Up until early October, strong oil prices in 2018 spurred investment in areas beyond the Permian like the Bakken. A jump in average horizontal completion activity in 2018 to 110 wells/month compared to just 83 in 2017 resulted in almost 200 Mb/d of oil production growth from January to December in the Bakken this year, pushing total production to a record 1.4 MMb/d. As investors and midstream companies look for new opportunities, the Bakken emerged as a key area of focus. Enbridge, Energy Transfer, Phillips 66, and Bridger have all announced pipeline projects that would impact the Bakken by either adding or removing pipeline capacity serving the region. In late October, Energy Transfer announced a binding open season to expand the DAPL and ETCO system to 570 Mb/d from its current capacity of 530 Mb/d, and not too long thereafter, on November 9, Phillips 66 and Bridger announced a binding season for the Liberty oil pipeline which is expected to have an initial capacity of 350 Mb/d and connect the Bakken and Rockies to Corpus Christi. While it is unclear how much of the Liberty capacity will be allocated to the Bakken, if we assume that it is 250 Mb/d, then between Liberty and the DAPL expansion we would add 290 Mb/d of incremental pipeline capacity connecting Bakken directly to the Gulf by the end of 2020. With these and other pipeline shifts occurring in the Bakken, we thought we would take a moment to review Bakken oil transportation dynamics and how they could shift over the next few years.

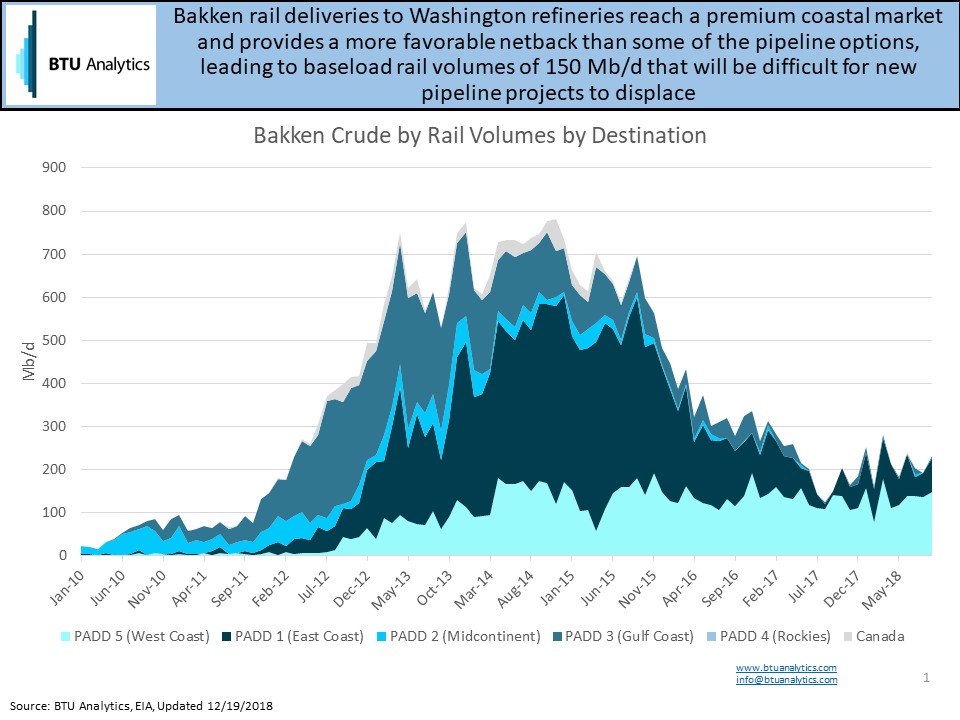

Currently, Bakken outbound pipeline capacity and in-basin refining is equal to production at 1.4 MMb/d. However, rail has been and continues to be an important outlet for the Bakken as well and has averaged 250 Mb/d in 2018. Of these volumes, 130 Mb/d on average moves to the Washington refineries on the West Coast and is cost competitive with many of the pipeline routes serving the Bakken while also reaching a premium coastal market. The other 120 Mb/d of rail is being delivered primarily to the East Coast and is more expensive to ship via rail and has been supported by wide Brent/WTI spreads. The eastbound volumes are more susceptible to competition from new pipeline projects that could provide lower cost access to premium coastal markets as well.

