Higher oil prices have lifted drilling activity across the country, and Oklahoma is no exception. In the STACK, a handful of operators are driving the majority of area activity, and those operators have touted the potential of the region for some time. Today’s market commentary brings STACK economics into focus by providing an update on who’s driving regional activity and the success those operators have seen to date.

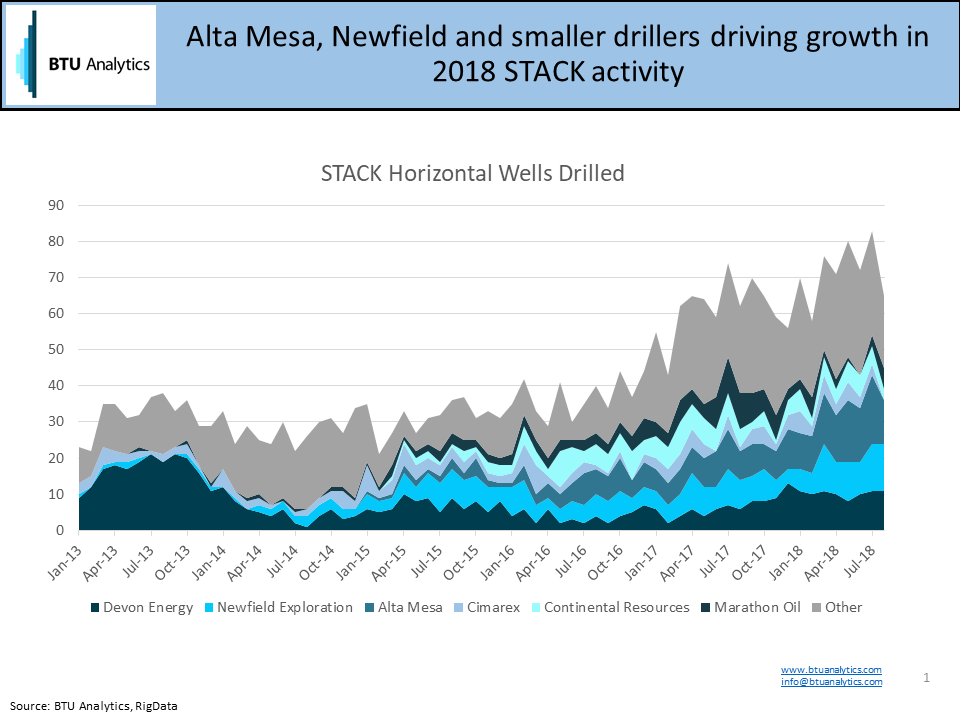

Drilling activity in the STACK has grown steadily since mid 2016, with operators now averaging 70-80 new wells each month. The top six producers represented 63% of basin activity in 2018.

