The COVID-19 pandemic, along with an oversupplied European market, poses a setback to the juggernaut growth rate of US LNG exports leading into 2020, but BTU Analytics does not predict this to be the final nail in the coffin for US LNG exports. Feed gas deliveries to export facilities fell as much as 62% at the trough, from a monthly average of 8.7 Bcf/d in February 2020 to 3.3 Bcf/d in July 2020. In spite of this precipitous decline in demand, BTU Analytics observed increases in August 2020 (prior to Hurricanes Marco and Laura) and expects LNG feed gas supplies to reach at least 5.7 Bcf/d in 2021, despite recent demand-driven setbacks. With molecules produced in Appalachia fighting constraints to reach the Gulf, and associated gas output in several key liquids-focused plays falling in response to prolonged weak crude pricing, that modeled LNG recovery will likely require additional near-Gulf molecules. Today’s Energy Market Insight will discuss the feasibility of gas production growth from a basin some might find surprising – the Western Eagle Ford.

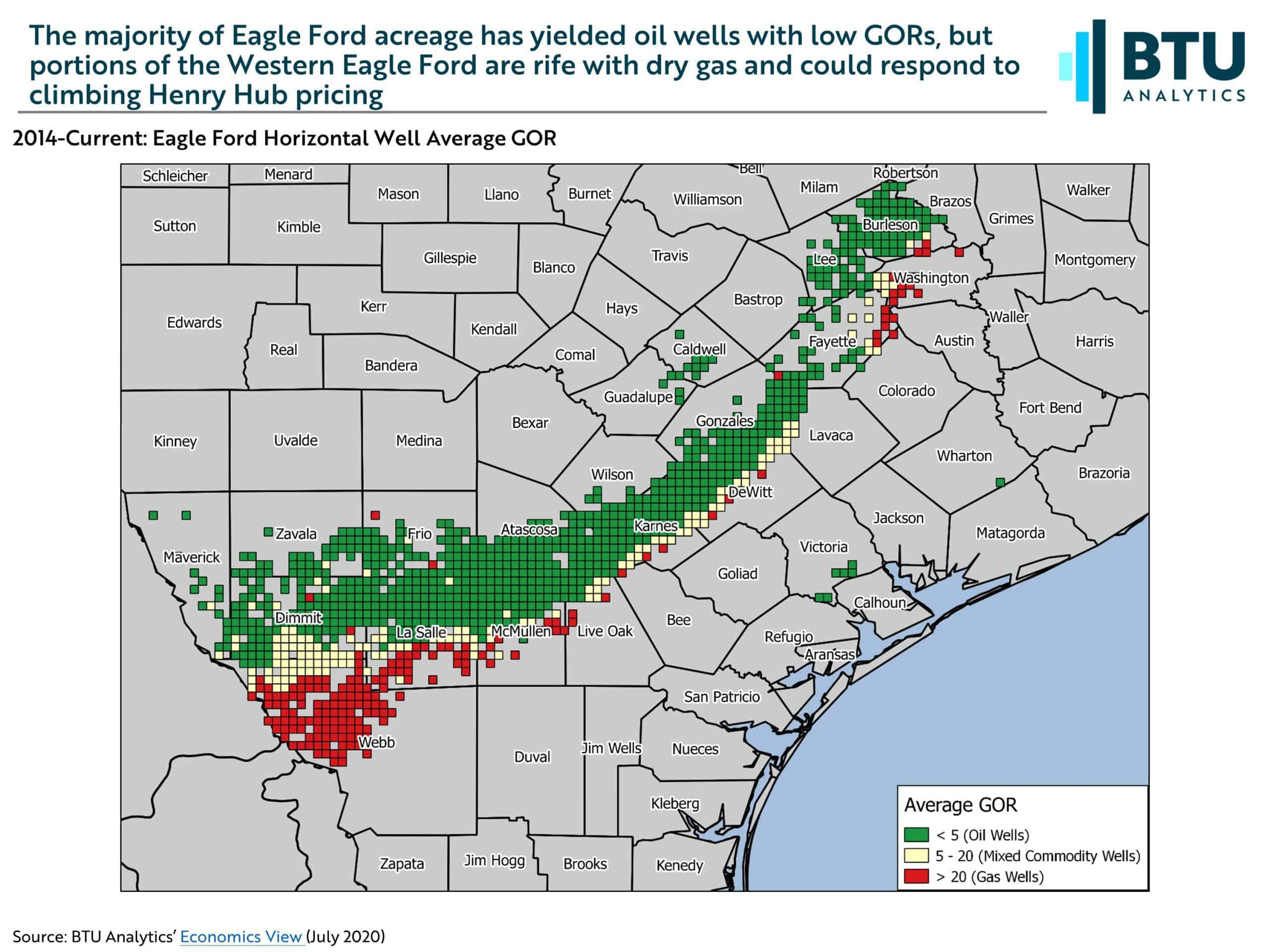

The Eagle Ford is typically thought of as a liquids-rich shale play, which is reflected by the abundance of grid boxes shown above with low average gas-oil ratios. Furthermore, the attractive oil breakevens in the eastern portion of the play are poised to play a significant role in the crude production recovery amid tepid price strengthening through 2023. However, Eagle Ford acreage includes a large window of dry gas development in the southern portion of the play, particularly in Webb and La Salle Counties. Dry gas acreage in the Eagle Ford has not drawn much attention for the last several years while gas prices paled in comparison to crude prices. However, recovering LNG export demand over the remainder of 2020 and 2021 appears likely to strain supply near the Gulf amid slow associated gas production recovery, creating what could become a perfect storm to revitalize dry gas-directed activity in the Western Eagle Ford.