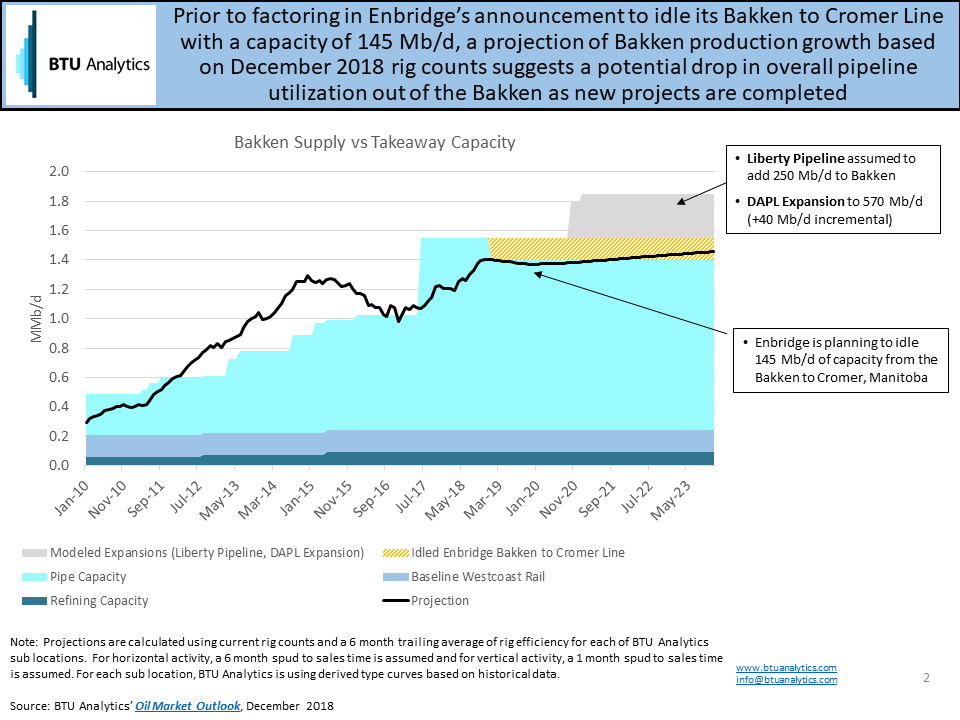

Therefore, while utilization of existing pipeline infrastructure has averaged 80% in 2018, implying spare capacity of 250 Mb/d and calling into question the need for a new project, the destination of existing pipelines compared to additional direct Gulf Coast access via new projects is key. Both Energy Transfer’s DAPL expansion project and Phillips 66 and Bridger’s Liberty oil pipeline have proposed to increase Bakken pipeline access to premium Gulf Coast markets and could likely do so at a lower cost than the rail option to the East Coast.

That said, a production outlook based on current rig counts shows Bakken production as relatively flat at first glance and calls into question the need for additional pipeline capacity. However, a third Bakken pipeline announcement by Enbridge to idle its Bakken to Cromer line which connects into the highly congested Canadian Enbridge Mainline System eliminates 145 Mb/d of Bakken takeaway capacity from the region. Taking this into account, Bakken pipeline capacity looks much tighter, and if the Bakken returns to a growth trajectory, these new pipelines could prove to be attractive options for Bakken shippers.

