Redetermination season is around the corner and with that comes the likely risk that operators will see their revolving credit lines shrink. BTU Analytics has already highlighted operators’ rush for liquidity from the equity markets, but what will happen to drilling activity if the spigot from bank financing is tightened a few cranks?

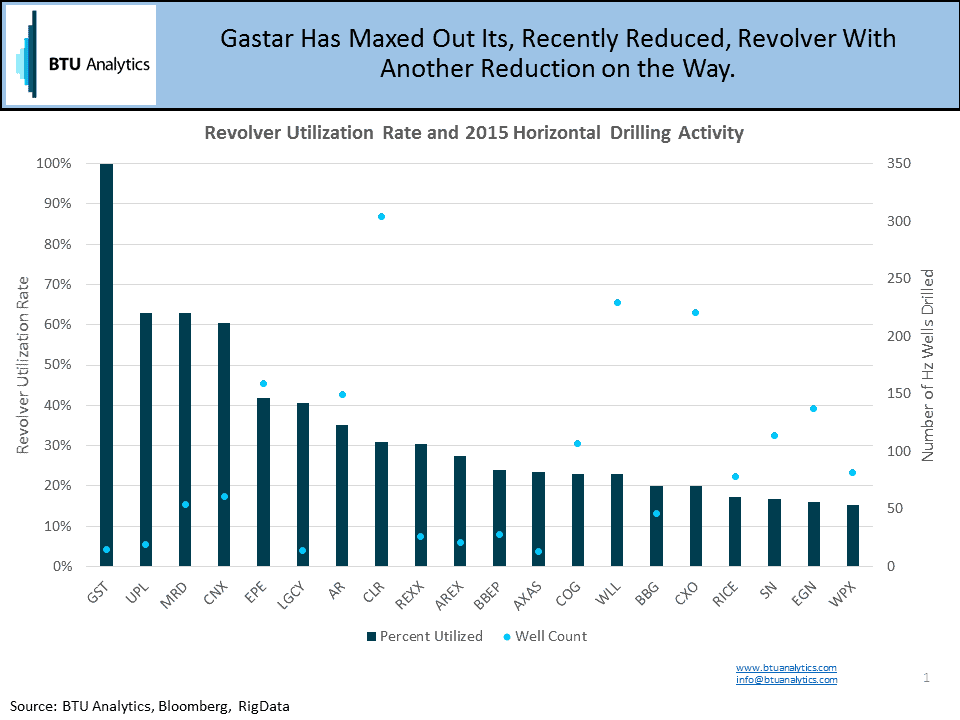

To determine who will be most affected by a reduction in revolving credit lines, BTU Analytics took a sample of about 60 companies across various regions and looked at how much of their revolver had been utilized as of the end of 2015. The graphic below shows the 20 operators with the highest utilization rate and their recent activity measured by the number of horizontal wells drilled in 2015.

Gastar (NYSE: GST), who has the distinction of standing at the top (or bottom) of our sample, has already had its borrowing base reduced recently and will again soon. Recently, Gastar’s revolving credit line was reduced from $200M to $180M and will again be reduced to $100M due to planned sales of Appalachia assets with the excess $80M to be repaid immediately.

