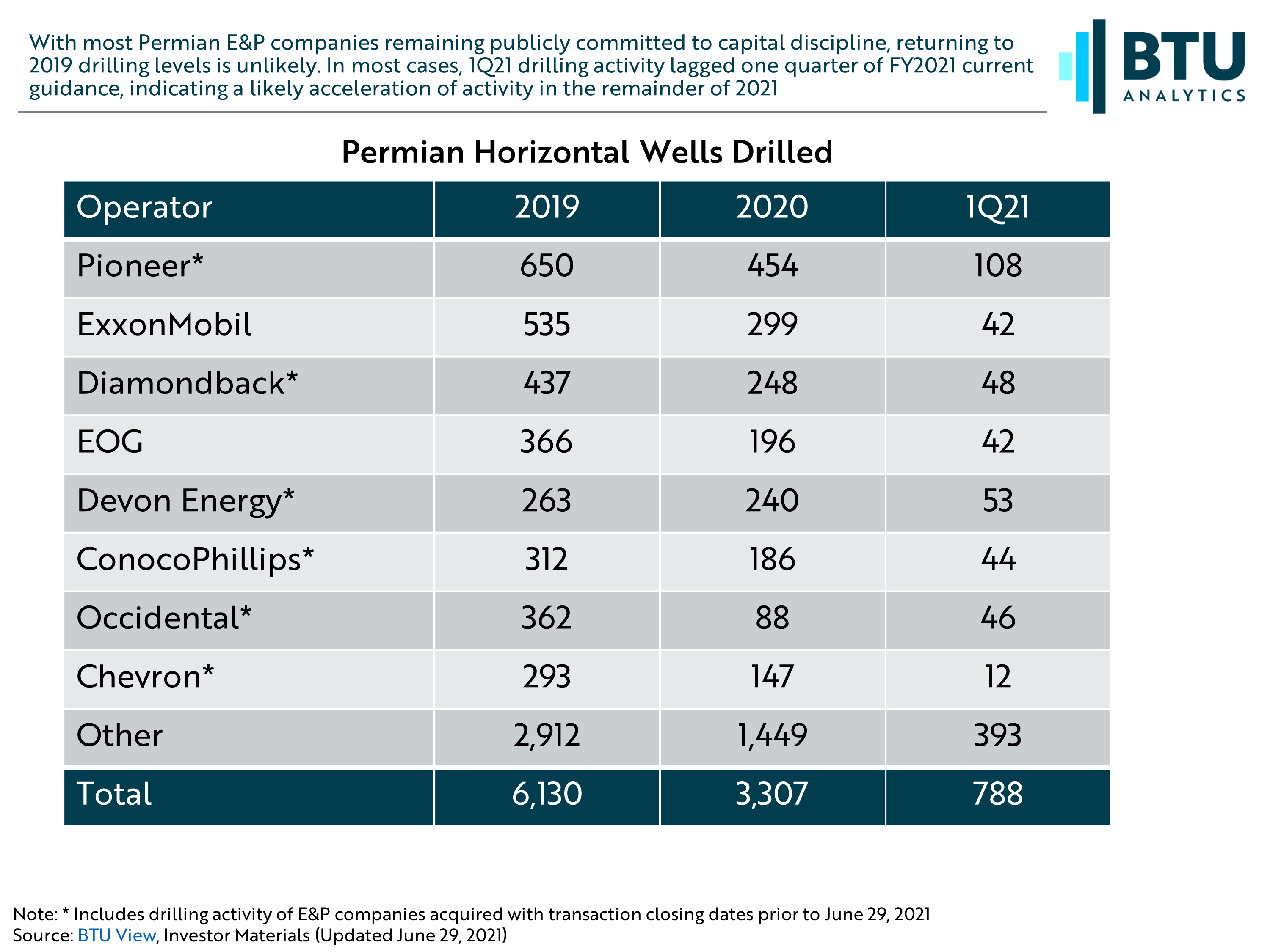

The table below shows the number of horizontal wells drilled for the top eight operators in the Permian based on number of wells drilled from 2019 to present, including the wells drilled by companies acquired in that time frame. The majority of these operators have participated in consolidation over the last two years as denoted by the asterisks next to each operator in the table.

This bolstered their Permian acreage positions and added contiguous acreage, in many cases. However, the collapse of crude prices in 2020 triggered a significant reduction in drilling activity across the basin that has yet to return to the levels of 2019 drilling. Operator guidance for 2021 indicates drilling will remain significantly suppressed for the balance of the year. Capital discipline remains the mantra for most E&P companies, raising questions about potential increases in planned drilling activity in 2H21 even with WTI above $70/bbl. With significant Permian inventory concentrated among these companies and suppressed drilling levels, how does this bode for long-term inventory drawdown?