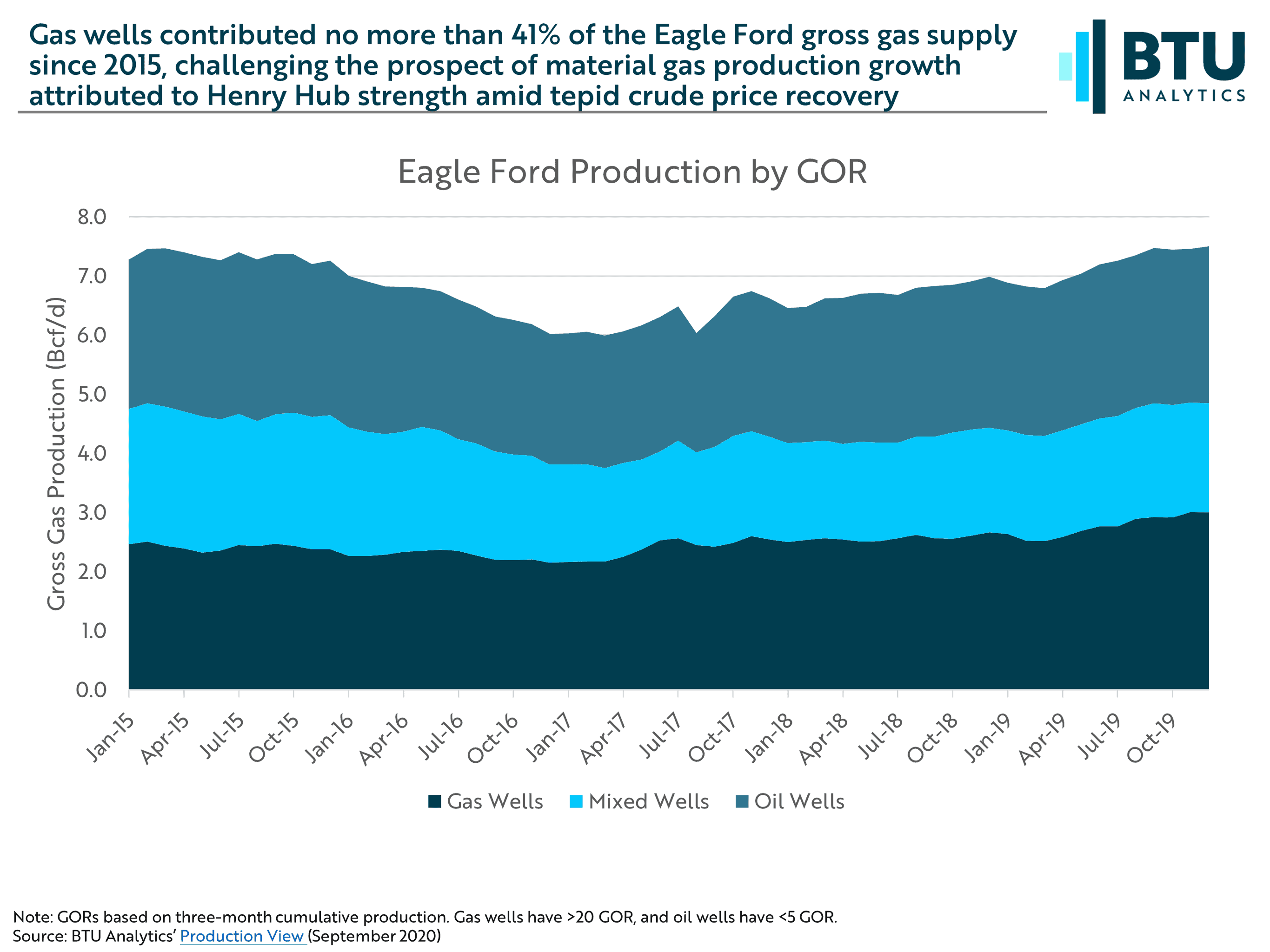

Using the same GOR-based classification for oil, gas, and mixed commodity wells, a breakdown of Eagle Ford gross gas production shows an oil and mixed commodity well majority compared to production from wells primarily targeting dry gas. Eagle Ford gas wells were responsible for 39% of the 7.2 Bcf/d average production in 2019. Given the dependence on liquids pricing for the oil and mixed commodity wells, it would be difficult to materially grow Eagle Ford gas production through new activity based solely on gas price strength.