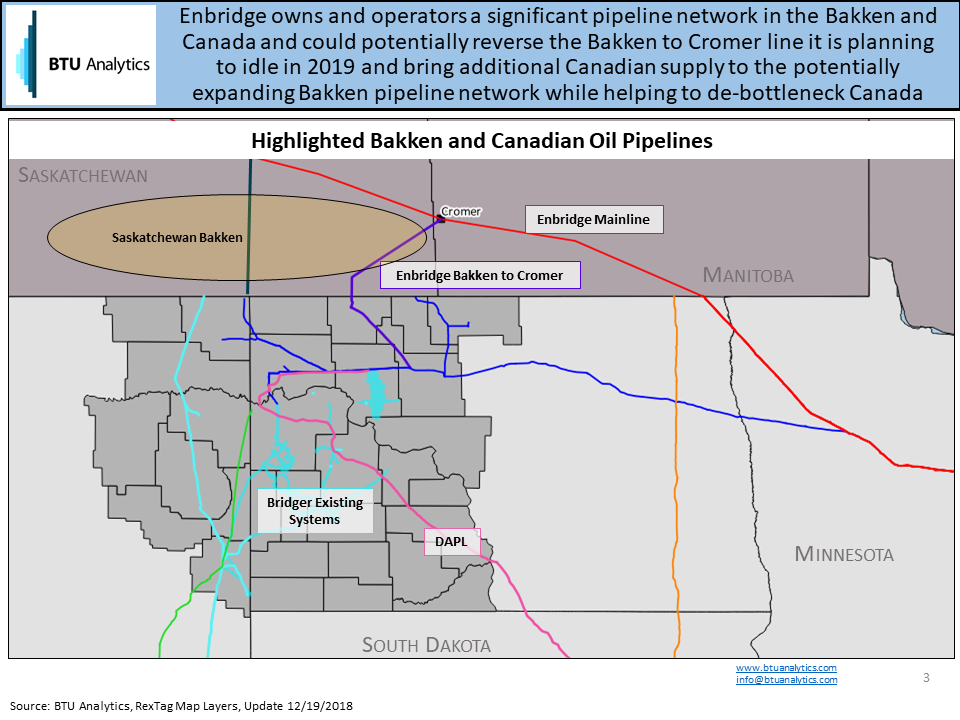

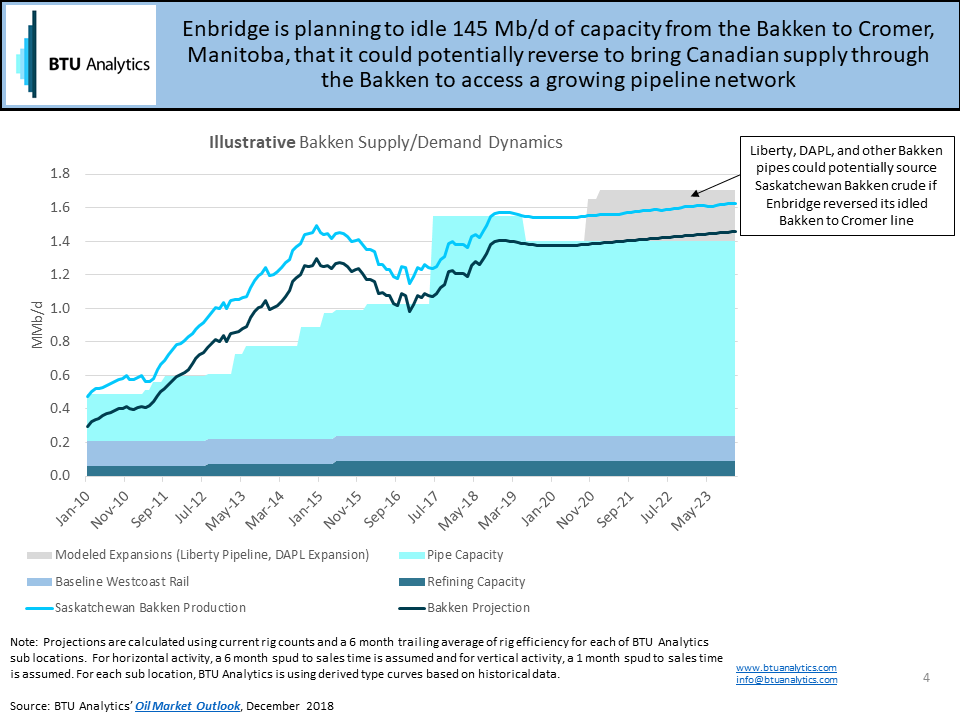

Finally, Enbridge’s Bakken to Cromer line used to flow Saskatchewan crude into the Bakken until it was reversed in 2013. Therefore, as Enbridge (a key Canadian pipeline player) looks at its portfolio of pipelines for expansion and de-bottlenecking opportunities, if there ends up being spare pipeline capacity out of the Bakken relative to Bakken production, there may be an opportunity to redirect some portion of Saskatchewan Bakken production, which is also primarily light, through the Bakken pipeline network to the Gulf. Saskatchewan Bakken production in 2018 averaged 168 Mb/d and is expected to remain stable over the next five years. The chart below shows that if Saskatchewan Bakken production can be re-directed from the Enbridge Mainline through the Bakken, it would support high utilization of existing and proposed Bakken projects as well as add more capacity to the Enbridge Mainline for upstream Canadian oil producers in the oil sands who have been staring down the pipe at negative $38/bbl differentials to WTI in November until Alberta imposed mandatory production cuts on oil production of 325 Mb/d for 1Q 2019.

While DAPL and Liberty are being pitched as pipeline projects for the Bakken, could they ultimately provide a much-needed outlet to Canadian producers as well? For more information on changing oil pipeline dynamics request a sample of our Oil Market Outlook Report.