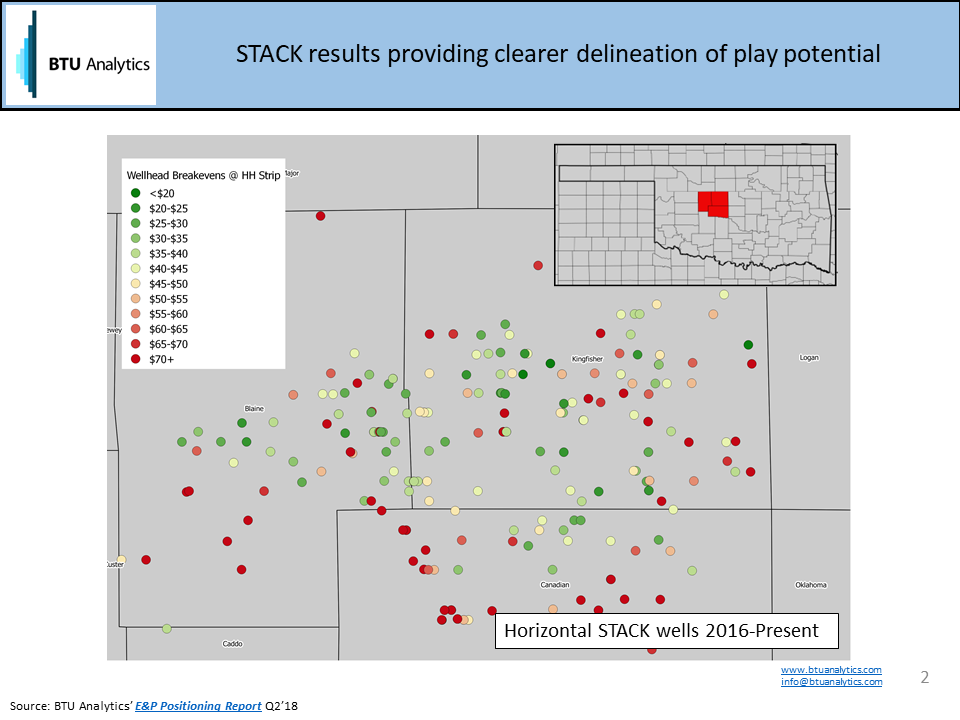

BTU Analytics calculates economics for every horizontal well in the major onshore regions as part of our E&P Positioning Report, using state reported production data, estimated well costs, and our in-house knowledge of cost structure including gathering and processing costs. In the STACK, significant play variation in gas to oil ratios (GOR) and reservoir pressure over relatively small geographic areas factor into the variability of economic outcomes. The slide below shows the economics of wells turned to sales from 2016 to present in the play.

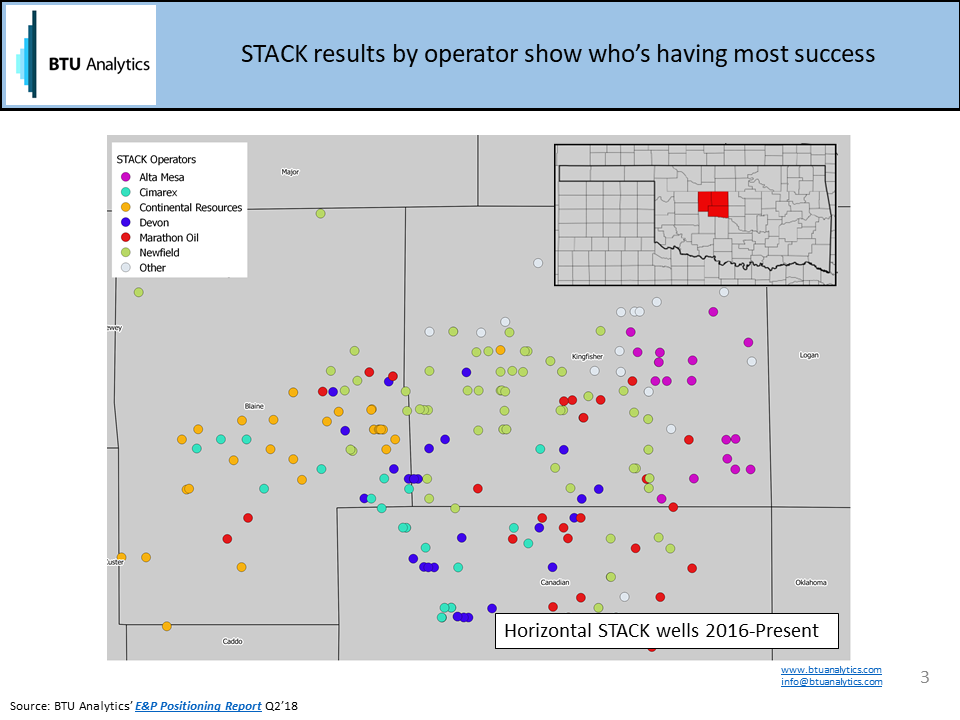

Looking at these same wells from an operator perspective shows which operators are having success and where. Notably, Continental Resources, Newfield, and Alta Mesa have had the best average results since 2016 on wells with public data available.

How do these results compare to other assets within these producers’ portfolios? Will infrastructure constraints ruin the party? And what happens to the STACK once Permian takeaway constraints no longer limit the pace of US growth? Find these answers and more by requesting samples of BTU’s E&P Positioning Report and Upstream Outlook Report.