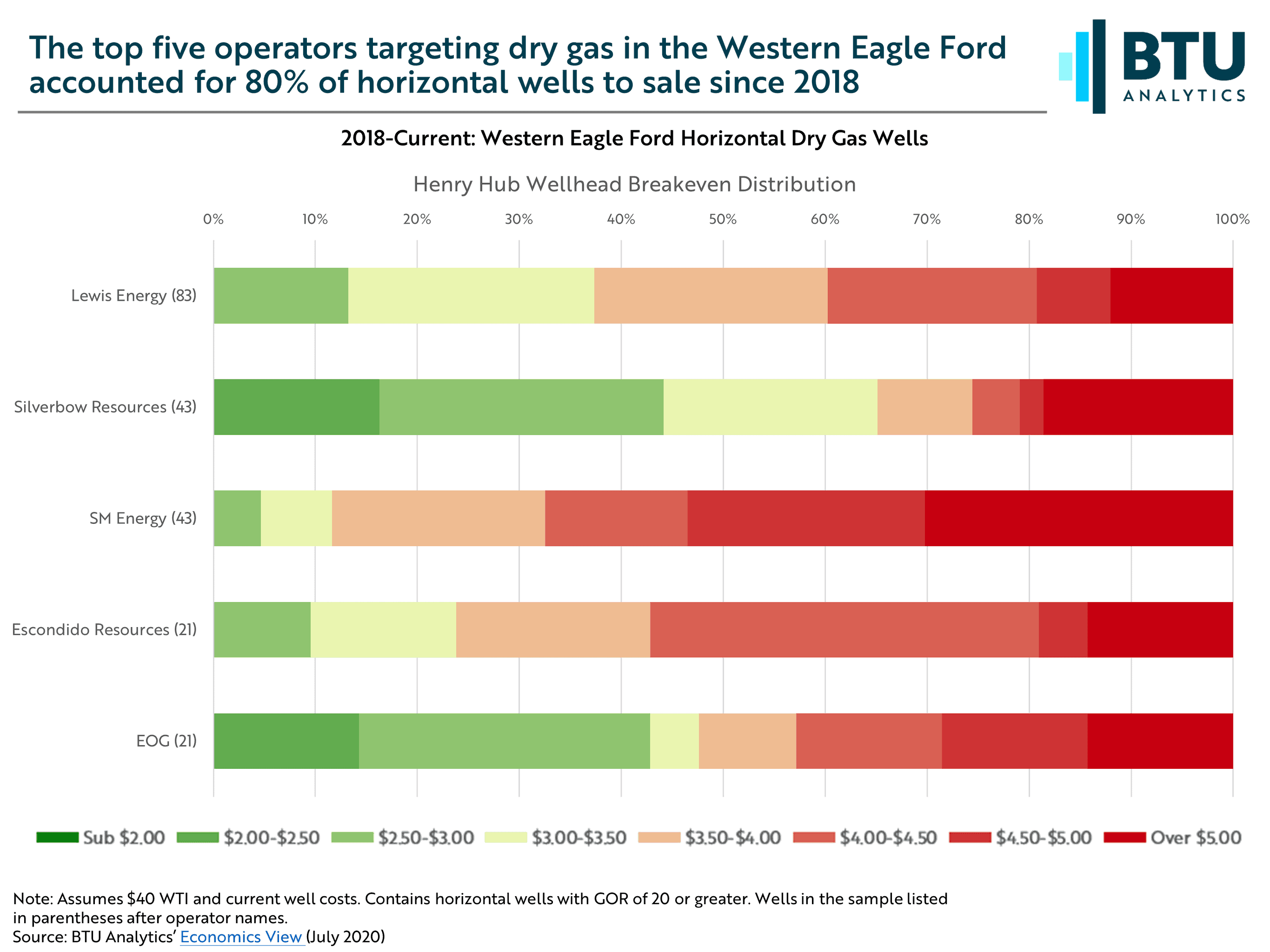

With winter, Henry Hub prices are expected to crest $3/MMBtu by December 2020. Dry portions of the Eagle Ford begin to gain appeal amid languishing crude prices, which can be seen in the BTU Economics View. The chart above shows a distribution of the top operators targeting dry gas acreage, but only two, SilverBow Resources and EOG Resources, turned more than 15% of horizontal wells to sale with gas breakevens below $3/MMBtu since 2018, which limits upside potential for dry Eagle Ford gas activity. With significantly underutilized drilling rigs and completion equipment sitting idle in most service companies’ yards across Texas, drilling and completion costs could likely be reduced, further improving future breakevens. It is also important to note that these are wellhead breakevens, meaning gas basis needs to be factored in before getting a realized, in-basin natural gas price. The Eagle Ford is positioned close to the Gulf, minimizing transportation costs to many LNG facilities when compared to most shale basins, but will this be enough to give the Eagle Ford an edge to fuel LNG exports?

With Henry Hub pricing rising as 2021 approaches, dry gas-directed activity in the Western Eagle Ford could gain momentum, but the lack of economically attractive gas-rich acreage, even at forecasted prices, will prevent most operators from benefiting. To perform your own breakeven analysis or run commodity price scenarios at a regional, operator, or customized acreage level, request information about a trial for BTU Analytics’ Economics View. For additional context regarding the drivers of our LNG exports, regional basis, and infrastructure build-out forecasts, check out this month’s Gas Basis Outlook.