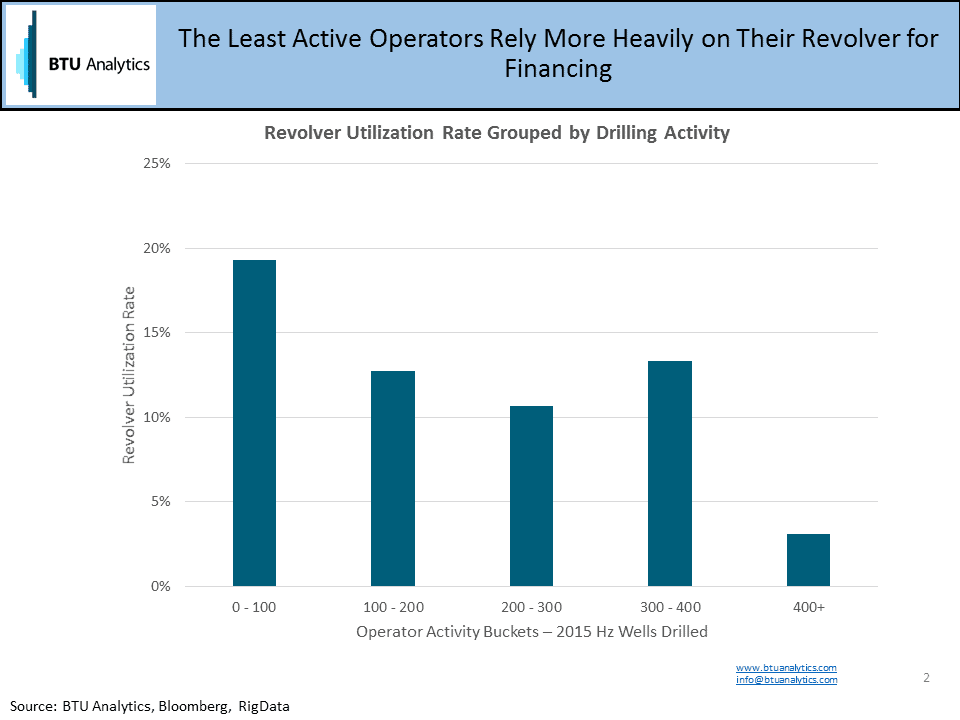

Looking at our sample from a different angle shows that the least active operators in our sample were the ones who relied most on their revolving credit facilities. The graphic below shows the average utilized revolver among operators with similar levels of activity. Conversely, this shows that the bulk of activity comes from operators who are able to finance their operations using other means.

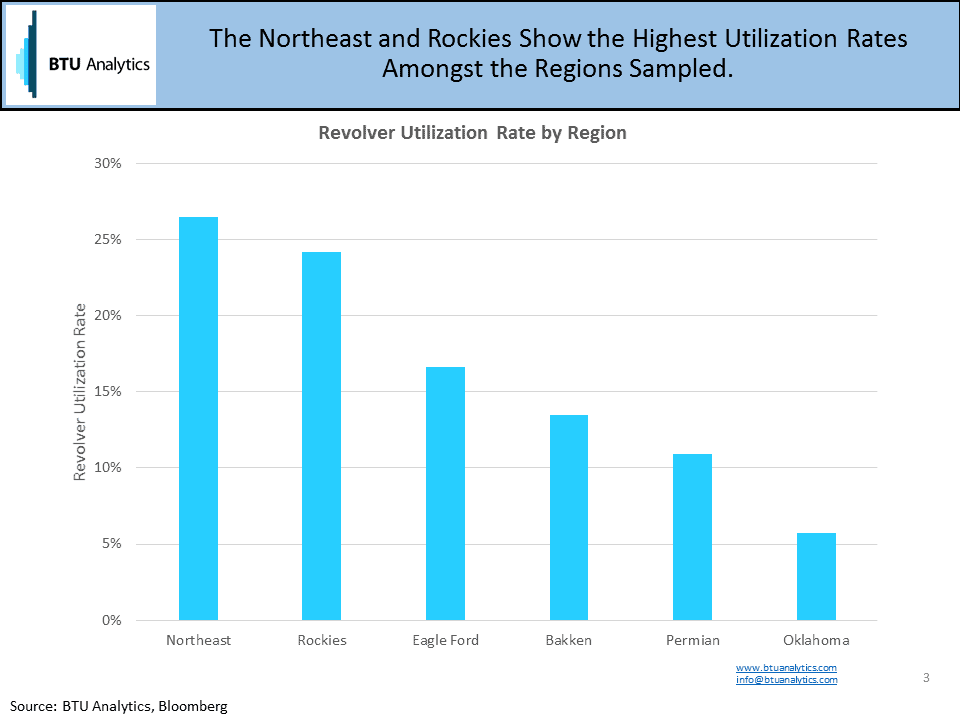

All of this evidence points towards a trim in borrowing base in the coming redetermination not having much of an impact on production activity moving forward broadly speaking. However, it might be the case that some regions will be affected disproportionately, so it is worth looking at utilizations by region. The graphic below compares revolver utilization rates by operator regions of focus, and shows that the Northeast and Rockies stand at the top of the pack with utilization rates higher than 24%.

The Rockies region has a smaller than average sample size, since there are few pure play companies in the Rockies, so this allows Bill Barrett (NYSE: BBG) and Ultra Petroleum (NYSE: UPL) to pull up the regional average. In the Northeast, while Gastar no doubt pulls up the Northeast average, something more could be at play. With the infrastructure build out occurring in the Northeast, operators who take commitments on new projects are required to provide a letter of credit to the midstream company to prove their credit worthiness. Often times this letter of credit will be drawn from a revolver, pushing up an operator’s utilization rate.

While the coming redetermination season will provide heartburn for some operators, for the most part, operators will be able to survive this haircut to liquidity. To see BTU Analytics’ complete view on North american production and drilling activity, request a free copy of our Upstream Outlook.