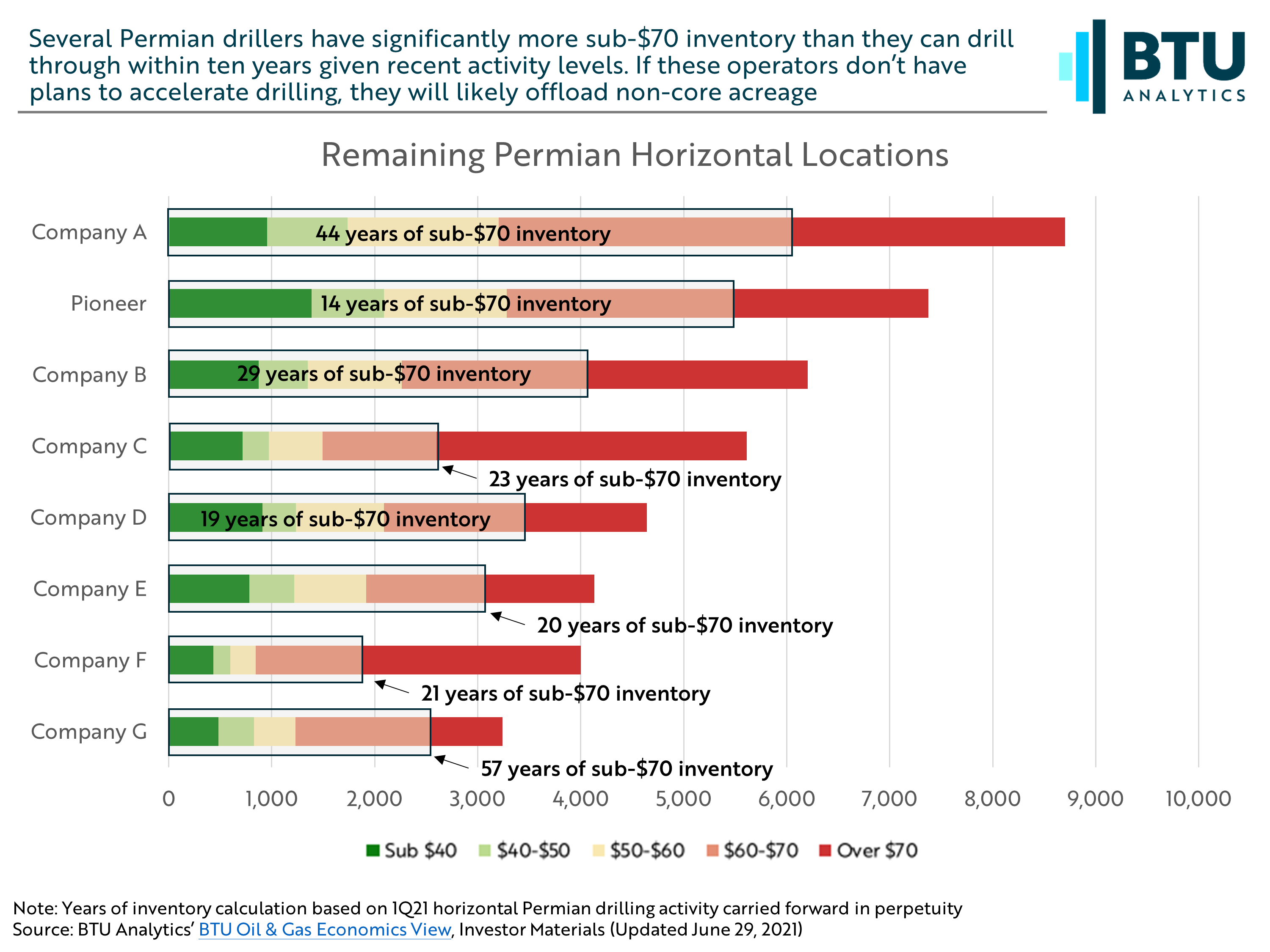

At the current pace of drilling 1Q21, the companies in the first table each have over a decade of drillable locations. For several of these companies, the inventory estimates suggest decades of sub-$70 horizontal locations remain. Pioneer has been the most active driller in the Permian in 2021 to date and subsequently has the shortest runway of remaining locations compared to its peers despite having the second most remaining locations. For all operators in the sample above, the inventory runway drastically exceeds the five-year window for proved reserves calculations used by the SEC, meaning most remaining locations provide limited benefit to reserve calculations. Additionally, focus on decarbonization is accelerating the concern of peak demand for oil and may cast further doubt onto the long-term viability of these locations as being economic in the future.

The recent frenzy of M&A activity has largely focused on whole-company acquisition or becoming a basin pure play, but divesting assets in basins of focus may become more prevalent. Occidental Petroleum recently announced the sale of non-core Permian Basin acreage to Colgate Energy Partners III, which is expected to close in 3Q21. While Occidental is still reducing debt from its recent acquisition of Anadarko, Occidental also represents one of the producers in the chart above with over a decade of remaining inventory to monetize either through drilling or divesture.

There is still plenty of time left on the clock in 2021 for companies to increase their drilling activity, but given recent commitments to capital discipline, it seems likely that 2021 will leave plenty of drillable locations untouched in the Permian Basin. Unless E&P companies start getting aggressive with developing their acreage or divesting non-core assets, they could be left holding onto significant amounts of unneeded acreage outside of the five or even ten-year windows. BTU Analytics’ BTU Oil & Gas Economics View allows for inventory analysis for public and private operators in major shale basins in addition to access to several other interactive economic data sets. Additionally, production and drilling data can be found within BTU View if you would like to keep apprised with recent activity trends.